Bonds are considered a more conservative investment option compared to stocks. This asset class presents less risk, but the potential returns are also lower. Still, bonds remain an important part of a diversified portfolio.

In this article, we’ll discuss the benefits of investing in bonds. We’ll give you an overview of the best bonds to buy and the risks that come with them. An industry expert also shared effective investment strategies for those looking at bonds to strengthen their portfolio.

As seasoned investors, you’re all aware of the key benefits of investing in bonds:

Steady income stream: Bondholders receive regular coupon payments, which provide consistent cash flow

Capital preservation: When held to maturity, bonds can help protect your initial investment

Portfolio diversification: As bond performance is often not correlated with stocks and other asset classes, bonds can allow you to build a diverse portfolio

Tax benefits: Some types of bonds are exempt from federal and/or state income taxes; municipal bonds are an example

Stable investment: Bond prices don’t fluctuate as dramatically as stock prices, providing more stability to your portfolio

There are mounting concerns, however, about soaring government debt, which is expected to have long-term implications on the bond market. But according to experts, this doesn’t mean that investors should be wary of Treasury and other high-quality bonds.

“Bonds, particularly short-maturity ones, reduce portfolio volatility while offering attractive yields,” explains David Mammina, partner and financial advisor at Coastline Wealth Management. “With debt markets offering historically high yields, especially at the front end, bonds provide income with lower risk than equities.

“Tax-exempt municipal bonds also offer tax-advantaged income, enhancing returns for high-net-worth investors.”

Mammina is among our excellence awardees for the Best Independent Advisors in the US. Get to know him and other industry leaders by checking out our Best in Wealth Special Reports.

Mammina lists several types of bonds that have high return potential even in the current economy:

Let’s go over each of these bond categories.

Short-term bonds typically mature between several weeks and a few years. This means that you can receive the bond’s principal and any accrued interest sooner. A good example is Treasury bills, also called T-bills, issued by the US government. They can have a maturity period as short as a few months.

Short maturity bonds are considered less risky investments compared to long-term bonds. This is because they are less sensitive to interest rate changes that can lead to significant price fluctuations. They are also more liquid, allowing you to access the funds more easily.

“Short maturity bonds, like T-bills, are optimal due to high yields and low equity correlation,” notes Mammina, who holds CFP, MBA, and CRPC designations.

Tax-free bonds offer opportunities to earn interest income that is exempt from federal income tax and, in some cases, state and local taxes. This type of bond is often issued by state and local governments to fund public projects, including hospitals, schools, and roads.

A popular example is the resurgent municipal bonds, also called munis. “Tax-exempt municipal bonds provide stable, tax-advantaged returns, with $280 billion in new issuance year-to-date and positive fund flows,” Mammina says.

Their tax-exempt status also makes them an attractive choice if you’re in a higher tax bracket and looking to maximize your after-tax returns. The exemption, however, doesn't apply to capital gains if you sell the bond for a profit before it matures.

You can buy municipal bonds through brokerage accounts, either directly or through mutual funds or exchange-traded funds (ETFs).

As the name suggests, TIPS are debt securities set up to hedge against inflation. They also have US government backing, making them among the lowest-risk bonds you can invest in.

Additionally, TIPS’ principal isn’t fixed, unlike other types of Treasuries. The amount can rise or fall during its term. If the principal is higher than your initial investment, you’re paid the increased amount. But if it’s equal to or lower than your initial investment, you get the original amount.

“Treasury inflation-protected securities are attractive for inflation hedging, with real yields reflecting market expectations of 2.25 percent inflation over five years,” Mammina explains.

Investment-grade corporate bonds are issued by corporations that are less likely to default, making them a good option for conservative investors. These bonds receive high ratings from major credit rating agencies such as Fitch, Moody’s, and Standard & Poor's (S&P).

“Investment-grade corporate bonds offer higher yields with manageable risk for diversified portfolios,” Mammina says.

On the Fitch and S&P scales, bonds rated BBB- or higher are considered investment-grade. For Moody's, investment-grade bonds have a rating of Baa3 or higher. These ratings show the issuer's ability to repay debt. The higher the ratings, the lower the default risk.

When investing in bonds, there are several strategies you can take to maximize returns. Your choice can depend on a range of personal factors – investment goals, risk tolerance, time horizon – and economic factors – interest rates and market conditions.

These are just some of the tried-and-tested strategies bond investors use:

This is considered one of the most popular and effective strategies for investing in bonds. It involves buying bonds and holding them until maturity, regardless of short-term market fluctuations.

This strategy suits you if you’re focused on the long-term benefits such as steady income streams and capital preservation. You can also reinvest coupon payments in other bonds or assets to further optimize returns.

This involves investing in short-term and long-term bonds, while avoiding intermediate-term debt securities. The goal is to balance the stability and lower yields of short-maturity bonds with the potential higher returns but greater risk of long-term bonds.

Think of short-term bonds as a buffer that provides security and a steady income stream. The long-term bonds, meanwhile, offer potential higher returns, especially if interest rates drop.

The barbell strategy gets its name from its graphical representation, which resembles a barbell used in weightlifting. With investments allocated to two distinct extremes – low-risk and high-risk assets – this creates a bond portfolio heavily weighted at both ends.

Here’s an illustration:

The example shows a bond portfolio consisting of:

As you can see, there are no bonds within the four- to six-year range.

The barbell strategy, however, requires active management. This is because short-term bonds need to be reinvested at maturity to reduce the impact of potential interest rate increases. You may also need to rebalance your portfolio based on changing market conditions.

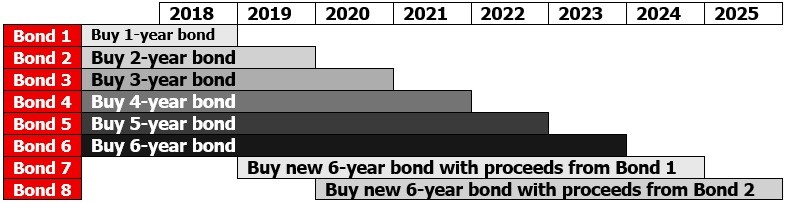

Laddering requires building a portfolio of bonds with different maturity periods. This creates a “ladder” of investments that mature at different times. This strategy helps reduce the risk associated with fluctuating interest rates.

By spreading maturity dates, you can create a more stable and predictable income stream as bonds mature at different intervals.

Here’s an illustration:

Bond ladders also provide greater flexibility in managing liquidity. As bonds mature, you can reinvest the payments for other investments or spend them on personal needs.

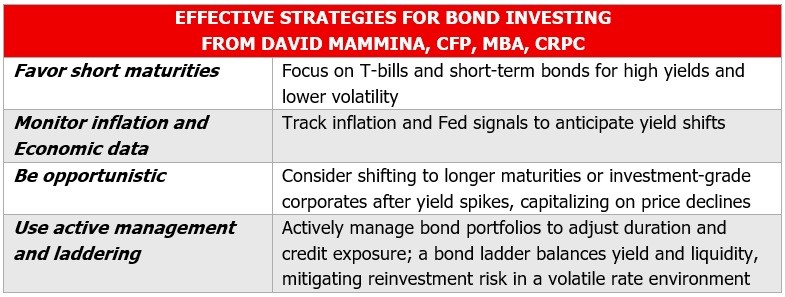

Here are some practical tips and strategies from Mammina for those who want to maximize returns from their bond investments:

Find out if active investing makes more sense in fixed income than equities in this article.

There are several risks you should be wary of when investing in bonds. Mammina sums up the four biggest risks as:

Let’s expound on these a little more.

Because of their longer maturities, long-term bonds are more sensitive to interest rate changes than short-maturity bonds. You can manage interest rate risk by diversifying your bond holdings. Bond laddering is one of the most effective ways to lessen the impact of rising interest rates on your portfolio.

Inflation erodes the purchasing power of coupon payments received from bonds, particularly those with fixed interest rates. When prices rise, the real value of these fixed payments decreases.

Bonds often act as a diversifier in a portfolio. This means that they are expected to move inversely to stocks to reduce overall portfolio risk. Diversification is more effective if bonds and stocks have a low or negative correlation.

If the correlation, however, shifts to positive, the benefits of diversification are reduced. If this happens, both asset classes may fall in value during a market downturn, resulting in larger losses.

Bonds are less liquid than stocks and cash. If you need to sell a bond quickly, you may need to accept a lower price to find a buyer, potentially resulting in capital loss.

There are several factors that investors need to consider when buying bonds. Mammina crunches the numbers to emphasize the importance of some key variables before you start investing in bonds.

“Inflation affects bond yields,” he says. “In May 2025, inflation was 2.3 percent (core at 2.7 percent), a bit higher than expected. With solid economic growth, like 2.8 percent GDP in 2024, the Fed might delay cutting interest rates, which could affect bond prices.”

“The 10-year Treasury yield was 4.23 percent on July 1, 2025, down slightly from 4.435 percent in April. Shorter maturities (e.g., two-year yields at 3.75 percent) offer lower volatility and better risk-adjusted returns.”

“Rising deficits, projected to increase by $3 trillion to $4 trillion over a decade due to recent fiscal bills, pressure yields,” Mammina notes. “Concerns about US debt sustainability, highlighted by Moody’s downgrade, remain critical.”

“Assess issuer credit quality to avoid default risk, especially in volatile markets.”

While bonds may not offer the same high growth potential as stocks, they play an essential part in portfolio diversification. They serve as a cushion against market volatility, providing investors with a more predictable income stream compared to stocks. This stability makes investing in bonds beneficial during economic downturns.

Subscribe to InvestmentNews+ today for full access to premium content, data, and investment analysis

IRAs now hold nearly twice the assets of 401(k) plans — and most of that money didn't arrive through annual contributions.

A new survey finds that many women prioritize financial security but continue to leave savings in accounts that may not keep pace with inflation.

Roundhill, Bitwise and GraniteShares funds remain on hold while the agency weighs how novel ETFs should be regulated.

"Shares of alternative assets managers have lagged this year as investors grow wary of private-credit exposure."

The fintech platform is touting a new AI-free Planning Observations feature, which draws on IRS tax records to uncover opportunities for advisors.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.