This month’s edition, which includes guest contributor Kyle Van Pelt, kicks off with the big news that Morgan Stanley is acquiring asset manager Eaton Vance, in what was largely billed in the media as asset management consolidation of Eaton Vance’s mutual fund family … but in practice may be a $7 billion bet from Morgan Stanley on the future of Direct Indexing technology to displace ETFs and mutual funds, as in practice more than half of Eaton Vance’s assets were actually managed or overlay portfolios of its subsidiary Parametric (which is estimated to control a whopping 75%-plus of the current Direct Indexing marketplace). Though in practice, Morgan Stanley will likely simply re-package Parametric into an ultra-HNW solution for its own 16,000-plus brokers serving affluent clients… leaving the door still open for other Direct Indexing startups (or fast-encroaching incumbents) to gain market share with the mass of independent advisers.

From there, the latest highlights also feature a number of other interesting adviser technology announcements, including:

Read the analysis about these announcements in this month’s column, along with a discussion of more trends in adviser technology, including MoneyGuide’s new built-in analytics to identify potential product sales opportunities for clients, Income Conductor’s novel discount on E&O insurance for independent advisers that use its retirement income planning software (with underwriters presuming that clients will be more likely to be satisfied with their outcomes?), ScratchWorks FinTech accelerator announcing its Season 3 winners with $5 million of funding and opening for new applications for Season 4, and CRM systems signaling that they may be becoming the new hub for advisory firms as Holistiplan, fpPathfinder, fpAlpha and Knudge all announce new integrations to Redtail and Wealthbox!

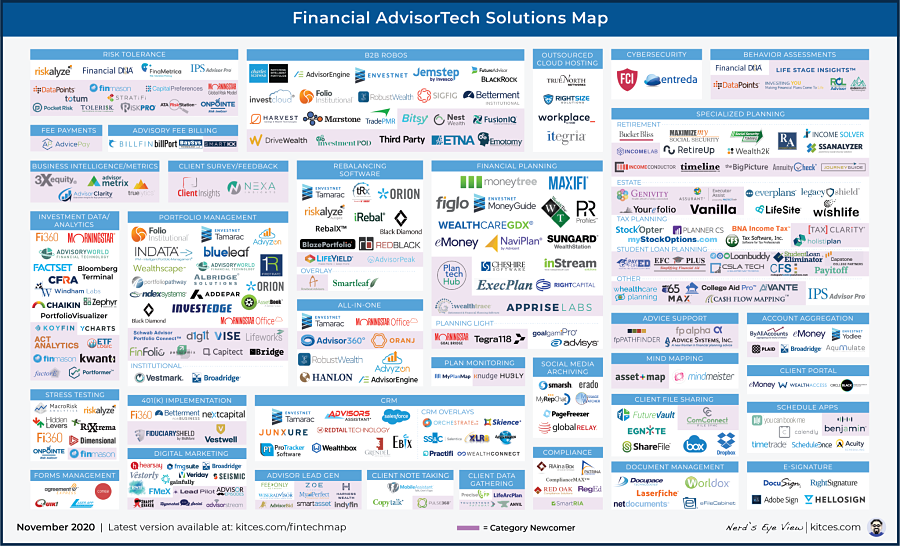

Be certain to read to the end, where we have provided an update to our popular new Financial AdviserTech Solutions Map!

I hope you’re continuing to find this column on financial adviser technology to be helpful! Please share your comments at the end and let me know what you think!

*#AdviserTech companies who want to submit their tech announcements for consideration in future issues, please send to [email protected]!

Is Morgan Stanley acquiring Eaton Vance to create its own proprietary direct indexing solution? The concept of “direct indexing” has been around for more than 20 years, since early pioneers like Parametric began to offer their ultra-high-net-worth clients a deconstructed version of the S&P 500 index by owning each of the individual stocks of the S&P 500 to facilitate their clients’ ability to engage in tax-loss harvesting (especially valuable at ultra-HNW clients’ top tax brackets) on each individual stock and not just the index fund as a whole. In practice, though, such strategies were only available to HNW investors, as it took a fairly sizable portfolio to be able to buy all 500 stocks of the S&P 500, in the appropriate percentage allocations, when limited to the whole-share units of individual stocks (e.g., with a small portfolio, buying just one share of a stock trading at $100/share with a $100,000 portfolio would give it a 0.1% allocation, which is greater than the weighting of 300 out of the 500 stocks in the S&P 500!). However, over the past decade, the rise of fractional share investing through brokerage/custodial platforms like Apex Clearing — and by extension to the early robo-advisers that used them, including Betterment and Wealthfront — have made such direct indexing solutions available to much smaller portfolios. When coupled with the recent emergence of “ZeroCom” (the widespread availability of zero-commission stock trading), it raises the question of whether advisers and investors will soon eschew index funds altogether and just purchase the direct-indexed version without the mutual fund or ETF wrapper fee at all. Of course, the caveat is that popular index funds like the S&P 500 have already become so commoditized that they are available for a nearly negligible cost of just a few basis points, while it still costs at least some money to offer and operate direct indexing software. Because of that, skeptics have questioned whether direct indexing will ever really go mainstream or remain in the domain of HNW clients who can better maximize the tax benefits (if only because they can harvest tax losses at higher marginal tax rates). But this month, Morgan Stanley announced that it was acquiring Eaton Vance. Most financial advisers know it for its mutual fund offerings, but in practice it has more than 50% of its $500 billion of AUM in direct indexing solutions through its subsidiary, Parametric, which it had quietly acquired all the way back in 2003 with less than $5 billion of AUM before direct indexing was on anyone else’s radar screen! Which means Morgan Stanley in one fell swoop has acquired the largest dominant player in the direct indexing space — as Parametric had by some estimates a 75%-plus market share in direct indexing already — which it can now distribute via its nearly 16,000 brokers to a bevy of ultra-HNW clients, as well as further expand Parametric’s “Custom Core” offering, an extension of direct indexing in which investors not only hold the components of the underlying index but then modify them to fit personal preferences (e.g., by under- or overweighting investment factors, or screening out undesired stocks in an ESG overlay). Notably, though, because Morgan Stanley as a traditional wirehouse is concentrated in the ultra-HNW investing space in the first place, it seems unlikely that the acquisition will be the catalyst that democratizes direct indexing for the masses — leaving the door open to other upstarts like OpenInvest, JustInvest, Ethic Investing, and Folio’s Direct Indexer to expand the reach either to consumers directly or through the broader financial adviser community. Nonetheless, when Morgan Stanley is willing to put $7 billion on the table to acquire the current direct indexing market leader — which was growing so quickly, the rumor was that Eaton Vance was about to rebrand to Parametric when it was acquired — it’s not clear that direct indexing will fully disrupt the current marketplace of ETFs and mutual funds, but it’s hard to call it just a fad anymore!

LPL acquires Blaze portfolio rebalancing software for $12 million to in-house its own model marketplace? One of the hottest trends of the past four years has been the rise of so-called model marketplace, where advisers receive a list of prospective model portfolios they can use with their clients, and in theory with as little as two clicks of a mouse button — one to select the model portfolio, and the second to implement it in the client’s account — can get the client up and running with a diversified portfolio. Nominally, the appeal of the model marketplace approach is that it greatly enhances the efficiency of advisers themselves, who save time by not needing to be so hands-on in creating and customizing their clients’ diversified portfolio allocations (as customization instead simply becomes choose-the-right-match-in-portfolio-model from an ever-growing marketplace list). Except the reality is that financial advisers don’t actually spend very much time on the actual duties of investment management in the first place; according to Kitces Research, the average solo financial adviser spends about 5.2 hours/week on investment-related activities, which amounts to 260 hours per year, or an average of only two to three hours per year per client, much of which would still have to be spent, even with a model marketplace, both to do due diligence on the models being used and monitor whether each individual client is on track. Accordingly, a recent YCharts industry study showed that only about 10% of advisers are using a model marketplace to access third-party strategies, and a recent Cerulli study similarly showed only 16% of advisers using asset allocation models as the primary basis for their portfolio construction process, raising the question of whether model marketplaces are just a niche solution for a small subset of advisers who still find the portfolio construction process to be painful in a world where individual advisers can already buy a wide range of rebalancing software solutions that largely automate the process for them, anyway. However, the reality is that model marketplaces also reflect a broader battle underway in the industry — where advisers are disintermediating mutual fund and other third-party asset managers by using technology to manage their own (largely ETF) portfolios, ETF providers are trying to figure out how to distribute models to advisers as a way to get them to use the asset manager’s ETFs (by including their own ETFs in the prebuilt models), and adviser platform intermediaries (e.g., broker-dealers) are trying to figure out how to get a piece of the pie that they’re losing when advisers eschew mutual funds (and their 12b-1 and sub-TA fees) and largely cut their broker-dealers out with their own self-managed portfolios. Because the key to easily implementing model portfolios is to have the technology to do it, in recent years a number of adviser platforms and asset managers have been acquiring rebalancing software solutions to vertically integrate their technology-based model distribution platforms, from Morningstar acquiring TRX and Invesco acquiring Jemstep, RedBlack, and Portfolio Pathways to Oranj acquiring TradeWarrior and even BlackRock taking a stake in Envestnet. Accordingly, it’s perhaps not surprising that LPL, the largest independent broker-dealer by head count with more than 16,000 reps, announced this month that it was acquiring Blaze Portfolio, one of the only portfolio rebalancing software solutions that had not already been acquired (leaving AdvisorPeak as one of the only remaining “pure plays” left in what was not long ago a very crowded independent category!?). In fact, the scarcity of rebalancing software platforms still for sale appears to have been a major driver of the price, with Blaze reportedly acquired for $12 million plus another $5 million in contingencies, or a total of $17 million for just 135 firms, which at a typical average revenue of $10,000-$15,000 per firm (for small to midsized RIAs, where Blaze primarily competed), implies revenue that may have only been around $2 million, and a multiple of 6-9X revenue! Of course, the reality is that LPL didn’t likely acquire Blaze for Blaze’s existing 135 firms and revenue — though LPL has indicated that Blaze will continue to remain available as an independent solution that can grow its own market share and revenue — but instead for the ability to leverage Blaze with its 16,000-plus advisers, and more importantly for the potential for LPL to generate additional asset management revenue (which could be many multiples of the software revenue alone) by utilizing Blaze as the hub for its own internal model marketplace trading implementation (with the ability to generate an expanding list of internal model offerings from LPL to its advisers). Still, though, the real question will be whether LPL can drive higher implementation of its in-house models (and a layer of asset management fees or ETF distribution revenue-sharing payments it can collect) through the use of Blaze, in a world where the majority of advisers have increasingly shown a preference to eliminate layers of intermediary fees and avoid model marketplaces. Not to mention that when advisers just package together technology-automated diversified portfolios, it raises the question for the client of what the adviser’s value is in the first place (when direct-to-consumer robo-advisers can accomplish the same at an even lower cost). Which means that in the end, the success of LPL’s acquisition of Blaze may hinge less on advisers’ needs for portfolio management construction tools, but instead on whether LPL can deepen its advisers’ focus on financial planning to the point that they feel confident in their ability to charge advice fees and add value even, and especially if, LPL’s Blaze and its list of models diminishes the adviser’s own role in the portfolio management process for clients.

Lincoln Investment acquires Hanlon Advisory Software for its own proprietary all-in-one broker-dealer technology platform. Interactive Advisory Software was one of the original silver bullet AdviserTech solutions of the 1990s, aiming to unify the “Big 3” components of adviser technology — CRM, financial planning and portfolio management — into a single all-in-one solution (in an era when the internet was still nascent and there were no open AdviserTech APIs for cross-platform integration). Yet more than a decade later, IAS has become the negative embodiment of the all-in-one challenge, having created a solution that was capable in all categories but a master of none, beset from all directions by best-in-class category solutions that inevitably managed to dissuade any particular adviser away (as IAS simply didn’t have the resources to compete in every category at once). The end result was that IAS was eventually sold in 2012 to Hanlon Financial, a TAMP with $3.4 billion of AUM, with the goals of both using the software to differentiate its support capabilities for advisers by pairing together investment management and technology (a la Envestnet) and to tap the nearly 170 firms using IAS that collectively had $70 billion of AUM to potentially use Hanlon for its investment management. Yet eight years later, the goal of converting IAS users to Hanlon never materialized, with Hanlon’s AUM declining below $1 billion and the IAS-cum-Hanlon-Advisory-Software user base down to just 135 firms (as, in the end, technology for a TAMP is usually deemed table stakes and TAMPs must still compete, first and foremost, in the expensive-to-distribute, highly competitive world of asset management). Which is problematic not only for the outright decline in AUM for Hanlon, but also because maintaining software in a competitive environment — especially an all-in-one platform that competes in several categories at once — necessitates a growing user base to amortize the ever-rising costs of iterating new features and paying down the technology debt. As a result, Hanlon announced this month that its all-in-one Hanlon Advisory Software solution is being sold to Lincoln Investment, a top-25 broker-dealer by adviser head count with more than 1,000 reps that hopes to leverage the software to power its own proprietary adviser tech platform. From Lincoln’s perspective, in a world where independent broker-dealers increasingly struggle to differentiate themselves from one another, having its own proprietary software solution takes a page from the playbook of Commonwealth Financial, which is known for the quality of its own Commonwealth-only all-in-one solution that it uses to attract top advisers. (Consequently it has one of the highest average productivity levels of any independent broker-dealer.) The irony is that Commonwealth announced last year that it was spinning its Advisor360 platform out from the broker-dealer, having found that even with more than 2,000 high-production reps, it was still too expensive to amortize development costs over its internal rep base. It landed a major deal with MassMutual to power the platform for its 9,000 reps (and having a broader software growth strategy to fuel future software development). This raises the question of whether Lincoln will be able to reformulate IAS/HAS into a competitive all-in-one solution itself over an adviser base that is larger than Hanlon’s but still smaller than what Commonwealth deemed to necessitate a spin-off. Nonetheless, Lincoln Investment’s bold purchase at least gives it an opportunity to better chart its own technology future, in a world where most other broker-dealers are increasingly beholden to their back-end clearing firms or Envestnet’s often essential but increasingly encroaching platform, and where most firms don’t have the time to build their own solution and few options exist to achieve the head start of buying a going concern to build upon (especially now that IAS/Hanlon Advisory Software is once again off the market!).

YCharts recapitalizes with private equity as it crosses $15 million ARR and expands from investment research to investment communication. For literally decades, Morningstar has been the staple of investment research and analytics tools for financial advisers, with a near hegemony in the broker-dealer world and a strong presence in the RIA community (often among RIAs that broke away from broker-dealers and continued to use the software they already knew). While some deep dive investment platforms like Bloomberg have attempted to encroach on Morningstar’s space, adoption has been limited, even among RIAs, who are more likely to manage mutual funds and ETFs but not necessarily utilize the granular stock-level investment capabilities of a Bloomberg terminal. That made it all the more notable in 2013 when a new investment research startup called YCharts appeared, gunning to be the Bloomberg for RIAs (but at a fraction of the price point), and funded by Morningstar as a key investor (ostensibly to help it grow in an RIA channel where Morningstar itself was still lagging). YCharts has grown in the seven years since, built not just with a focus toward providing a less expensive alternative to Bloomberg for RIAs, but on tools commonly needed and missing in the RIA community (e.g., analytics and monitoring tools for advisers who build their own models and don’t use third-party model marketplaces and a popular Excel Add-In tool that allows advisory firms to export YCharts data into their own spreadsheets for further analysis). But in the end, the upside of any AdviserTech platform is limited when it exists only to support even essential back- and middle-office functions of advisory firms, compared to the potential pricing power that comes when AdviserTech software is a front-office tool that directly supports client — and especially prospective client — meetings. This is why Riskalyze was able to rapidly gain market share against all of its risk tolerance competitors and incumbents; while it is nominally labeled risk tolerance software, in practice Riskalyze is most often used as a proposal generation tool for prospects (where proposals are couched in the terms of why the adviser’s proposed portfolio measures up better in terms of the client’s Risk Number than their existing, often not-well-diversified portfolio). It’s the new-revenue-generating opportunities Riskalyze creates that allow it to charge $200/month or more for what most other competitors struggle to provide at half or even a quarter of the cost. In that vein, YCharts has increasingly begun to position itself not just as a tool for investment research, but one for investment communication with clients and prospects, moving itself beyond just back-office investment analytics and into front-office client interactions. Now, YCharts has passed $15 million of annual recurring revenue, or ARR, and has announced a capitalization with new private equity partner LLR Partners. LRR bought out all existing owners, including the increasingly awkward competitor Morningstar, and is putting new capital into YCharts to fuel not just further growth but what YCharts CEO Sean Brown suggests may be new acquisitions to expand YCharts’ reach. Where exactly YCharts will go with its new capital remains to be seen, though a natural extension would be either to go deeper into investment communications (e.g., by partnering with Clearnomics’ white-labeled market commentary for clients?), or potentially to pair with another risk tolerance software solution in a step toward the still underdeveloped AdviserTech category of proposal generation (though arguably YCharts already has more than enough other investment metrics to offer advisers as the measuring stick for a superior portfolio proposal without mimicking Riskalyze’s Risk Number approach). In the end, though, YCharts’ growth in an already crowded investment data and analytics marketplace simply speaks to the fact that sometimes, going really deep with just a few key features is all it takes to get a positive foothold in the adviser community. From there, the farther AdviserTech can shift from back office to front office (and from the “overhead” to the “revenue-generating” side of the adviser’s P&L), the more pricing power and adoption it can gain!

CapGainsValet launches new Delivery service to support advisory firms tracking end-of-year mutual fund distribution announcements. Given the volatile and tumultuous market in the face of the coronavirus pandemic, coupled with what continue to be record flows out of traditional open-end mutual funds and into ETFs, 2020 is shaping up to be a potentially big year for end-of-year mutual fund distributions, especially coming on the tail end of a 10-year bull run that has meant significant capital gains accumulated within mutual funds. For many advisory firms, distributions are challenging to track because each mutual fund company makes its own announcements of anticipated year-end mutual fund distributions, on its own timeline, often on its own website (and not a centralized resource). That led five years ago to the creation of CapGainsValet, a resource created by a financial adviser for the adviser community that aggregates mutual fund capital gains distribution announcements from more than 250 mutual fund managers (and what may be close to 1,000 individual mutual funds across those firms), so advisers can quickly look up the latest details on their various mutual fund holdings across client accounts. The baseline “Free Search” at CapGainsValet provides direct links to the mutual fund distribution announcements of the 10 largest mutual fund managers for advisers, including Vanguard, American Funds, DFA, Fidelity, Pimco, and BlackRock, while a Pro Search option that accesses all 250 mutual fund managers’ 2020 announcements is available for a small one-time fee of $5. In 2020, CapGainsValet has created a new “Delivery” feature, where the adviser submits a list of mutual fund ticker symbols, and CapGainsValet will provide the firm with a personalized spreadsheet that is updated every Monday with the latest capital gains estimates (as new distribution estimates come out from the mutual fund managers through the fall), at a price of just $3.50 per mutual fund tracked (with a $50 setup fee and a $200 minimum per firm). Of course, the irony is that collecting and tracking mutual fund distribution estimates is still a painfully manual process for something that arguably should just be incorporated into portfolio management and rebalancing software directly (e.g., where iRebal or Tamarac or Eclipse simply gather and show advisers the anticipated estimated capital gains when they’re reviewing client portfolios, or warn them if they’re about to purchase a mutual fund that has significant embedded gains that are about to be distributed). But until portfolio rebalancing tools build an integration directly to CapGainsValet (or collect the data themselves), for the typical advisory firm that may spend several hours trying to track end-of-year capital gains estimates, CapGainsValet is arguably still an incredible deal for the time savings (especially the new Delivery service that largely automates the tracking and reporting for advisers, though firms must contact directly for a firm-specific quote!).

Envestnet shifts MoneyGuide back to its product distribution roots with new premium analytics to help spot opportunities for (product sales to) clients. In the early days of financial planning, the reality was that a financial plan wasn’t produced to get paid for planning; instead, it was used primarily to demonstrate that the client had a need that the adviser could fill with a product they had for sale. Accordingly, the financial planning software illustrated a retirement shortfall, which the client could solve by saving more in the account their adviser would manage; an insurance gap, which the client could fill with the adviser-sold life insurance policy; an estate tax liquidity shortfall, which the client could also solve with an adviser-sold life insurance policy; and an education funding gap, again solved by saving more into an adviser-managed investment account, or later an adviser-managed 529 college savings plan. In essence, the financial planning software’s purpose was to identify opportunities for product sales as a part of a needs-based selling approach, and advisers (only) did updates when there was a new opportunity to demonstrate a new need that the adviser could solve with a new sale. Over the past 20 years, the business of financial advice has increasingly shifted away from its product-based transactional roots, though, and toward a more relationship-based advice model, where the adviser provides ongoing advice to an ongoing client to earn an ongoing fee. Yet despite the rising level of ongoing advice, most financial planning software is still largely built to produce one plan at a time, where each planning instance is a stand-alone event, and the adviser only discovers planning opportunities in the process of doing that updated plan (or only discovers after the fact that there was nothing to plan for). Ideally, though, advisers wouldn’t repeatedly produce (time-intensive) financial plans just to see whether there are any new planning opportunities; instead, the planning software would help monitor the client’s situation, and communicate to the adviser when a planning opportunity arises. Accordingly, this month, Envestnet announced a new “premium analytics” offering — an extension of an “Opportunities To Engage” module it highlighted earlier this year — that will comb through client data in the financial plan to try to spot situations where an adviser can engage the client on various “insurance, health, and lending” opportunities. In addition, Client Opportunities will monitor for key client dates when money may be in motion (e.g., an approaching retirement date), provide weekly updates of the probabilities of success for every client’s financial plan in a “Plan Pulse” feature, and help monitor the client’s portfolio for new investment opportunities with a next-best-action-style “Recommendations” engine. On the one hand, the appeal of MoneyGuide’s new Opportunities (and related Pulse and Recommendations features) is that, perhaps finally account aggregation is beginning to yield its promised value for advisers, going beyond just pulling in data to update otherwise static reports and using the flow of data to actually trigger actions and events for the adviser to take on the client’s behalf (or at least communicate with/to the client about), which turns financial planning meetings from reactive (wait for the client to come in with an issue) to proactive (contact the client because the planning software identified an issue). On the other hand, though, the reality is that MoneyGuide’s new Client Opportunities don’t necessarily focus on opportunities for client advice, per se, but on the triggers related to investment, insurance and lending product needs. That, not coincidentally, aligns perfectly with Envestnet’s solutions as the largest platform TAMP investment provider that also recently launched its own Insurance/Annuity and Credit Exchanges for advisers to facilitate financial services products for their clients. That means, in essence, that Envestnet appears to be turning MoneyGuide’s financial planning software into the front-end sales engine for its own product distribution platform, in the hopes that advisers will operate as its last-mile salespeople to their clients. Of course, the reality is that clients often do need various financial services products, and to the extent that Envestnet creates open insurance exchanges, it won’t necessarily have a conflicted incentive to steer advisers and their clients toward any particular product, as long as the adviser implements whatever products they may ultimately need through any of Envestnet’s ever-widening shelves of products. That ultimately positions Envestnet well to supplant the broker-dealers it’s historically served as the new technology-based product distribution platform of the future — with the caveat that if MoneyGuide increasingly becomes a product distribution channel for Envestnet, it may be appealing for the traditional but declining base of brokers at broker-dealers, but it also opens the door for competing financial planning software solutions that choose to focus on advice-centric advisers instead.

Income Conductor negotiates discounted E&O insurance for advisers who plan their clients’ retirement income strategies with its software!? One of the great ironies of the ongoing debate about whether advisers should be uniformly held to a fiduciary standard is that broker-dealers have repeatedly raised concerns that a fiduciary obligation would increase costs because of the fiduciary liability they would face, even though in practice, less transactional and more advice-centric fiduciary RIAs actually pay lower rates for Errors and Omissions insurance. In other words, the insurance companies that actually have to price risk and pay claims (and put their own money on the line to do so) have long since recognized that ongoing-advice relationship models present less legal liability than more transactional brokerage businesses. Of course, not all RIAs engage in low-risk or “pure” advice behavior, and as a result, E&O insurance companies must still underwrite individual advisers and firms to evaluate the actual risk exposure, looking for factors that may indicate the adviser is more client-centric and advice-centric and at reduced risk for the higher-liability transactional approach. In this context, it’s notable that this month, Income Conductor, a retirement planning software solution that models time-segmentation “bucketing” strategies to formulate retirement income plans for clients and then monitor them on an ongoing basis, announced a partnership with the Varney Agency to provide a discount of up to 20% on the E&O insurance for Income Conductor’s adviser users, on the basis that advisers using ongoing retirement planning software tools will better understand their clients, craft better recommendations, and therefore be less likely to make E&O claims (thus the E&O insurance discount). From the perspective of the Varney Agency, the deal is appealing for the potential to gain market share in a competitive world of adviser E&O coverage, with a pathway for risk-based (or rather, less-risk-based) pricing discounts without doing as much time-consuming underwriting. For Income Conductor, the appeal of the deal is both a nice affinity discount for its adviser users and an implicit validation of its retirement planning approach as actually being seen as less risky to insurance actuaries (i.e., more likely to result in satisfied clients, rather than the dissatisfied clients who may sue their advisers!). On the other hand, it’s notable that the Income Conductor/Varney deal also provides discounted coverage for cyberliability coverage — nominally as a testament to Income Conductor’s software security, but since the policy would apply to the entire advisory firm, which would typically use many other types of (potentially less secure) software as well, it’s not entirely clear how much of Varney’s E&O and cyberliability insurance discounting is actually an adjustment for risk, and how much of the discount is simply due to the kind of group affinity discounting that’s already common for insurance carriers trying to reach a large mass of small advisers that are otherwise difficult to market to (the Financial Planning Association offers a 5% discount on E&O insurance with Markel simply by virtue of being an FPA member, and NAPFA provides E&O insurance affinity discounts to its members as well). Nonetheless, the idea that advisers who use financial planning or retirement planning software may be lower risk for E&O insurance carriers, such that they would be able to merit a discount on coverage, is striking. If more E&O insurance carriers and their actuaries concur, it may quickly become a trend as planning software providers try to one-up each other to validate whose adviser users make the best financial plans that are the least likely to result in client complaints and legal liability.

Could Altruist’s new partnership with Apex Clearing drive portfolio management software costs down to just $1? One of the most striking aspects of the RIA business model is that RIAs receive access to their core investment platforms entirely for free, a remarkable contrast to independent broker-dealers that, even at scale, will typically retain at least 10% of the broker’s revenue (and only pay out the remaining 90%). The difference is driven in part by the fact that broker-dealers have greater compliance responsibilities to oversee the brokers on their platforms (while RIA custodians largely defer investment adviser representative oversight to the RIA that’s using the platform), and, in a larger part, to the fact that RIA custodians get to keep all of the brokerage and custody/clearing revenue generated on their platforms, while the typical independent broker-dealer is itself an intermediary that rests on top of an underlying custody/clearing firm and receives only a part of those underlying brokerage/custody/clearing economics. On the other hand, the reality is that the platform provided by modern RIA custodians is still limited, in that it doesn’t cover the full breadth of an RIA’s technology needs. That has led to an explosion of portfolio management and performance reporting AdviserTech solutions over the past two decades, with so many providers that it’s not even clear there’s enough of an addressable market for all 50-plus to survive even at pricing that often amounts to $10,000 to $15,000 of revenue per adviser with a full client base. Yet, in practice, RIA custodians generate as much as 15 to 25 basis points of average revenue on an advisory firm, of as much as $150,000 to $250,000 of revenue from a $100 million AUM RIA (and potentially upwards of $2 million/year for a $1 billion RIA!). That means the RIA custody business is so profitable that custodians could actually develop their own portfolio management solutions and provide them to their RIAs for free. Sure enough, over the past decade, TD Ameritrade acquired iRebal and offered it to its RIAs for free, Fidelity has built WealthScape for its RIAs to manage their portfolios, and last year Schwab announced its new Portfolio Connect platform to similarly support the trading and performance reporting functions that RIAs have historically paid independent software companies (e.g., Orion, Black Diamond, Tamarac, etc.) to provide. Against this landscape, it was notable last year when startup Altruist launched what was nominally an independent multicustodial portfolio management and performance reporting solution for advisers at a nominal price of $1/month/client when the going rate averages closer to $40/month/client. The key distinction, though, is that Altruist wasn’t just a performance reporting solution, but instead stated that it intended to operate as an RIA custodial platform for RIAs, using the economics of the 15-25bps custody/clearing business to subsidize the cost of its software down to nearly nothing. Of course, the caveat is that it’s still very expensive to launch a new RIA custodian from scratch, in a world where assets under administration are measured in the tens or hundreds of billions of dollars (or in the case of Fidelity and Schwab, literally in the trillions), and as a result, Altruist actually established itself as an introducing broker to an underlying clearing platform, effectively replicating the independent broker-dealer model but in a pure RIA-only, technology-only format. Unfortunately, though, even building just the technology layer on top of an underlying clearing platform is still difficult, and as a result, Altruist announced earlier this year it was switching to new clearing partner DriveWealth, and this month announced that it was changing again, this time to Apex Clearing. While in theory Altruist’s model was to nearly “give away’’ a multicustodial portfolio management solution for $1/month/client in the hopes of overlaying and winning away competing custody business, it’s not clear whether competing RIA custodians will continue to provide data feeds to support Altruist’s Trojan horse strategy, or whether it will simply be forced to operate as a proprietary Apex-only trading platform (akin to TradingFront’s partnership with Interactive Brokers). Nonetheless, in a world where the historical battle has been RIA custodians bundling software for free (on top of the lucrative economics of the custody/clearing business) against independent software providers that require advisers to pay for software that allows them to maintain independence from those RIA custodians (and/or to be multicustodial), Altruist’s business model represents a substantive break as a “software company” operating as an introducing broker to capture basis points on custody/clearing in lieu of (far lower) per-adviser or per-client software fees. That highlights that even if Altruist itself isn’t the ultimate winner of the battle given its own challenges in finding the right clearing firm to build its solution on top of, it portends a world in which other AdviserTech software companies will have to consider whether they’re going to cross the divide and go directly into the custody/clearing business — or risk being put out of business by those that do (or that already are).

Will AdviserTech replace annuity wholesalers for product discovery as tech-based distribution accelerates with new RightCapital and SS&C integrations? Annuities have quite a storied history among not only consumers but financial advisers themselves. In some circles, “annuities” is a bad word, analogous to high-commission high-pressure sales tactics. In other circles, they are the greatest thing since sliced bread, providing a guaranteed-income foundation to retirement that simply cannot be matched by a diversified portfolio alone. No matter which side of the argument you are on — or most likely, somewhere in between — the reality is that annuities are jumping (back) into the spotlight right now, reflecting combination of both the search for new ways to create income for those entering the decumulation phase with bond yields at historic lows and a major tax law change last year that for the first time creates the potential for fee-based annuities (where RIAs can be paid directly from the annuity, akin to all the other investment assets they advise upon). Accordingly, in an effort to match the growth of the fee-only RIA movement and as a response to Reg BI (where even hybrid broker-dealers are increasingly concerned about offering commission-based annuities alongside fee-based advisory accounts), new fee-based annuities are being manufactured and brought to market lightning quick. While they are still quite a bit more expensive than passive ETFs and index funds (in light of the additional guarantees that annuities have attached), they are increasingly competitively priced for a (no-commission) adviser to offer them. Yet in practice, adoption of fee-based annuities in the RIA channel in particular has been slow. For those affiliated with broker-dealers and still doing commissioned-based business, annuities have always been a part of the tool set. But it’s been difficult for annuity companies to shed their legacy high-commission perceptions among RIAs, known for being reluctant to take wholesaler calls and having a “Don’t call us, we’ll call you” mentality. Not to mention that as such fee-based annuity offerings proliferate, advisers may suddenly struggle in determining how to pick the best one for their clients. Enter a new wave of adviser technology partnerships with annuity providers! Whether it’s analyzing the risk profile of an annuity product on Riskalyze or identifying the need for an annuity when conducting a financial plan in RightCapital or any of the other planning platforms, a growing number of adviser software platforms are leveraging the transparency of new fee-based annuity products to incorporate them into and begin illustrating them directly within an adviser’s planning and analysis tools for clients, comparing those companies’ products against each other to try to find which one is truly going to provide the best results for the lowest cost. That in turn can be illustrated in clients’ ongoing portfolios as well, with new partnerships between annuity companies and fee-based annuity distributors like DPL Financial Partners, and portfolio performance reporting solutions like SS&C’s Black Diamond or Orion Advisor Services. From the adviser’s perspective, such software-based analyses provide appealing time efficiency in the process of crafting annuity recommendations. After all, why would advisers take five meetings with five different wholesalers from five different companies, when they can click a few buttons to evaluate all five products in the context of that specific client’s financial plan? In other words, the marriage of AdviserTech platforms and annuity product manufacturers promises the potential to actually deliver on the promise of greater efficiency in annuity product selection, effectively turning AdviserTech software into the product discovery channel, and shifting wholesalers into a product due diligence support role (as the adviser further vets the software-suggested solution). In essence, then, the world of annuity product distribution is rapidly being transformed from one of relationships with external wholesalers to one in which annuity products compete in a software-analysis-driven meritocracy… a tremendous step forward for the industry, but with a substantively different role for AdviserTech software providers in their role of matching product solutions to the needs of advisers’ clients!

Is CRM becoming the new adviser hub as Knudge, fpPathfinder, fpAlpha And Holistiplan build new integrations to Redtail And Wealthbox? Given that most financial advisers are tied to either a broker-dealer or RIA custodial platform to facilitate the implementation of their client portfolios, it is perhaps not surprising that the “adviser platform” itself has largely been centered around broker-dealers and custodians. From TD Ameritrade’s VEO, Fidelity’s WealthScape and LPL’s ClientWorks to Commonwealth’s Advisor360, adviser platforms have become the daily dashboard that the adviser logs into, the center of the adviser ecosystem that other providers look to integrate into, and they increasingly are becoming a distribution channel unto themselves for everyone from asset managers and product manufacturers to niche AdviserTech solutions looking to reach advisers (and their clients). In fact, control of the adviser dashboard has become so valuable that increasingly independent AdviserTech platforms have been trying to elbow their way in, from Envestnet’s Advisor Portal to Orion Advisor Solutions, the spin-off of Commonwealth’s Advisor360 to the ongoing rise of Morningstar Office. The caveat, though, is that while historically advisers were largely investment-centric — such that they used their broker-dealer or RIA custodian’s platform, and any competitor had to at least match the investment capabilities of those platforms — the ongoing transition from investment-centric to financial-planning-centric advisers is triggering a fundamental reordering of which systems have priority for the adviser’s attention, such that the primary question the adviser asks every morning is not, “How are my client portfolios performing today?” but “What financial planning tasks do I need to follow up on to service my ongoing clients?” Accordingly, the flow of AdviserTech integrations is beginning to shift from investment platforms to the adviser’s CRM system. In fact, over just the past month, Knudge (which helps manage financial planning task follow-ups for clients) announced an integration to Wealthbox, Holistiplan (which helps advisers analyze client tax returns) announced an integration to Redtail and fpPathfinder (which makes financial planning checklists that advisers can record in their CRM to document that all the key issues were covered in the client conversation) also announced an integration to Wealthbox (after announcing an integration to Redtail earlier this year). And this summer, fpAlpha (which helps analyze client documents to find planning opportunities) announced an integration to Redtail. It’s a remarkable shift from just one or two years ago, where the standard path for early stage AdviserTech startups was to build integrations to TD Ameritrade’s VEO as a pathway to initial adviser distribution. Of course, the idea that a CRM system could be a hub and ecosystem unto itself isn’t new; Salesforce has built much of its success on effectively cultivating an App Exchange marketplace where third-party providers could design plug-ins to the Salesforce CRM system. But with Salesforce currently concentrated in larger adviser enterprises, while CRM systems like Redtail and Wealthbox dominate in the small to midsize independent RIA marketplace where AdviserTech firms tend to gain their initial traction, it’s the non-Salesforce CRM systems that appear to be becoming the new pathway for AdviserTech innovation to be introduced to the marketplace.

ScratchWorks AdviserTech Accelerator announces Season 3 finalists and opens Season 4 applications. One of the biggest challenges when it comes to AdviserTech innovation is the lack of capital to fund such innovation in the first place, in a world where most FinTech venture capital firms are only interested in funding startups in the direct-to-consumer marketplace that have the potential to become $1 billion-plus unicorn investments, and show disdain for the small addressable market of financial advisers who tend to produce companies that may be worth only tens or hundreds of millions of dollars at maturity. The end result is that the bulk of AdviserTech startups are homegrown solutions, where advisers create software to solve their own problems at their own firms, then start offering their solution to other advisers, and eventually end up with a software company in addition to their adviser firm. Such was the path of AdviserTech solutions from Junxure to Redtail in the CRM category, Orion to Tamarac in portfolio management, iRebal to TradeWarrior and RedBlack for stand-alone rebalancing, RiskPro and Tolerisk for risk tolerance, Hyperchat Social for social media, Benjamin from Wela for client communication, and our own AdvicePay for advisory fee billing. In other words, while capital itself is limited for most AdviserTech solutions, advisory firms themselves are very profitable enterprises, affording at least a subset of entrepreneurially minded firm owners the ability to use the profits from their advisory firms to fund their AdviserTech endeavors. In 2017, a group of RIA executives decided to come together and expand that approach by developing ScratchWorks, a “Shark Tank”-style program where AdviserTech founders can pitch a group of six RIA executives who know and love the financial adviser world and, if persuaded, will invest their own capital into the endeavor. Still, though, picking prospective winners in the AdviserTech marketplace is challenging and risky, such that in its inaugural season, ScratchWorks only actually made an investment in Snappy Kraken’s marketing technology (for $100,000), and in Season 2 the ScratchWorks investors ultimately passed on all three finalists. Season 3 of ScratchWorks featured LifeWorks (which is aiming to build an end-to-end, all-in-one, cloud-native RIA platform with everything from CRM to digital account opening to client billing and performance reporting), Act Analytics, which is building a portfolio construction tool specifically to facilitate advisers talking to their clients about their values preferences and then easily implementing ESG portfolios aligned to those client preferences, and ReAllocate, which is aiming to help RIAs invest their clients in direct real estate holdings as an alternative to publicly traded or nontraded REITs (albeit in a limited partnership form that will necessitate K-1s for clients and be limited to accredited investors). And in the end, ScratchWorks decided to make a major investment for Season 3, putting nearly $5 million of capital to work, with $3 million going into ReAllocate, given the growing hunger for more ways to invest client assets beyond traditional market-traded stocks and bonds, and $1.8 million to LifeWorks, to fuel more holistic technology platforms for RIAs. At the same time, ScratchWorks announced the launch of its Season 4, so any AdviserTech entrepreneurs who are hoping to get their own shot at capital to build the next great AdviserTech solution, applications are open through Dec. 18!

New Product Watch: EvoShare launches adviser-white-labeled UPromise for retirement solutions. For the mass of Americans, credit cards walk a fine line between being a convenience and a curse, providing easy access to credit to smooth out short-term disruptions in household cash flow and the ease of not needing to carry around cash, but posing the challenge of keeping a good handle on one’s personal spending and not unwittingly (or irresistibly) going into debt in the midst of impulse spending. For a subset of consumers, though, credit cards are a gateway to rewards, from points and travel to outright cash-back deals, where credit card companies make money not on the credit card interest (that applies to debt-based spenders), but simply on the “interchange” fees (typically about 2% to 3%) that merchants are required to pay credit card vendors to have their purchases processed, effectively remitting a portion of the interchange fees back to the spender and seeking those who will spend enough for the credit card company to profit on interchange volume alone. In this vein, credit card companies have been pushed to come up with increasingly exotic deals and partnerships to attract spenders, from ever-rising packages of points and cash-back discounts, to arrangements like UPromise, where cash-back contributions are added directly to a 529 college savings account (credit card cash back with a purpose!). More recently, EvoShare entered the marketplace with a similar approach to UPromise, except its goal was not to tie credit card cash-back dollars to a college savings account, but instead to a retirement account, establishing partnerships with 401(k) plan record keepers to allow plan participants’ cash-back contributions to go directly into their employer retirement plan. In the years since, EvoShare has further expanded its marketplace, similar to the way UPromise did, by negotiating deals directly with a wide range of online stores, from Target to Walmart, Lego to Microsoft, allowing consumers who purchase through the EvoShare portal to receive additional cash back directly to their retirement accounts (a form of marketing affinity program, where EvoShare itself keeps a small scrape of the negotiated discount for itself to fund its own platform), and nudges to save more through EvoShare’s own “Impulse Savings” tools. Alternatively, consumers can simply link their existing credit cards and then shop locally and receive retirement contribution credits on qualifying purchases (again, similar to UPromise). Now EvoShare is looking to partner with advisory firms directly, which will be able to white-label a co-branded version of the EvoShare portal directly for their clients, allowing them to provide spending discounts to their clients and have those savings go directly toward the clients’ emergency savings, their 529 plan, their 401(k) plan, or even a directly held IRA or brokerage account that the adviser manages! In addition, EvoShare allows clients to invite their friends and family to the (adviser-co-branded) portal and associated mobile app, potentially driving additional referral opportunities. Ultimately, most advisory firms are not accustomed to being tied to clients’ household spending budget and cash flow, and some may find it awkward to suddenly be offering nominal discounts on clients’ groceries and household expenditures when previously they had focused on managing their life savings balance sheet. On the other hand, when advisory firms are increasingly feeling pressure to show value and be involved on a more holistic basis with their clients, EvoShare may provide an appealing foundation to expand the advisory firm into a more holistic relationship with the client (and with a white-labeled portal that reinforces the new value the advisory firm is bringing)? Though notably, for its initial foray into wealth management, EvoShare is pricing at $250/month for each advisory firm office location, with a 10-license minimum (i.e., $2,500/month) and a $5,000 setup fee, which means initially EvoShare will likely only be used by larger RIAs, super-OSJs and independent broker-dealers with multiple locations.

In the meantime, we’ve updated the latest version of our Financial Advisor FinTech Solutions Map with several new companies, including highlights of the Category Newcomers in each area to spotlight new FinTech innovation!

So what do you think? Will LPL be able to gain momentum on its model marketplace and in-house models by offering Blaze Portfolio internally? Will Altruist be able to disrupt the RIA custodian marketplace (and portfolio performance reporting solutions) with its new Apex Clearing partnership? Is direct indexing going to gain momentum as the next big thing after ETFs? And would you want to offer credit card/spending discounts to your clients as a way to expand your brand (and to nudge clients to save more to their investment and retirement accounts)? Please share your thoughts in the comments below!

Special thanks to Kyle Van Pelt, who wrote the section “Will AdviserTech replace annuity wholesalers for product discovery as tech-based distribution accelerates with new RightCapital and SS&C integrations?” You can connect with Kyle via LinkedIn or follow him on Twitter at @KyleVanPelt).

Disclosure: Michael Kitces is a co-founder of AdvicePay and fpPathfinder, both of which were mentioned in this article.

Michael Kitces is the head of planning strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay, and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’s Eye View. You can follow him on Twitter at @MichaelKitces.

Craig Iskowitz is CEO and founder of Ezra Group, a management consulting firm providing advice to the financial services industry on marketing and technology strategy. You can follow him on Twitter @craigiskowitz.

Clients are saying they would consider switching advisors if another professional offered estate planning services, according to a new Trust & Will survey.

CEO Laurel Taylor says the fintech's composable AI stack helps workers optimize dollars across Trump Accounts, 529s, 401(k)s, and other employee benefits.

The bank has swiped three private banking veterans from BNY as the city climbs the ranks of America's fastest-growing wealth hubs.

Employee accounts, crypto trials and job cuts frame a pivotal year for the Swiss lender.

New name draws on founder's family history as consolidation reshapes the broker-dealer landscape.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.