While inflation risks are rising more than at any point in the last two decades and investors could see further price changes over the summer, PGIM is more sanguine about long-run inflation. In an interview with IN Create, Nathan Sheets, former Undersecretary of the U.S. Treasury and PGIM Fixed Income’s Chief Economist and Head of Global Macroeconomic Research, shared the firm’s view on inflation, and how the team is investing in light of it.

IN Create: What are your expectations for inflation in the U.S. economy?

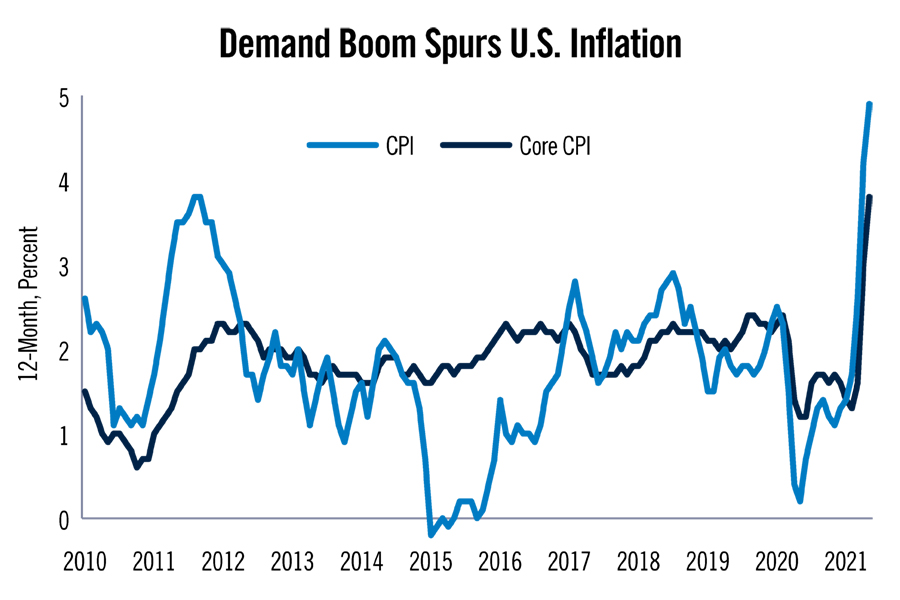

Nathan Sheets: We’ve seen some substantial price readings in recent months and could see more, but we believe it will prove temporary. A few factors are supporting near-term inflation. First, demand is strong and running ahead of aggregate supply as we come out of the pandemic. Second, supply chain shortages and bottlenecks are exacerbating price pressures. Finally, the service sector - which was hit hardest during the pandemic - is starting to recover. As prices in that sector normalize from extreme lows in 2020, that also creates higher inflation readings.

While these current pricing pressures are extraordinary, we believe they are transitory. Many of the bottlenecks and shortages should subside, easing some of the inflationary pressures on the supply side. You see it come up a lot in areas such as the commodities sector … these periods of intense shortages tend to generate demand and supply side responses, where even if pressures don’t abate entirely, the intensity diminishes.

On the demand side, government stimulus has pulled forward a lot of demand. But this is temporary. As stimulus ebbs and after society has fully opened for a while, we’ll return to a normal economic environment, in which higher prices tend to cut off demand.

IN Create: Economists and investors haven’t had to think about inflation in decades. While your base case is that inflation pressures normalize, is the threat more real this time around?

Nathan Sheets: Yes. I would say the risks around inflation are more severe than at any point in the last 20 years. The price pressures we are experiencing are intense. And there’s a chance the Fed gets it wrong. They plan to have a more reactive strategy, waiting to see sustained inflation before raising rates. Such policies aren’t designed to respond to high inflation. However, we still don’t believe these near-term pressures are feeding into an inflationary psychology that would spur longer term inflation.

IN Create: What signals are you watching to see if significant inflation starts to push through?

Nathan Sheets: There’s not a single indicator to watch … you need a dashboard. I’ll be watching goods prices in aggregate and service prices in aggregate to see how they are moving in relation to each other. Wages are a critical part of that dashboard. So are inflation expectations. I’ll also be looking for breadth: Are price increases concentrated in a few sectors – as they are today – or are those increases broadening?

IN Create: At what point do you think the Fed would respond by raising rates?

Nathan Sheets: I believe they’ll look through near-term readings and stay patient. The Fed wants strong evidence price increases aren’t transitory. They may taper bond purchases as early as October, but I don’t believe a rate increase is on the table until at least the second half of next year.

IN Create: How would you characterize the current rate environment? How were you positioned at the beginning of the year and have you since changed your view?

Nathan Sheets: Our view for some time has been that the economy will recover, but the Fed will hold off on raising rates any time soon. Further out, we believe the post-pandemic environment will resemble the pre-pandemic environment, with many of the same structural factors – aging demographics, high debt levels, deleveraging within the corporate sector, innovation and price competition – supporting a low-rate, low inflation environment.

We expect credit spreads to grind tighter and the dollar to depreciate a bit in the second half of this year as Europe’s economy improves. In terms of how we are positioned, we’ve generally been long credit and duration. We see opportunities in fixed income globally, with emerging markets providing a potentially durable source of alpha.

IN Create: Where does PGIM Fixed Income have a different view than the consensus?

Nathan Sheets: We are committed to the view that rates over the medium to long run will resemble the pre-pandemic environment, with the forces we mentioned earlier suppressing long-term inflation and rising rates.

IN Create: Where are you finding attractive opportunities in fixed income markets?

Nathan Sheets: Coming out of the pandemic, corporate leverage is obviously higher than going in. We expect many corporations to go through deleveraging processes, opening them up for potential upgrades as they improve their balance sheets. We also believe select, highly rated, senior CLOs (collateralized loan obligations) are attractive. It’s a market niche where some investors, given memories of the financial crisis, won’t invest in anything that starts with “C.” The reality is highly rated CLOs performed well during the crisis and we believe they remain a mispriced opportunity. Third, we remain bullish on emerging markets. They are a potential source of alpha, in an environment where finding alpha will remain a challenge.

To learn more about inflation in today’s economy, visit Insights at www.pgiminvestments.com

This material is being provided for informational or educational purposes only and does not take into account the investment objectives or financial situation of any client or prospective clients. The information is not intended as investment advice and is not a recommendation. Clients seeking information regarding their particular investment needs should contact their financial professional.

Investing involves risk, including possible loss of principal. Some investments have more risk than others. Fixed income investments are subject to interest rate risk, and their value will decline as interest rates rise. Past performance does not guarantee future results.

PGIM Fixed Income is a unit of PGIM, Inc. (PGIM), a registered investment advisor. PIMS and PGIM are Prudential Financial companies. © 2021 Prudential Financial, Inc. and its related entities. PGIM and the PGIM logo are service marks of Prudential Financial, Inc. and its related entities, registered in many jurisdictions worldwide.

1049818-00001-00

With trillions of dollars set to change hands, new data suggests probate costs and delays are becoming a bigger factor in estate planning decisions.

Orion and RFG Advisory tackle account-opening delays with new updates as custodial integrations reshape how fast advisors can move client assets.

The deal extends the acquisitive mega-RIA's rapid 2026 expansion as industry consolidation hits record levels nationwide

As recent Middle East tensions put the Strait of Hormuz back in focus, a structured process with purpose can help protect investors against their natural self-sabotaging tendencies in choppy markets.

ESG-focused Longwave Financial, approaching $1B AUM, acquired Seattle-based MG Financial and hired a client services manager from an LPL-affiliated firm.

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income