Mike Quinn does his own taxes.

He pores over IRS Publication 17, a guide for individual filers, with the zeal of a certified public accountant, and he meticulously calculates how much money to set aside each April.

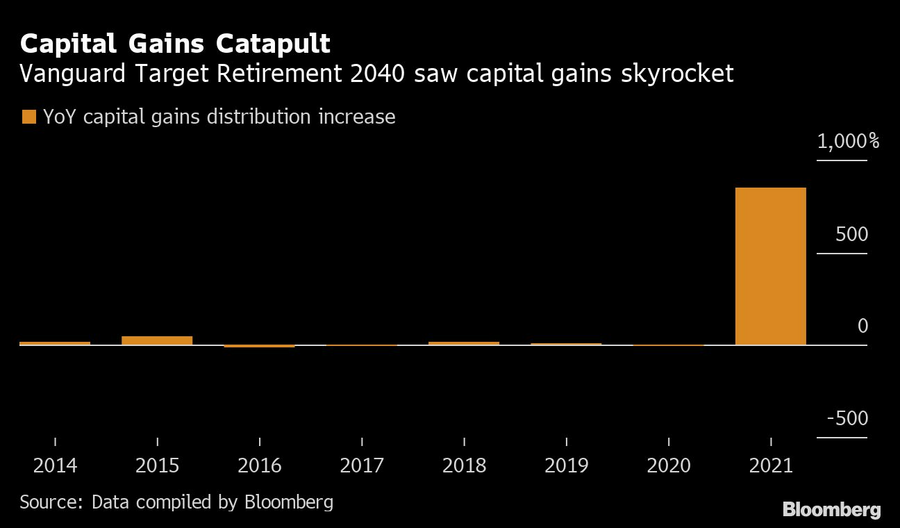

But this year came with a stinging surprise — a tax bill that was roughly $30,000 more than he anticipated. That’s because Quinn, an independent contractor from New Jersey, owned two Vanguard Group retirement funds that racked up massive capital gains — an increase of more than 2,000% from the prior year — that fell almost entirely on the shoulders of unsuspecting individual investors.

Quinn, 56, is just one of potentially tens of thousands of Vanguard clients stuck with significantly higher tax bills this year because of a change the company made to its target-date funds in late 2020, according to a class-action lawsuit filed March 14 in federal court in Philadelphia.

“I put faith in these guys for 20 years and lived through a couple of their foibles after Jack Bogle,” Quinn said, referring to Vanguard’s legendary founder, who died in 2019 and left a legacy built on lowering costs for retail investors. “This one was just too much.”

The Valley Forge, Pennsylvania-based company has a cult-like following among do-it-yourself savers, some of whom have voiced disappointment with customer service in recent years.

The tax debacle threatens to further erode that well of goodwill.

In December 2020, Vanguard made changes to its target-date funds, which allow investors to choose a year when they plan to retire and then let the company handle the rest — changing a fund’s asset mix to gradually become more conservative as the target date approaches. Indeed, Bogle embraced an investing philosophy of “set it and forget it” — tailored to investors with neither the time nor inclination to actively manage their own portfolios.

Vanguard had two classes of funds — lower-fee institutional funds and more costly retail funds. Seeking to stay competitive against other large asset managers, the firm lowered the institutional funds' minimum investment for retirement plans to $5 million from $100 million.

That triggered an “elephant stampede” — as Wall Street Journal columnist Jason Zweig described it — with money pouring out of the retail funds and into the lower-fee institutional funds, forcing Vanguard to sell assets from the retail funds. Assets at Vanguard’s 2035 target fund dropped $8 billion to $38 billion, and they fell by $7 billion to $29 billion in the 2040 fund.

While institutions and other investors with tax-advantaged accounts such as 401(k)s and IRAs weren’t adversely affected, the resulting capital gains fell on the pool of retail investors with taxable accounts who remained in the higher-fee funds.

This, according to the plaintiffs, was reckless and unnecessary. Vanguard, they claim, could have simply merged the retail and institutional funds from the beginning because they had the same strategy, asset mix and management. In fact, the firm decided to do just that in September, but after the damage had already been done, attorneys for the plaintiffs said in the complaint.

“Vanguard had other, readily-available ways to lower costs for retirement plans without hurting its taxable investors,” they wrote. “But it either did not even consider these options, or did not care about hurting its smaller, taxable investors. This was a gross violation of Vanguard’s fiduciary duties.”

The company and Chief Executive Tim Buckley are named as a defendants, along with more than a dozen other executives and trustees.

“Vanguard has a long-standing history of reducing costs across all products, strategies, and asset classes to directly benefit investors,” spokeswoman Emily Farrell said in a statement. “By dropping investment minimums for our target-date funds, we broadened access to lower-cost options for employees in small employer 401(k) plans. And by lowering costs for these funds, we helped millions of investors in individual accounts and retirement plans retain more of their returns.”

Lisa Greene-Lewis, a CPA with Intuit Inc.’s TurboTax, said that a surprise tax situation like the one outlined in the lawsuit could force unprepared investors to sell assets to come up with enough cash.

“They have to figure out quickly how to pay that tax bill,” she said. “They could use savings, or if they have some other assets, they might sell those to pay what they owe, but that’s like a snowball.”

Other plaintiffs include Valerie Verduce of Georgia, who held Vanguard’s 2020, 2030, and 2040 retail funds in taxable accounts. Those products distributed more than $60,000 in capital gains last year, leaving her with an estimated $9,000 tax liability. Another, Anthony Pollock of California, invested in Vanguard’s 2025 and 2035 retail funds and saw the holdings distribute more than $105,000 in capital gains, leaving an estimated $36,000 in tax liabilities. Catherine Day of Massachusetts invested in the 2025 and 2030 retail funds, which distributed more than $80,000 of capital gains, resulting in a estimated $12,000 tax liability, according to the lawsuit.

Quinn, who held Target Retirement 2030 and 2035, said he was outraged by the capital gains on the two funds. The year-over-year gains on the two funds far exceeded the average gains of just 1.9% on all other Vanguard funds he held.

“Vanguard has been great with fees — they’ve always been low,” Quinn said. “But this tax hit, and the reason for it, was infuriating.”

Cerulli research shows advisor retirements and breakaway movement fueling record M&A demand across the wealth management industry.

“The father even shared office space with the son and used a Medallion Guarantee stamp on the client’s account statements,” an attorney said.

The investment banking arm of RBC is ramping up its hiring across the U.S., Canada, and Europe.

The 140-year-old firm catering to ultra-high-net-worth clients joins a growing roster of wealth managers and tech providers plugging Claude into advisor workflows.

Three broker-dealers secure teams across the country as the recruiting race shows no signs of slowing.

As $84 trillion prepares to change hands, advisors who treat estate planning as peripheral are quietly building a sieve, not a book.

In volatile markets, the advisors who win aren't the ones with the best calls - they're the ones whose clients stay the course.