This month's edition kicks off with the big news that Riskalyze has been recapitalized with a valuation of more than $300 million, as the risk tolerance assessment tool continues to expand its adviser reach — seemingly unimpacted by an explosion of new startup competitors that have failed to make much of a dent in its growing market share — and move into more adjacent components of the adviser tech stack. Yet with increasingly large competitors firing back with their own recent new offerings — from Morningstar's Risk Score to Orion's new 3D Risk Profile — and the majority of advisers still apathetic and not using any risk tolerance software tools (Riskalyze's or any other) at all, the question arises as to whether Riskalyze's new round of capital will be deployed to continue growing its presence in the U.S., begin to go global into new (and less competitive) markets in Europe instead, or adapt its trading platform to move into the hot new space of direct indexing where there are even more dollars currently in flux?

From there, the latest highlights also feature a number of other interesting adviser technology announcements, including:

Read the analysis about these announcements in this month's column, and a discussion of more trends in adviser technology, including:

And be certain to read to the end, where we have provided an update to our popular “Financial AdviserTech Solutions Map” as well!

#AdviserTech companies that want their tech announcements considered for future issues should submit to [email protected]!

For as long as financial advisers have been regulated, the regulators have placed a fundamental obligation that the adviser must “know your client,” or KYC, to understand whether recommendations being made are appropriate given their investment goals and tolerance to take investment risks. As a result, risk tolerance was primarily viewed through a compliance lens, whether advisers, after onboarding a client, conduct an assessment of their goals and risk tolerance to be able to document the appropriateness of their subsequent recommendations.

Until Riskalyze showed up in 2011. What was unique about Riskalyze was that, rather than treating risk tolerance as a KYC obligation (after the individual has become a client), it shifted the risk tolerance conversation to the prospecting stage, where those who had not yet become clients could get an understanding of how their current portfolios were aligned to their tolerance, how the adviser’s portfolio would be (better) aligned to their tolerance, thereby creating a level of desire and urgency to improve one’s (risk) situation by hiring the adviser. And done in a manner that went beyond the traditional approach of complex investment analyses full of Greek letters (alpha, beta, sigma, etc.).

In other words, Riskalyze’s real win was creating a common language that both advisers and clients could use to speak about risk, built around their “risk number.” Clients, even those who are relatively sophisticated, rarely want to talk about Sharpe ratios and standard deviations, let alone the several other variables that go into calculating risk. Sometimes the best ideas are the simple ones, and the risk number was/is beautifully simple at putting risk at the center of the conversation with prospects and clients. Which over time, Riskalyze expanded to an ever-growing suite of capabilities built around that risk number core, from stress tests to retirement projections to ongoing client check-ins.

However, Riskalyze has reached a difficult spot in its journey. The good news is that according to the latest T3 Tech Survey, Riskalyze holds a dominant market share in the risk tolerance category. Notwithstanding that lead, it still has ample room to grow, as risk tolerance software remains one of the lowestcategories of AdviserTech adoption (at just 41% market penetration), in a world where just using a homegrown questionnaire (or a purely “conversation approach” where the adviser just talks to the client about risk and makes a judgment call about what to implement) still hold the majority market share. In other words, apathy is still the biggest competitor to a solution like Riskalyze, which provides more opportunity for upside, but likely also some frustration for the leadership at Riskalyze, which probably would have thought it would be more of a staple in the conversation today in the same way that CRMs, financial planning, or portfolio management are (which all enjoy ~70%-90%-plus market adoption). Instead, though, while Riskalyze’s growth has been remarkable, they have been forced into a place where they need to expand the platform into adjacent lines of business to continue growing, quickly moving them from a place where they had very little competition only a few years ago to now where every new domain they tread into is an already crowded space with heavyweight incumbent competition.

At the same time, Riskalyze’s growth story within the risk tolerance category has also faced an onslaught of competition, with risk tolerance having long been the area of the Kitces AdviserTech Map with the highest concentration of newcomers, all seeking to emulate (and compete with) Riskalyze’s success. This year saw a new level of competition as now very well-funded established players, like Morningstar with its new Portfolio Risk Score and Orion’s 3D Risk Profile, seem to be trying to cut Riskalyze off by offering similar functionality for no additional cost as an extension of their existing platforms.

In that vein, it is perhaps no surprise that Riskalyze is taking the next step in its own growth journey, announcing a “recapitalization” by Hg for what was reportedly a $300 million-plus valuation. It is peculiar that there has been such an emphasis placed on calling this a “recapitalization” rather than an acquisition, which isn’t a term used often for these types of deals, and suggests it may have been as much about getting former PE firm owner FTV Capital out (along with early investors who may have wanted their own exit after nearly 10 years), as opposed to taking a significant round of new growth capital. No matter what it’s called, it's another successful liquidity event in the adviser technology landscape for a company that carved its own path.

The broader question is simply where Riskalyze looks to go next, as expanding adoption within the risk tolerance category remains steady but slow, and competitors like Morningstar and Orion are offering their own free tools to take up the apathetic market share (who haven’t been willing to pay for a solution but may be won over “for free” and be taken out of Riskalyze’s future market opportunity).

Given Riskalyze’s building of its autopilot trading tool, at least one option would be to jump into the emerging direct indexing wave. Combining the Riskalyze risk number with the autopilot trading experience and a direct indexing engine to allow advisers to further customize (for their own investment preferences, or the client’s individual-specific tolerance constraints) could be a very unique way to build customized portfolios that are still centered around Riskalyze’s risk framework. Alternatively, to the extent that Riskalyze takes on at least some new capital, it may also use some of its new powder to acquire a performance reporting company and begin to grow inorganically to further extend toward Orion, Black Diamond and Tamarac. Or given Hg’s own roots in Europe, it’s possible that the next stage of Riskalyze growth has nothing to do with the U.S. at all, and instead will leverage Hg’s connections and expertise to be introduced into the relatively less-competitive European adviser markets instead.

Only time will tell, but either way Riskalyze deserves acknowledgment and congratulations for its latest round. Building something from scratch is incredibly difficult, and while some AdviserTech solutions in recent years have seen incredible exits and valuations (e.g., MoneyGuide, Orion, etc.), Riskalyze is the largest AdviserTech exit to come in the post-financial-crisis fintech boom, launched at the same time that robo-advisers first appeared, with a bet that human advisers would win out over the robots. It was a bet on human advice that served Riskalyze and its investors incredibly well!

One of the biggest themes of AdviserTech in recent years has been consolidation, as the number of unique companies on the Kitces AdvisorTech Map has exploded to more than 300, and a growing number of incumbents have sought to acquire up-and-coming (or even more established) AdviserTech solutions, from serial acquirers like Envestnet, Orion and Morningstar to more strategic acquirers like AssetMark, Fidelity and most recently even Vanguard.

In all of those scenarios, the common theme was that the incumbent had an existing presence and market share in some portfolio or asset management category and acquired adjacent AdviserTech solutions to expand and round out its ever-growing platforms to become more full service. By contrast, Tifin Group has been a relative newcomer in the world of AdviserTech consolidation, purchasing a number of smaller AdviserTech solutions before they substantively gained traction (and the higher price tag that comes with it).

At the least, Tifin ostensibly hopes that by investing into the often undercapitalized AdviserTech startup (so often created as a “homegrown” side project by an adviser who sees a gap in their own practice, and builds technology to solve it, but may not have really been prepared to grow and scale a tech solution), it can help companies that may have never gained traction on their own to do so. At best, though, Tifin appears to be hoping that it can piece together enough components of the AdviserTech stack to cobble together its own full-breadth adviser platform (which thus far includes Clout for digital marketing, Totum for risk tolerance, and Magnifi for investment analysis), where the whole has the potential to be worth even more than the sum of the parts.

Yet ironically, one of the hottest emerging categories of AdviserTech is not just helping advisers run and scale their businesses with technology, but helping them get the leadsin order togrow. For which Tifin Group has been allocating its capital by trying to acquire digital media platforms that may have limited opportunity to monetize asmedia, but can become very lucrative as adviser lead generation platforms that connect to Tifin’s technology (via FinancialAnswers.io) to help facilitate engagement with prospects until they’re ready to engage with advisers directly.

And now, with Ian Rosen (former CEO of StockTwits) at the helm, Tifin has acquired another media property, StockNews, under its FinancialAnswers.io brand.

On the surface, the audience of StockNews is highly engaged. It’s a solid platform to quickly consume market movement by all interested parties, and identify which stocks have momentum. Under the surface, there are millions of people who do their research, pick their investment choices, or even discover professional financial advice via channels like StockNews. Which drives the lead generation opportunity for Tifin.

At the same time, even further underneath the surface, Stock News has a very solid API for its content. The API consists of news about specific tickers, general market news, sentiment, sectors, etc. One can start to imagine how that becomes powerful to Tifin portfolio company Magnifi, which is trying to help create a better, more personalized search engine for investment products, or Clout, which is aiming to create a content marketing platform for advisers, or Farther, which is also trying to (algorithmically) help match clients to advisers. In other words, the type of data that StockNews collects and distributes is fuel for all of these portfolio companies, all while adding value on its own to the Tifin media group and Financial Answers for lead generation.

There are no silver bullets to building a singular successful offering for financial advisers, and ironically it can actually be more difficult for platforms to gain adoption when they start out as more comprehensive, because it increases the complexity and switching costs for the prospective adviser, who must change out everything at once. Nonetheless, the reality is that as growth continues to be the No. 1 goal and the No. 1 struggle for most advisory firms, by anchoring itself to a lead generation channel, Tifin arguably has the potential to attract advisers with the outright lead-gen growth opportunity, which can make them more willing to go through the necessary change to adopt Tifin’s tools when the ROI is not just the efficiencies of tech, but an attached growth engine — at least, if TIFIN can actually figure out how to successfully convert at least some of the traffic from non-adviser-centric DIY-oriented media platforms into the kinds of delegators who hire financial advisers?

It’s hard to look anywhere these days and not see the looming impact of cryptocurrency and blockchain, from the recent rise of NFTs (non-fungible tokens), to the daily media buzz about the price of Bitcoin and the cost of buying a new computer (and the limited supply available) as a result of a crypto-induced shortage of high-speed video cards. That not only has clients swimming in conversations about crypto — that they inevitably bring as a question to their adviser — but increasingly is putting advisers themselves on the spot to at least have a better understanding of and answers for their clients’ crypto questions (even if they’re not yet looking to invest in crypto on behalf of their clients).

Enter OnRamp, which this month announced a new $6 million venture capital round to continue to grow its crypto solutions for financial advisers. At the heart of OnRamp’s mission is education via OnRamp Academy. There has been a core belief that even if advisers themselves are not interested in crypto or investing in it, they need to be able to discuss it with their clients, or risk being left behind. Every day, the amount of people who have some slice of their net worth allocated to crypto, whether it is 0.01% or 100%, grows. Which means advisers need to be able to have informed discussions and provide holistic advice about a client’s entire investment holds, and that advice needs to go beyond, “I think crypto is too risky to invest in.”

Notably, though, OnRamp has indicated that it’s building out a crypto portfolio management offering, going beyond just education alone. Thus far, the platform has begun to build out integrations to crypto custodians — which help advisers track their clients’ held-away crypto assets in existing performance reporting tools — and is now looking to build out trading, with future capabilities on the road map to facilitate billing, performance reporting and cash management. Which is important, because there is significant complexity in direct ownership of cryptocurrency like Bitcoin, given the need for each client to maintain an individual crypto wallet with a private key.

Ultimately, there is still a great deal of speculation about whether or not the traditional portfolio management companies will get into the cryptocurrency space — presenting a major competitive threat to OnRamp just as it tries to get off the ground. Alternatively, there’s the possibility that a traditional asset manager simply acquires OnRamp when it starts to show traction, akin to the way that Vanguard acquired JustInvest as the direct indexing trend was showing more promise, but JustInvest hadn’t scaled to a large size just yet. Still, though, the “outcompete or be acquired” calculus isn’t always that simple. For instance, many thought the same thing about Asset-Map when it launched; why wouldn’t financial planning companies just add this kind of mind-mapping data-gathering capability to their existing offerings? Well, they didn’t, and Asset-Map has quickly grown to a sizable market share with strong user ratings as it pioneers a new planning-software-adjacent category. Add in the complexity and charged nature of crypto, and it’s easy to see a wide range of potential outcomes for OnRamp.

Nonetheless, as long as the focus on and interest in cryptocurrency continues to grow, the tendency is for a rising tide to lift all boats. With $6 million of fresh capital in the coffers, OnRamp now has a healthy runway to build to the next stage of growth and begin its pivot from just adviser education into (crypto) asset management. The only real question is whether advisers themselves will decide to begin taking the crypto plunge… and/or whether the potential rise of Bitcoin ETFs will lead to advisers to eschew direct-held Bitcoin and simply buy a small slice of cryptocurrency in a traditional ETF wrapper instead.

The 2010s is proving to be the decade when “risk” tools really became central to the adviser technology stack. Of course, the reality is that regulators have imposed a know your client obligation for decades, and while the decade did begin in the shadow of the financial crisis (which put “risk” in a whole new light for many investors and advisers), it’s certainly not the first time that there have been challenging, volatile markets. Consequently, it appears that the rise of risk as a focus of the 2010s was less about the need to assess risk or the fact that markets deliver it from time to time, and more about the commoditization of investment management that increasingly drove advisers to define their value proposition not just in terms of trying to generate portfolios with superior investment performance, but trying to help clients behaviorally to not personally underperform the potential of what markets can provide.

In practice, this meant both developing better tools to assess risk tolerance (witness the rise of Riskalyze) and better tools to understand the risk(s) that a portfolio was really taking, with a growing number of AdviserTech tools providing more capable investment analytics for ever more unique ways to assess risk in a portfolio, from the rise of stress-testing tools like Hidden Levers and MacroRisk Analytics, to focused risk analytics tools like FactorE, Chaikin and Portfolio Visualizer, and increasingly institutional-grade analytics like BlackRock’s Aladdin.

And now, after more than a year of developing the software, Fabric RQ announced that it has raised a seed round, bringing yet another risk tool onto the market this fall. Fabric RQ is taking the Aladdin route to market, it seems, touting its institutional pedigree in the domain of risk analytics (and a desire to bring those capabilities to advisers).

Notably, Fabric was co-founded by Rick Bookstaber. Rick is no stranger to risk, as he has had a prominent career, most notably helping Ray Dalio’s Bridgewater Associates navigate the financial crisis of 2008, joining the Obama administration to work on the Financial Stability Oversight Council and then serving as chief risk officer at the University of California. In the Fabric teaser video, Rick says that “risk is the fabric of the financial universe,” something that, like the universe itself, we are still developing more tools to understand.

The caveat, though, is that while risk is everyone and in need of being better understood, financial advisers, by and large, create broadly diversified portfolios, where the diversification itself is meant to smooth out the risk. In other words, adviser portfolios — with their broad asset-class-based exposure, longer time horizons, and (typically) lack of any leverage — don’t havethe same depth of risk concerns as institutions in the first place, at least, outside a subset of the largest mega-RIAs with tens of billions of AUM that may have the depth of investment-team capabilities to be able to delve deeper into more nuanced and sophisticated risk analyses. And from the client perspective, a conversation about risk between advisers and clients that relies on such in-depth risk analytics has the potential to derail any productive conversation, as clients can feel lost or confused.

Bookstaber claims that institutions have had an “unfair advantage” over advisers for years when it comes to their ability to analyze risk, and Fabric is aiming to change that. And arguably, it is only a good thing for investors and the industry that risk becomes more of the fabric of the conversation. Nonetheless, as advisory firms increasingly shift their value proposition to generating more gamma with behavioral management of clients with less focus on pure alpha, and wealth management and financial planning itself become more and more central to the adviser value proposition, the question arises: Will Fabric be able to entice advisory firms to take a deeper look at the more complex and nuanced aspects of risk that require institutional-grade analytics to evaluate, or will advisers simply opt to build ever-more diversified and simpler portfolios for clients as their value proposition shifts elsewhere, obviating the need for such risk analytics tools in the first place?

One of the least appreciated drivers of trends in the asset management industry is the intersection between what asset managers have to offer, and what financial advisers find they’re able to sell to their clients in order to differentiate and distinguish themselves. That’s why mutual funds grew in the 1980s and 1990s (as financial advisers sold professionally managed mutual funds to differentiate themselves from legacy advisers still selling individual stocks), and why ETFs grew in the 2000s and 2010s (as financial advisers differentiated themselves from mutual funds by using ETFs as their new portfolio building block). And now as ETFs increasingly become the dominant destination of adviser flows, their near-ubiquity is leading to a hunger for the next investment differentiator, leading to the rise to direct indexing, which allows advisers to distinguish themselves from their ETF-using brethren by showing a more customized and personalized version of portfolio construction.

Thus far, true portfolio personalization is in an early stage, and one that necessitates new forms of portfolio management technology to handle the complexity of doing so at scale across dozens, hundreds, or thousands of clients at a time. Which is why in practice, the rise of direct indexing has been less an asset management story thus far, and primarily an adviser technology story instead, spurring a slew of recent deals including JP Morgan acquiring 55IP and OpenInvest, Fidelity investing in Ethic, and Vanguard acquiring JustInvest. In essence, the direct indexing move seems to be creating just enough fear for the large asset managers that they are proactively scooping up offerings showing any promise, before they become real threats, and can instead be leveraged bythe asset managers instead.

At the same time, though, a number of asset managers that already offer separately managed accounts are beginning to build their own homegrown technology to manage direct indexing portfolios, such as Canvas by O’Shaughnessy Asset Management, which quickly grew to more than $1 billion in AUM in barely a year.

And now, another direct indexing SMA — Veriti — has announced its own crossing of the $1 billion AUM threshold (which they claim was driven entirely by word of mouth and referrals), after similarly evolving from an internal offering within an advisory firm that was managed with its own technology to become a third-party direct indexing offering for other advisers.

What continues to be compelling about these solutions is how they are applying the tech to scale, and bringing solutions that were typically reserved for very high-net-worth investors, as legacy direct indexing players like Parametric and Aperio started in the ultra-high-net-worth domain, and technology newcomers like Wealthfront began to use technology to democratize direct indexing and bring it down market in the 2010s. Accordingly, Veriti is currently offering its direct indexing solution for anyone with at least just $250,000, and anticipates that number will come down further soon.

Ultimately, it remains to be seen whether direct indexing will become the trend that topples ETFs and mutual funds, but with one new asset manager after another posting $1 billion-plus of inflows in just a year or a few years after launching, direct indexing is clearly moving beyond a fad into a full-blown trend. And in this case, it appears that asset managers themselves are becoming one of the biggest drivers, showing a willingness to disrupt themselves before technology newcomers do it to them. In the end, though, anticipate that the line between separately managed accounts and direct indexing will continue to be blurry — if only because the asset management industry would far prefer to charge basis points as a direct indexing SMA than software user fees as a technology solution. And given the sheer complexity to manage — and especially to execute the trading of — direct indexing at scale, it seems likely that advisers will be willing to outsource the raw direct-indexing implementation for a reasonable fee.

The bottom line, though, is simply to recognize that when advisers feel pressure to differentiate themselves, they will move on to the next big thing in order to distinguish themselves in client conversations from what everyone else is doing. Which means, ironically, that while portions of the asset management industry are still reeling with the adviser shift from mutual funds to ETFs, the rapid growth of ETFs over the past decade, coupled with the rise of robo tools to manage portfolios at scale, means the next adviser shift in portfolio management is already getting underway!

When Altruist first launched as an RIA custodian back in 2018, it set out to distinguish itself with the robo-style technology interface and onboarding capabilities that advisers had been clamoring for (but traditional RIA custodians had failed to deliver on) for a mere $1/account, coupled with an appealing zero-commission trading platform to implement with clients. The idea was that with venture capital support, Altruist would ultimately grow and scale to the point that it could generate enough revenue from the other economics of the custody and clearing business, leveraging its technology to be internally so efficient that it could be both the lower-cost custodian and the lower-cost portfolio management software solution.

The caveat, though, is that advisers generally have very high expectations of the full breadth of capabilities that an RIA custodian must bring to bear to win their business, and the widespread adviser fear of the hassles and client risk of repapering means that advisers can be veryslow to change to new solutions, often opting to adopt new platforms with their newclients but refusing to move many or any of their existing clients. Which can severely slow the growth of new (and existing) RIA custodial competitors.

In the context of the broader industry, these trends have led to a growing focus on capturing a market share of new RIAs — in particular, the breakaway broker movement, which actually canput billions of AUM in motion all at once — and a trend toward mergers and acquisitions as RIA custodians try to gain ever-more scale to bring down their costs (most notably, with Schwab acquiring TD Ameritrade).

Unfortunately, though, Altruist doesn’t necessarily have the capital it would take to acquire another RIA custodian and it hasn’t yet built the depth of service and support capabilities to attract the large breakaway broker teams (that tend to prefer more established household names, having come from a big firm brand). That has led the firm to push more toward independent brokers transitioning to independent RIAs (who have to repaper to leave their broker-dealer anyway), new startup RIAs beginning from scratch (who have no repapering because they have no clients yet), or lifting their revenue peradviser by being able to monetize more than just the custody/clearing layer alone.

In that context, it’s notable that last month, Altruist announced that it had hired away Adam Grealish, the now-former head of investing at Betterment. That’s significant because a pure RIA custodian or a standalone technology company wouldn’t necessarily need its own head of investing. What kind of business does need a head of investing on staff? A TAMP.

Notably, Altruist founder Jason Wenk is no newcomer to the TAMP business; in fact, he’s the founder of FormulaFolios, which quickly grew over the past 10 years to become a nearly $3.5 billion AUM TAMP itself.

By turning Altruist into a(nother) TAMP, Wenk has the opportunity not only to expand the economics of Altruist itself — capturing the asset management revenue layer on top of the custodial and technology layers — but as a “vertically integrated TAMP” that offers TAMP services with greater internal efficiencies (by building its own technology directly down to the custodial roots), and its own proprietary technology to offer a differentiated client- and adviser-experience, while capturing the underlying custodial revenue opportunity. Which would put Altruist in rarefied air alongside the likes of AssetMark and SEI, which similarly offer TAMP services built on top of their own (self-)clearing capabilities.

More generally, though, it’s worth recognizing that the evolution of Altruist itself highlights the ever-blurring lines between the industry’s labels and layers (e.g., TAMP, RIA custodian, etc.). As Wenk himself emphasizes, Altruist is trying to combine the best elements of established financial services institutions (from RIA custodians to asset managers) and the tech savvy of robo-advisers, which helps to explain why it has priced as tech (at $1/account), even as it has driven its revenue model as a custodian, is launching a TAMP, and in practice is built on topof another clearing firm (Apex).

In the end, advisers do need a lot of elements to serve their clients, and it’s well documented that a lot of those elements currently do not integrate very well. Because traditionally, each layer had to build integrations to one another, while again, Altruist is effectively building the vertically integrated stack that captures it all. In other words, it seems as though Altruist is trying to become a sort of glue between the best parts of the traditional financial services industry and the new disrupters.

People want and need financial advice. They want a human to guide them through life’s biggest decisions. The core elements of advice remain unchanged: Clients have dollars that need to land somewhere and be invested, while receiving advice on their entire financial picture (beyond the portfolio alone), and the adviser needs the tools and platform to do so efficiently. How those elements are all delivered may change, but they will always be required.

Having someone who knows how the new disrupter was thinking about an investing platform (as Grealish moves from Betterment to Altruist) to support the vision of an Altruist as a next-generation TAMP-cum-custodian will be a powerful combination to increase their revenue/adviser as they continue to try to grow and scale in the hypercompetitive world of RIA platforms!

When robo-advisers first showed up nearly 10 years ago, their stated goal was to use technology to replace the human financial adviser at a fraction of the cost, and they made the case that financial advisers were charging an arm and a leg and that the true cost of financial advice should be no more than 0.25%. In practice, not only have financial advisory fees ‘failed’ to decline in the decade since, but recent Kitces Research shows that financial advice fees are actually on the rise as financial advisers reinvest in a more holistic financial planning value proposition. Not to mention that — as most robo-advisers themselves discovered — one of the biggest drivers of high financial planning fees is not actually the cost to deliverthe advice, but the client acquisition costs to getthe client in a hypercompetitive market in the first place.

In fact, because of the significant challenge in simply getting clients — where the average client acquisition cost among financial planners is more than $3,100 per client — the irony is that the greatest disruptive threats to financial advisers appear to come not from technology startups, but incumbentsthat aim to leverage technology, coupled with sometimes immense existing networks of customers, to compete against the mass of smaller independent advisory firms that don’t have the marketing size and scale to compete. Accordingly, in recent years, firms like Vanguard have launched a Personal Advisor Services platform offering technology-enabled human financial advisers for a fee of just 0.30%, and both Schwab Plan and Bank of America Life Plan have gone so far as to begin offering an entirely freecomprehensive financial planning software for their existing customer to use to do planning for themselves.

Of course, the reality is that simply providing consumers with the information they need to improve their financial lives isn’t necessarily enough; while some people can simply take new knowledge and apply it, for most, the real secret to behavior change is not simply learning new information, but figuring out how to change their mindset and how to break old habits for new ones. Which is a domain that is uniquely suited to working with a human financial adviser, as it’s often the human-to-human connection that fosters the level of accountability we need to actually change our behaviors.

However, for many financial advisers, the truth is that they’re not necessarily built to engage clients in ongoing efforts to help them change their behavior; instead, the value of the financial planner is often in the financial plan itself — as advisers utilize sophisticated financial planning software that is not generally accessible to the consumer, conducting analyses that clients simply couldn’tdo on their own. For which the adviser is paid as the pathway for the input (in the form of data collection) and the output (in the form of a plan presentation).

In this vein, it’s notable that last month, American Express announced that it was partnering with BodesWell, a startup on a mission to build financial planning software that consumers can use themselves withoutneeding to go to or through a financial adviser. In the initial six-month pilot, American Express will roll out BodesWell — in a white-labeled offering called My Financial Plan — to 25,000 existing American Express cardholders, providing them both a personal financial management dashboard leveraging Plaid for account aggregation, and tools to help them set and then monitor their progress toward various goals (from buying a house to saving for retirement). All of which will be provided to Amex cardholders for free. (At least for now.)

From the American Express perspective, the move into financial planning is notable because American Express was arguably the OG of large financial services firms offering financial planning when it acquired IDS Financial in the 1980s (subsequently rebranded as American Express Financial Advisors), and become one of the first broker-dealers to lead with a comprehensive financial plan for which they charged a stand-alone fee (in a world where everyone else gave the financial plan away for free in the hopes of getting paid with the subsequent sale of a mutual fund or an insurance policy). Yet AmEx ultimately decided to exit that business — spinning off the entire financial adviser business into what is now known as Ameriprise in 2005 — to focus on its credit card business. And so AmEx’s (re-)entrance into financial planning is arguably just a return to a strategy that the company has already proven can work, leveraging its massive network of (typically above-average affluence) premium cardholders to cross-sell financial services. The only question at this point is how, exactly, AmEx will aim to monetize its new financial planning offering, from starting to charge for financial plans, upselling to human financial advisers, or adopting a model more akin to Personal Capital where it simply identifies those who account-aggregate a significant amount of portfolio assets and contact them about rolling over to an AmEx advisory account.

From the broader industry perspective, though, the real significance of the AmEx-BodesWell partnership is that just as financial planning fees begin to rise, new competitors with immense scale are aiming to leverage technology to bring those fees back down. Or, as Jeff Bezos famously quipped, “your [sizable profit] margin is my opportunity,” from the free Schwab Plan to the free Bank of America Life Plan and now AmEx’s free My Financial Plan. The fact that the shift is now being accelerated by American Express — one of the early pioneers of charging for financial plans and notgiving them away for free — makes the situation somewhat more ironic. Though it is not entirely new, as American Express itself championed charging for financial plans in a world where everyone else was giving them away for free. Which means in the long run, it’s not clear that AmEx (and Schwab, and Bank of America) will necessarily cause any kind of collapse in the fees that financial advisers charge. But it does highlight that advisers will find it increasingly difficult to just rely on the sophistication of their financial planning software itself to demonstrate their planning value, as the software tools become more and more accessible to consumers directly. Instead, financial advisers increasingly will have to compete with the more specialized expertise and the behavioral counseling they can provide on topof what the software will be able to do for free?

One of the greatest ironies of modern financial planning software is that it’s not actually very good at formulating a true plan. Ultimately, the whole point of a planis to determine in advance an anticipated course of action to handle an unknown future; if A happens, we’ll do B, but if X happens, we’ll do Y instead. So regardless of whether A or X actually happens, there is a planfor what to do in response. In practice, financial planning software requires that all inputs be set in advance for the duration of the plan; the prospective retiree is projected to spend some set amount each year, and may change that spending based on certain goals (e.g., spend more in the first 10 years with active retirement travel, add dollars to the portfolio when the vacation house is sold at age 80), but can’t actually adjust spending to plan for the biggest uncertainty: the market itself.

This limitation stands in stark contrast not only to real human behavior — when markets and wealth decline, consumers tend to tighten their belts, and when the markets are on the rise, there is a wealth effect that leads to rising spending — but also fails to take into account the retirement research itself, which shows that even just relatively modest adjustments to retirement spending in the face of volatile markets can get a retirement plan back on course. In fact, once it’s recognized that retirees can and do change their retirement spending in the face of declining wealth, the entire concept of a Monte Carlo “probability of success” is no longer relevant, as in the end every plan can succeed at not running out of money, and Monte Carlo probabilities of 50% or even lower are viable; the only questions are how likely it is that the retiree may have to make adjustments tothe spending along the way, and how big those adjustments turn out to be.

To fill this void, several years ago a new crop of retirement decumulation planning tools began to emerge, like Big Picture App and Timeline, that applied a more dynamic, rules-based framework to retirement plans. For instance, advisers could actually model decumulation plans in which retirees would ratchet their spending higher as markets grew, or simply keep their spending between4% and 6% withdrawal rate guardrails — raising their spending in bull markets, and trimming in bear markets — and showing not their probability of failure (which is a moot point when spending is cut in a bear market), but instead the frequency and magnitude of spending cuts that they might have to make along the way. That in turn is leading to the rise of new vendors like Income Lab, which is aiming to establish new types of guardrail approaches, and in turn, reinvent how retirement planning results are delivered in a world where “probability of success” is no longer the most relevant metric.

The caveat, though, is that financial advisers who tend to delve this deeply into decumulation planning for their retiring clients tend to be the more comprehensive financial planners, who already use traditional comprehensive financial planning software, and don’t necessarily want to do double data entry into a specialized decumulation tool as well astheir existing planning software. Nor do they want to explain why the output of one software may not precisely match the other (which is virtually inevitable, given differences in underlying assumptions and the underlying calculation engines themselves).

In this context, it’s notable that last month RightCapital announced the launch of a new dynamic retirement spending module, within RightCapital itself, that advisers can use to set guardrail thresholds above (or below) at which the retiree is assumed to increase (or decrease) their retirement spending to stay on track. That in turn is layered on top of RightCapital’s capabilities to do tax-sensitive retirement withdrawals and illustrate partial Roth conversions to fill the lower tax brackets, both of which are strategies that are also dynamic and can shift based on the variability of future market returns.

RightCapital’s approach is also notable in that for the past several years, competitors like MoneyGuide and eMoney Advisor have focused heavily on making simpler planning software tools (e.g., MyBlocks and Foundational Planning, respectively), while RightCapital has gone in the opposite direction and moved upmarket into more complex and sophisticated planning capabilities (for which Kitces Research has shown rising demand). Which positions RightCapital well as advisers increasingly charge stand-alone planning fees and/or frame their value in terms of financial and retirement planning (not investment management), and need increasingly sophisticated planning software to demonstrate their planning-centric value proposition.

As advisory firms increasingly struggle to differentiate themselves in an environment in which more and more advisers offer the same (comprehensive wealth management) services targeting the same (fairly affluent) clients, more and more advisory firms are showing a willingness to spend real dollars to generate new clients, leading to a veritable explosion of paid lead generation platforms on the Kitces AdvisorTech Map, from SmartAsset’s SmartAdvisor to Zoe Financial to Harness Wealth. That in turn is attracting new entrants to the category, most recently including Planswell.

Notably, Planswell is not entirely new to adviser lead generation… just a new player in the U.S. Having started in Canada as a direct-to-consumer offering that combined a robo-investing service along with insurance and mortgage products, the company nearly collapsed after “anonymously published allegations of sexual harassment made by a former Planswell employee against a company co-founder” resulted in a failure to secure its next round of funding, initially shutting the venture down entirely. It was revived in early 2020 as a more focused free financial planning software tool for consumers that then provided prospects’ information to a third-party human financial adviser to reach out and invite the individual to go further. The company then announced in late 2020 it was expanding from its Canadian roots into the even-larger U.S. market.

The appeal of the Planswell lead generation model, relative to other adviser lead generation services, is that prospects engage with the Planswell planning tools — rather than simply expressing that they’re interested in learning more about working with a financial adviser — which both provides an opportunity to better qualify the prospect before reaching out (if they’ve actually entered their financial information into Planswell), and in general has the potential to produce more engaged prospects (as those who are willing to go so far as to utilize more comprehensive self-directed planning software presumably have some real pain point they’re trying to solve for that an adviser may be able to meaningfully help with). The caveat, though, is that means the advisers become more directly tied tothe Planswell financial planning software — as prospects have already been anchored into an initial client experience through Planswell, and may be concerned if the adviser subsequently uses different planning software that produces different results — which means that Planswell cannot simply provide leads, but instead needs to engage advisers more deeply into its own ecosystem.

Accordingly, this month Planswell announced the launch of a new Plancraft offering that would move the platform from just a lead generation service into a more holistic practice management offering. The offering includes access to the Planswell financial planning software, weekly educational webinars and other live events, as well as formulating study groups of eight to 10 advisers for facilitated peer learning, to help them best leverage the Planswell planning software and lead generation service, for a total cost of $449/month (including $199/month for the Plancraft platform plus $250/month for the first 10 monthly leads).

From the adviser perspective, bundling together an educational and planning software offering to its lead generation service will likely make Planswell more appealing to newer advisory firms that haven’t already committed themselves to other planning software (as larger firms typically already have an existing adviser technology stack, and more often want to just pay for qualified leads), or firms that solely provide investment management or sell insurance and annuity products that simply don’t have any kind of planning software and could expand their services through Planswell. Though to the extent that Planswell’s offering is anchored around its lead generation service, in the end, as with any lead generation service, advisers will ultimately judge the offering by the quality of its leads — which remains to be seen, as Planswell expands its Canadian marketing roots into the more-crowded U.S. marketplace.

From the broader industry perspective, Planswell highlights both the opportunity and challenge of building more proprietary planning and other engagement tools as part of a lead generation service. On the one hand, doing so creates an opportunity to more deeply qualify and engage prospects, with the potential to improve lead quality. On the other hand, when adviser software switching costs tend to be high in the first place, the more all-in an adviser has to be, the harder it often is to gain traction and adoption in the first place?

One of the primary criticisms of financial advisers and the AUM fees they charge is that it’s difficult for an adviser’s portfolio choices to beat the market, which means an adviser-managed portfolio will inevitably underperform the index by the amount of their fees, which can add up to more than a quarter of the portfolio’s value over a multidecade period of time. At the same time, the truth is that not all investors can earn the returns of the market without an adviser, not because they don’t have index funds available to purchase, but because at least a subset of investors struggle to stay invested as markets turn volatile, producing a “behavior gap” between the returns of the index itself and the returns that investors receive for themselves after their trading. Which, in the aggregate, can cut their returns and future wealth by far more than just paying a financial adviser to help them stay the course.

However, the reality is that the biggest impact for the average American’s financial wealth accumulation over time is not the returns they earn on their savings (net of the adviser’s fees or their own investor behavior gap); it’s whetherand how muchthey save (rather than spend) in the first place. Which is driven not by our portfoliobehaviors, but our broader moneybehaviors, and the “scripts” that run in our heads and guide our relationship with (and decisions about) money.

In fact, Drs. Ted and Brad Klontz have found that most people have one of four money scripts that run through their heads and guide their financial decisions: money focus (money is critical for happiness, leading to a desire to always accumulate more money for more happiness); money status (our net worth is a reflection of our self-worth, and wealth must be shown in order to show one’s worth); money vigilance (money is accumulated through saving and working, and shouldn’t just be handed out); and money avoidance (money is evil, which means that less money is better than more, leading them to tend to spend or give away money rather than accumulate it). The researchers developed the Klontz Money Scripts Inventory (KMSI) to help assess the extent to which our financial decisions are being impacted by one of these four money scripts.

In practice, though, the KMSI has been used primarily by psychologists and therapists specializing in financial issues, and not necessarily by financial advisers. But now, DataPoints — which provides a number of financial psychology assessment tools, stemming from co-founder Sarah Stanley Fallaw’s research with her father (Thomas Stanley, of “The Millionaire Next Door”) on the behaviors that predict wealth accumulation — has announced a new partnership with the Klontzes to make the KMSI assessment available directly to financial advisers through the DataPoints questionnaire platform.

From the financial adviser perspective, the availability of tools like the KMSI through DataPoints gives a new opportunity to delve even deeper into understanding whyclients may be engaging in certain (positive or not-so-constructive) money behaviors, which can provide insight into why some clients tend to spend down their wealth while others struggle to enjoy it at all, why some tend to struggle to even save and build wealth in the first place while others can’t stopdoing so, and why some client couples (who have substantively different money scripts from each other) may be struggling to create alignment for their own financial planning goals.

From the broader industry perspective, DataPoints is becoming an increasingly active player in the rapidly growing AdviserTech Map category of Behavioral Assessments that go beyond pure risk tolerance to understand a client’s broader financial psychology, just as the CFP Board itself is incorporating financial psychology as a new Principal Knowledge domain of the CFP curriculum. Not that it isn’t important for financial advisers to help clients stay the course with their portfolios in the midst of market volatility. But as financial planning expands beyond the domain of products and the AUM model to serve a wider range of clients, so too will the demand for behavioral assessment tools that help advisers help their clients across the full spectrum of their money behaviors.

From the financial adviser perspective, one of the most surprising aspects of the coronavirus pandemic is how little the pandemic has actually impacted the advice business, as the explosion of adviser technology over the past 20 years enabled advisory firms to operate smoothly on a virtual work-from-home basis, and the ubiquity of Facetime and webcams has even allowed advisers to stay connected to their clients virtually. However, when it came to the world of adviser conferences, the virtual transition was not nearly so smooth. The pandemic shut down all in-person conferences in the second half of 2020, to what was widely viewed as a lackluster transition to online conferences, not just for advisers themselves but especiallyfor adviser technology exhibitors who found it almost impossible to connect with attendees in the virtual exhibit hall.

From the AdviserTech perspective, the significance of this disruption to traditional adviser conferences is that technology vendors lost one of their most popular marketing channels, in a world where advisers — especially independent advisers who are appealing to reach because they have the fastest sales cycle for the adoption of new technology — are extremely fragmented, and conference events were one of the few opportunities where technology could be showcased at once to a large number of advisers aggregated together.

But as the saying goes, “Necessity is the mother of invention.” In many cases, vendors simply decided that if the future of event marketing would be virtual, they would take control of their own fate, purchasing adviser email lists from third-party vendors like Discovery Data and RIA Database, procuring their own speakers who can attract a good adviser turnout, and running their own webinar marketing — which in many cases actually generated far more leads (as many vendors are lucky to collect a few dozen adviser business cards at an in-person event, but can potentially get hundreds of sign-ups for an adviser webinar on a popular topic), and at a lower cost (as paying for a webinar platform and a speaker directly is still often less expensive than an in-person conference exhibitor booth, especially when adding in the cost of shipping booth materials and travel and accommodations for the sales team).

Adam Holt, the founder of Asset-Map, went one step further as virtual conferences struggled in the fall of 2020 and launched AdviceTech.LIVE, which was billed as a “virtual showcase” of adviser technology that intentionally went light on the exhibit hall approach, opting instead to simply make technology demos part ofthe conference agenda itself; in other words, if the intention of an adviser technology conference is for advisers to find new tech solutions and vendors to showcase what they have to offer, why not simply make thatthe agenda of the event in the first place. While traditional conferences in the virtual format have struggled with their virtual exhibit halls because advisers who come for the education don’t necessarily want to go to the exhibit hall to shop for solutions (as they weren’t attending for solutions, they were attending for education!), an event that is intendedto help advisers shop for their technology can simply make tech demos front and center! Which works just fine in a virtual format!

Now the contrast of virtual versus in-person technology conferences has been put into sharp relief as the resurgence of the delta variant of Covid-19 led to the 2021 return of an even-larger AdviceTech.LIVE event, just as the T3 Advisor Technology conference was forced to cancel its 2021 return to an in-person event — ironically, announcing the news on the very day that AdviceTech.LIVE was hosting its own virtual event — and reschedule to a yet-to-be-determined date in the spring of 2022. Which in turn raises the question of whether in-person events like T3 will be able to recover, or will the future of AdviserTech conferences be entirely virtual?

Ultimately, I anticipate that the T3 Advisor Technology conference will be back, and will be successful — conference headwinds notwithstanding — because the reality is that T3 is less of a conference (where advisers go to get education), and more of a trade show (where the adviser technology industry at large comes together). In fact, the reality is that the T3 conference has never had a huge turnout of advisers (numbering only in the hundreds, while events like Schwab IMPACT see attendance in the thousands), and few vendors generate a strong ROI on their exhibitor fees solely from the new adviser users they gain from participating. Instead, T3 has long excelled as a place for technology vendors themselves to connect (with a number of key integrations, and even mergers and acquisitions, having gotten their start at T3), a place for industry consultants to get a handle on the latest and emerging trends (which are carried back to the enterprises they consult with), a place to interact with the small-but-important set of AdviserTech early adopters who help to drive those trends forward, and a place for companies to announce and showcase their latest releases to the strong media and influencer presence at T3. All of which are interactions that are uniquely suited to an in-person event where impromptu meetings and hallway conversations occur.

In other words, just as with traditional adviser conferences themselves, the future of AdviserTech events will be a blend of in-person for more community-based events (including the T3 Advisor Technology trade show), and virtual events like AdviceTech.LIVE for more targeted education, software showcases, and building brand awareness for AdviserTech vendors.

One of the biggest blocking points for new adviser technology innovation is the difficulty in distributing new technology solutions into the fragmented adviser landscape. As at one end of the spectrum are the large adviser enterprises — primarily banks and broker-dealers, and a growing number of mega-RIAs — which solve for the fragmentation by aggregating together a large number of advisers, but come with the complex demands of enterprises (from expectations of SOC-2 audits to multiple permission layers for specialized enterprise roles to custom integration requirements) and incredibly long enterprise sales cycles. At the other end of the spectrum are the solo independent advisers — primarily independent RIAs — who are their own firms and make their own technology decisions — one single adviser licensing seat at a time.

In practice, most AdviserTech firms break into the market with independent advisers first, valuing the much-faster sales cycle of the adviser-as-user-and-decider to gain initial traction, validate their product and begin expanding their feature set for the subsequent pivot into enterprises. With the caveat that reaching a critical mass of independent RIAs is still often a real challenge, given that the typical AdviserTech startup doesn’t have a deep boots-on-the-ground sales team. Which makes conferences where independent advisers gather a particularly compelling entry point to gain initial visibility and early adopter purchases, from the T3 Advisor Technology conference, to popular RIA trade shows like the former TDA LINC and Schwab Impact.

In this context, XY Planning Network launched its own Advisor FinTech competition back in 2016 to attract the next generation of adviser technology startups to its uniquely next-generation adviser base (as the organization’s focus on planning for Gen X and Gen Y clients has attracted a younger-than-average adviser, and its now 1,500-plus independent RIA advisers form one of the largest concentrations of independent advisers in one place). Over the past five years, the competition — which is limited to ‘startups’ (companies that launched in the past 12 months, or have less than $1 million of revenue) — has debuted some of the most popular up-and-coming AdviserTech tools, including SnappyKraken (2016 winner, subsequently raised $9.5 million), Vestwell (2017 winner, subsequently raised $112 million), Mineral’s Approach (2018 winner, subsequently acquired by Carson Wealth), and Holistiplan (2019 winner).

The latest 2021 XYPN AdvisorTech competition — after a hiatus in 2020 due to the pandemic — will showcase 12 AdviserTech companies, which will each receive an opportunity to deliver a seven-minute demo to the XYPN LIVE adviser audience, and this year will feature an “audience-favorite-based” voting mechanism for a Best In Show winner. Entrants are expected to follow the theme of “Productivity and Personalization” — highlighting AdviserTech tools that are specifically built to enhance the productivity and efficiency of the advice delivery process or better personalization for clients, with a particular focus on “AdviceTech” tools specifically facilitating the delivery of financial planning advice (and not just portfolio management services).

Ultimately, XYPN’s AdvisorTech Expo is narrower and more focused than the broader T3 Advisor Technology conference — which is still the largest AdviserTech trade show — or Informa Connect/WealthStack (which is more focused on WealthTech and technology tools for investment management), and will include a more curated list than events like AdviceTech.LIVE (as entrants must submit to consideration, and XYPN’s Expo will only include 12 finalists that get to present in-person at the conference in November). Which means it won’t necessarily function as a competitor to other AdviserTech events. But for vendors looking to get in front of a sizable audience of independent RIAs, without the high cost of traditional conference exhibitors (as selected finalists will be able to showcase at the Expo without being required to pay an exhibitor fee to the sponsor), XYPN’s AdvisorTech Expo is an appealing option for AdviserTech startups still trying to gain initial traction and get noticed.

Applications to the XYPN AdviserTech Expo are due by Oct. 1, and can be submitted here.

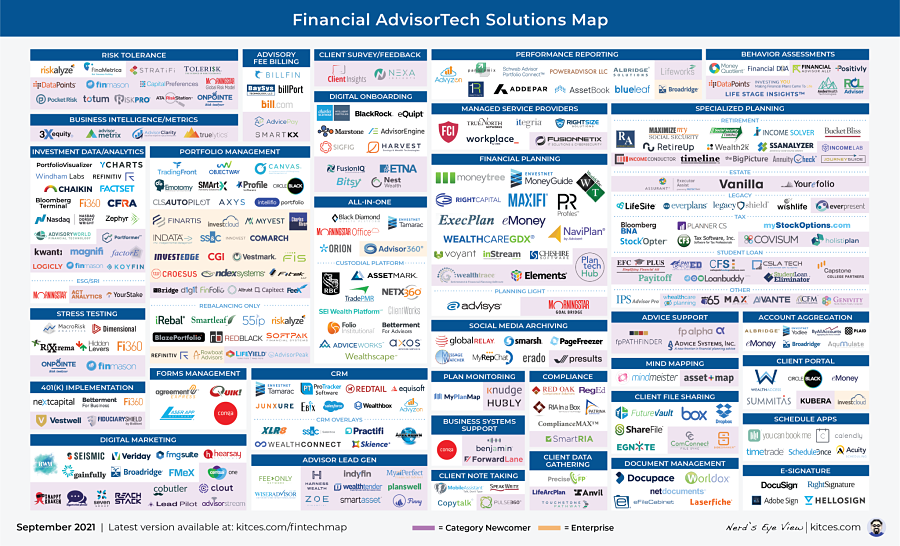

In the meantime, we’ve updated the latest version of our Financial AdvisorTech Solutions Map with several new companies, including highlights of the Category Newcomers in each area to highlight new FinTech innovation!

So what do you think? Is there still room for Riskalyze to gain more advisor adoption (in the U.S.), or should it expand into the world of direct indexing? Will more players like Veriti come to participate in the advisor direct indexing trend? Can Altruist gain more traction as a vertically integrated TAMP than being just another RIA custodian? Will RightCapital be able to continue gaining market share from financial planning software competitors with a more dynamic approach to planning? Please share your thoughts in the comments below!

Disclosure: Michael Kitces is the co-founder of XYPN and is on the Advisory Board for Timeline App, both of which were mentioned in this article.

Michael Kitces is the head of planning strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’sEye View. You can follow him on Twitter at @MichaelKitces.

You can connect with Kyle Van Pelt via LinkedIn or follow him on Twitter at @KyleVanPelt.

A California team with four decades of combined experience and a Kentucky father-son practice headline this week's advisor movement.

From generative AI on trading desks to personalized portfolio tools, financial firms are spending big on AI, but measuring returns is proving harder.

The fast-growing RIA aggregator adds Transcend Capital Advisors, a multi-state firm with more than 1,000 client relationships.

Christopher Blotto moved this month to Janney Montgomery Scott.

Finturk also added new form-filling and cash sweep tools to its AI-first CRM platform, while Zeplyn builds advisor coaching into its own AI operating system

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income