Unlike with public companies, federal securities laws restrict investments in private firms to accredited investors – and for good reason. Investing in the private market carries a much bigger risk as firms aren’t subject to normal disclosure requirements; something that publicly traded companies must meet.

Accredited investors are well-equipped to make smart investment decisions even with limited information to work with. But what are accredited investors exactly? And why do securities regulations allow them to take on inherently riskier investments? This article answers these questions and more, so keep reading.

The Securities and Exchange Commission (SEC) allows only accredited investors to participate in unregulated securities offerings. In layman’s terms, this means that if you’re considered as one, you can access investment products that aren’t available to the public.

As an accredited investor, you’re expected to have either:

If you meet any of these criteria, the SEC considers you as someone “financially sophisticated” enough to fend for yourself. Therefore, you’re also in less need of the protections that come with a registered offering.

An accredited investor status, however, doesn’t only apply to high-net-worth individuals and experienced investment professionals, or what the SEC refers to as natural persons. Financial entities that meet certain criteria can also be considered as accredited investors. More on this later.

Accredited investors play an important role in the investment process. Check out this guide if you want to learn the basics of how to start investing.

The SEC lays down the criteria on who qualifies as accredited investors in Rule 501 of Regulation D under the Securities Act. Under these rules, the commission has set different requirements for individuals and businesses.

Individuals must satisfy income and professional criteria to be considered as an accredited investor. To qualify as one, you must meet any of the following:

annual income must be over $200,000 for individuals or $300,000 for couples in each of the previous two years, with a reasonable expectation that income will be the same or higher in the current year

net worth must be over $1 million for both individuals and couples, excluding the value of their primary residence

financial or investment professional in good standing and holds any of the following licenses from the Financial Industry Regulatory Authority (FINRA):

director, executive officer, or general partner (GP) of a company selling securities

any “family client” of a “family office” that qualifies as an accredited investor

“knowledgeable employees” of a private fund

Financial entities can be considered as accredited investors based on one of these factors:

Want to know what the SEC’s role is in protecting investors? Check out this guide to find out everything you need to know about the Securities and Exchange Commission.

Once you or your business meets any of the criteria above, you can start investing in the private market. You also automatically join the pool of potential investors for companies looking to raise capital.

The SEC doesn’t grant accredited investor status. Rather, it’s the private companies’ responsibility to ensure that those they approach for funding meet the criteria of an accredited investor.

If you want to invest in unregistered securities, you can also approach private companies seeking investments. Depending on your credentials, the company may ask you to provide financial documents as proof of your status. More on this later.

Not all individuals, however, need to prove their credentials to invest in unregulated securities. These include industry professionals with certain accreditations, hedge fund managers, and partners in private equity firms.

The five-star awardees of our Top Financial Advisors in the USA list are prime examples of industry professionals whose credentials alone qualify them as accredited investors.

Private companies use different methods to verify your status as an accredited investor. These are the most common ones:

To ensure that you meet the SEC’s income threshold for individual accredited investors, you may be asked to provide official tax records from the past two years. If applicable, these may include:

Some private firms may accept pay stubs or ask for an employment verification letter.

Calculating your net worth involves getting the total value of your assets then subtracting the total value of your liabilities. The resulting figure is your total net worth. As mentioned, the value of your primary residence is excluded from the calculation.

Private companies may ask you to provide the following as proof of assets:

For your liabilities, companies may run a soft credit pull or request a consumer credit report from a major credit bureau. Some private firms may also require that all documentation to be under the accredited investor’s name and dated within the last 90 days.

As mentioned, financial professionals in good standing and with the following FINRA licenses qualify as accredited investors:

Private firms can independently verify your licensure status through FINRA’s Brokercheck tool.

Third-party attestations can be used to certify your status as an accredited investor. The document must be dated within the past 90 days and written by one of the following:

Accreditation letters follow a template and must contain specific wording required by the SEC. This includes confirmation that:

Here’s a sample template of a third-party attestation letter from Montague Law, a Florida-based venture capital law firm.

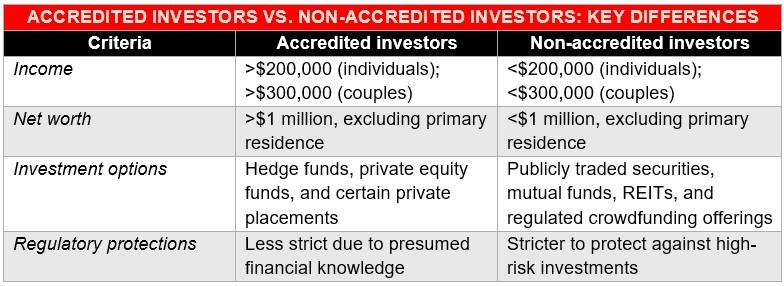

The SEC classifies investors into two categories based on income and net worth – accredited investors and non-accredited investors. This distinction has a direct impact on the type of investment opportunities available to each group.

Accredited investors are considered financially sophisticated enough to understand the risks associated with unregistered securities. They also have the financial means to weather any losses they may incur. These investors can likewise access investment products that aren’t available to their non-accredited counterparts such as hedge funds and private equity offerings.

In one of the previous sections, we defined what accredited investors are and outlined the eligibility requirements. For non-accredited investors, the SEC sets these criteria:

Not surprisingly, non-accredited investors comprise a huge portion of the investing public. In its latest report, the SEC reveals that only about one in five (18.5 percent) US households qualify as accredited investors.

Also referred to as retail investors, non-accredited investors are subject to stricter securities regulations. These laws are designed to protect them from making high-risk investments that they may not fully understand or afford.

This table sums up the key differences between accredited investors and non-accredited investors.

Once you achieve an accredited investor status, you can access several benefits that aren’t always available to the investing public. Here are some of them:

The biggest benefit that comes with being an accredited investor is that you can access securities products that aren’t available to your non-accredited counterparts. These include:

While riskier, these investment opportunities often yield higher returns.

Because of your presumed industry knowledge and financial resources, you don’t require the same level of protection as retail investors. For companies raising capital, this means less red tape and paperwork, lower compliance costs, and more flexibility.

Your status as an accredited investor allows you to access deals that are off-limits to the investing public. Many of these investment prospects are early-stage companies with strong growth potential. You can also access alternative investments that can deliver returns significantly higher than what the stock market could provide.

Being an accredited investor gives you the opportunity to rub elbows with the most influential players of the industry. You may be able to join exclusive events and conferences where you can network with other high-net-worth individuals.

Being an accredited investor, however, isn’t all roses. Some of the drawbacks of holding this status include:

Higher risk investments: While the potential returns are higher, there’s no guarantee that your investments will succeed, especially those involving early-stage companies.

Less regulatory oversight: As an accredited investor, you have less regulatory protection if your investments fail. The SEC presumes that you have sufficient industry knowledge and financial resources to fend for yourself.

Transparency challenges: Private companies are exempt from the SEC’s registration and disclosure requirements. This is where due diligence comes into play. Careful research and planning are necessary if you want to protect yourself from potential risks.

Many of the industry’s leaders qualify as accredited investors. If you’re looking for someone to model success from, our Best in Wealth Special Reports page is the place to go. Get to know how these investment experts rose through the ranks to become among the industry’s biggest and most influential players.

In an era of AI euphoria and market FOMO, getting back to basics with fixed income may be the most contrarian and most important move advisors can make.

Voya Financial adds private equity, credit and real estate options to its AMA program, building on support for looser federal investment rules in retirement accounts.

Shannon Reid, president of Osaic and the network’s number two executive, has plenty of challenges, industry executives said.

Auditors flagged the commingling. The COO allegedly knew. Investors kept getting the pitch

The advisors on the move include two brothers leading a family practice in Connecticut, and a husband-and-wife tandem working with business owners in the West Coast.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.