Updated December 14, 2023

The Tax Cuts and Jobs Act (TCJA) of 2017 provides a tax deduction to owners of a business that qualifies as a pass-through entity. The provision is scheduled to last until the end of 2025, but Congress has the authority to extend it to 2026, and even beyond.

The pass-through deduction, however, is not a straightforward provision. To be eligible, business owners must meet structure and income requirements. Still, the tax cuts don’t apply to all taxpayers equally.

In this article, Investment News explains how the pass-through deduction works and what businesses that exceed taxable income thresholds can do to qualify. Financial advisers can also share this piece with their business-owner clients to educate them on this important but complicated TCJA provision.

In 2017, the Tax Cuts and Jobs Act (TCJA) created a new form of tax deduction for owners of pass-through businesses. Also referred to as the 199A or qualified business income deduction, the pass-through deduction is capped at 20% of the business owner’s overall taxable income.

But to qualify, there are several requirements that businesses must meet:

Pass-through entities are structured in a way that helps businesses avoid the effects of double taxation. As the name suggests, the taxes of these types of businesses “pass through” the owners. Such entities don’t pay taxes at the corporate level, meaning they are prevented from being taxed twice.

Some of the most common structures of pass-through businesses are:

A sole proprietorship is a type of business that is owned and managed by one person. There’s no legal distinction between the business entity and the owner, who often pays personal income tax on business income.

A sole proprietor doesn’t necessarily work alone and may have other employees. This type of business structure is also called a sole tradership, or individual entrepreneurship or proprietorship.

A partnership is a type of business structure where two or more individuals share ownership. Each partner contributes to all aspects of the business. In return, they share in the profits and losses of the business.

Partnerships don’t pay federal income taxes directly. Instead, each partner reports their share of taxable income on their personal tax returns.

An LLC is a type of business structure that protects the owners from personal liability for the company’s debts and claims. If the entity is sued or unable to pay its debts, the owner’s personal possessions can’t be legally pursued.

An LLC can have one or more owners, also called members. LLC members share the responsibility of managing the business unless they bring in someone from outside to handle the daily operations.

An LLC is also not considered separate from its owners. Just like a sole proprietorship and a partnership, an LLC’s income passes through the business to its members, who then report their share of profits or losses on their individual income tax returns.

Just like an LLC, an LLP is granted limited liability protection, meaning the owners’ personal assets can’t be involved in business litigation or debt collection. The owners also don’t pay federal income taxes directly.

But unlike LLCs, which can have a single owner and be run by a non-member, LLPs have multiple owners who exclusively manage the business’ daily operations.

An S corporation is a special tax status granted by the Internal Revenue Service (IRS). It enables businesses to take advantage of the same legal protections as a C corporation but be taxed as a pass-through entity. This means that S corporations are exempt from federal taxes. Each shareholder reports profits and losses from the business on their personal income tax returns.

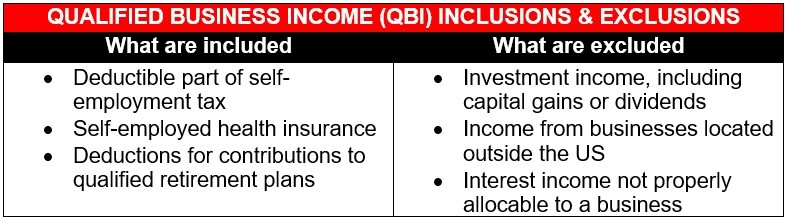

Enterprises also need to have qualified business income (QBI) to be eligible for a pass-through deduction. A QBI is defined as the net profit a business earns in a year. This can be calculated by subtracting a business’ deductions from its income.

Here’s what are usually considered part of QBI and what are not. You can find the complete list of inclusions and exclusions on the IRS’ QBI primer.

A business owner’s taxable income must not exceed a certain threshold to qualify for a pass-through deduction:

Some businesses earning above the threshold may be eligible for a portion or the full 20% pass-through deduction. The standard deduction for 2023 is:

Business owners aged 65 or older may be eligible for a higher standard deduction amount.

In addition, entities considered as service trades or businesses may be ineligible for the pass-through deduction. These include firms involved in:

Even if the business owners’ taxable income exceeds the thresholds above, there are still ways to reduce this taxable income to claim the pass-through deduction. Here are some of them, according to industry experts:

“The easiest, most obvious [strategy] is using a 401(k) plan,” notes Leon LaBrecque, chief growth officer of the wealth management specialist Sequoia Financial Group.

Professionals could reduce their taxable income – which includes employer plus employee contributions – with a 401(k) plan by a maximum of $66,000 in 2023 and $69,000 in 2024. The thresholds increase to $73,500 in 2023 and $76,500 in 2024 for those ages 50 and over.

So, an older, self-employed professional with a pass-through income of $370,000 can use a solo 401(k) plan to deduct $73,500 from income taxes and get the pass-through deduction.

“You’re getting a double bang for your buck,” LaBrecque adds.

Cash-balance plans can offer an even greater deduction, perhaps to the tune of a few hundred thousand dollars, according to industry experts.

“If the deduction you’re trying to get is under $55,000 or $60,000, a 401(k) plan will typically work,” explains Jason Kolinsky, a financial planner at Kolinsky Wealth Management. “If you want to do more than that, that’s when you’re typically looking at a cash-balance plan.”

Kolinsky adds that these plans are a type of pension plan but feel more like defined-contribution plans than traditional pensions.

The caveat, according to the financial adviser, is that owners should expect to establish cash-balance plans for several years. They must be willing to make plan contributions for employees during that period. “They’re also generally more costly to administer than 401(k) plans,” Kolinsky says.

But there’s another important distinction, according to Timothy Steffen, director of advanced planning in the private wealth management group at Robert W. Baird & Co. Cash-balance-plan contributions would reduce the net business income as the contribution is made at the business level, not the individual-owner level.

For example, if a partnership with two 50% owners and $500,000 in profit makes a $50,000 pension contribution, it lowers the partnership’s taxable income to $450,000, and each of the business owners’ taxable income by $25,000.

Again, the business owner’s taxable income is what determines if they get the 20% pass-through deduction.

Making large charitable gifts is also a way to reduce taxable income. Professionals can only offset a certain percentage of their income through charitable donations, Steffen adds.

They can offset up to 60% of their income each year by gifting cash to a public charity like a donor-advised fund.

A gift of stock, meanwhile, only offsets up to 30%. So, those with taxable income of $1 million, for example, wouldn’t be able to solely gift their way to the pass-through deduction.

The tax law changed the rules around bonus depreciation. According to Steffen, through 2022, business owners could write off 100% of the cost of a new piece of equipment in the year it was purchased. That percentage will then ratchet down in 20% increments, eventually hitting 0% in 2027.

The effect is a reduction in taxable income, via a reduction in business income. For example, a sole owner of a business with $500,000 in profit buys a $200,000 piece of equipment. The owner can take a $160,000 write-off in 2023 and ink a $340,000 total profit.

“Advisers sitting marginally over the income threshold can look at what they want to do in their office, like new furniture or computers,” LaBrecque says.

Many small businesses in the US opt for a qualifying pass-through business structure because of the several benefits. These include:

Unlike C corporations in which the entities and owners are required to pay business and individual income taxes, respectively, pass-through businesses don’t carry the burden of double taxation.

Instead, the profits and losses from the company are passed through the business itself onto its owners, who must then report the income when they file their personal tax returns. Pass-through deductions can be particularly beneficial to business owners who must pay the self-employment tax.

Owners of pass-through entities have the freedom to change their structure if they feel that the business has outgrown the existing structure. This allows owners to pick a structure that’s right for the business, while keeping the benefits of a pass-through deduction.

Sole proprietors, for example, can easily file paperwork to switch to an LLC if they feel that this type of structure suits them better. LLCs, meanwhile, can choose to be taxed like an S corporation or a C corporation.

Back when the TCJA was up for debate, a group of small business owners claimed that the reduction of the corporate tax rates from 35% to 21% heavily favored large companies. Because of this, lawmakers incorporated a tax break for small businesses in the legislation.

Called the qualified business income deduction, this provision enables pass-through entities to reduce up to 20% of their QBI to decrease their tax burden.

Business owners who want to claim the pass-through deduction must first complete Form 8995 or Form 8995-A. According to the IRS, Form 8995 applies to:

Business owners who don’t meet the above criteria should use Form 8995-A. After the pass-through deduction has been calculated, owners can claim it on Line 13 of their Form 1040.

Keep abreast of the latest developments in tax planning and administration in our Tax Management News Section. Be sure to bookmark this page for easy access to breaking news and the latest legislative updates.

A new proposal could end the ban on promoting client reviews in states like California and Connecticut, giving state-registered advisors a level playing field with their SEC-registered peers.

Morningstar research data show improved retirement trajectories for self-directors and allocators placed in managed accounts.

Some in the industry say that more UBS financial advisors this year will be heading for the exits.

The Wall Street giant has blasted data middlemen as digital freeloaders, but tech firms and consumer advocates are pushing back.

Research reveals a 4% year-on-year increase in expenses that one in five Americans, including one-quarter of Gen Xers, say they have not planned for.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.