Although downsizing may save money in the long term, it isn’t a cheap exercise. Reports have emerged that leading American financial institutions have shelled out upwards of a billion dollars on termination pay in the first two quarters of this year. This pain is a repercussion of Wall Street's overaggressive expansion strategy during the Covid-19 pandemic.

On Wednesday, Goldman Sachs, severely impacted by a slump in trading and investment banking, was the latest banking behemoth to announce a financial hit due to recent staff retrenchments. The bank disclosed it had incurred $260 million in severance-related expenses during the year's first half. Goldman has dismissed around 3,400 personnel, which is approximately 7% of its total workforce, this year.

A day earlier, Morgan Stanley, which has already terminated about 3,000 of its employees this year, revealed that it had paid over $300 million for staff layoffs, including nearly $80 million to wealth management employees. Meanwhile, Citigroup declared last week that it had spent an additional $450 million on severance pay. The bank announced in the previous month that it was nearing the completion of 5,000 job reductions.

Options Group's Michael Karp, a prominent Wall Street recruitment specialist, told The Financial Times that more workforce adjustment is likely in investment banking. He predicted, "For the remainder of the year, many of the larger firms will likely follow a dismiss-two-recruit-one approach."

Several Wall Street companies now admit they expanded their workforce excessively during the pandemic to keep up with a surge in trading and deal-making activities, even as remote working affected efficiency.

The drastic shift from boom to bust in recent years has been remarkably swift, even by investment banking's cyclical standards. More 11,000 layoffs have been collectively announced by Wall Street's largest employers this year.

There is a split among executives on whether more layoffs and resulting severance payments will be needed as the year advances.

Morgan Stanley's CFO, Sharon Yeshaya, told analysts this week that the bank anticipates benefiting from a backlog of deals and plans to "augment our reach to optimally exploit the opportunity."

Conversely, Goldman's CEO, David Solomon, said the bank would initiate another round of performance-based layoffs, a practice that was paused during the pandemic but reinstated last year. However, Solomon noted there were "no concrete plans for workforce reduction presently."

Citi has hinted at potential future layoffs. Citi CEO Jane Fraser told analysts last week, "As we advance through the latter half of the year, we will concentrate on further reducing our expenditure through a more streamlined organizational model."

Wells Fargo informed investors that it expects its workforce, which has already shrunk by 5,000 this year and 40,000 since mid-2020, to continue to decline. This bank was among the few that did not grow during the pandemic, partly due to an imposed regulatory asset limit following multiple legal and compliance violations.

Based in San Francisco, Wells Fargo, whose business leans more towards consumer banking than deals and trading, has hiked its expense forecast for this year by $800mn. Most of this hike is attributed to layoffs, though the bank did not reveal the exact costs already incurred.

On Tuesday, Bank of America stated that it had eliminated 4,000 roles, about 2% of its total workforce, in the second quarter. BofA has primarily relied on natural attrition, thereby avoiding massive severance payments.

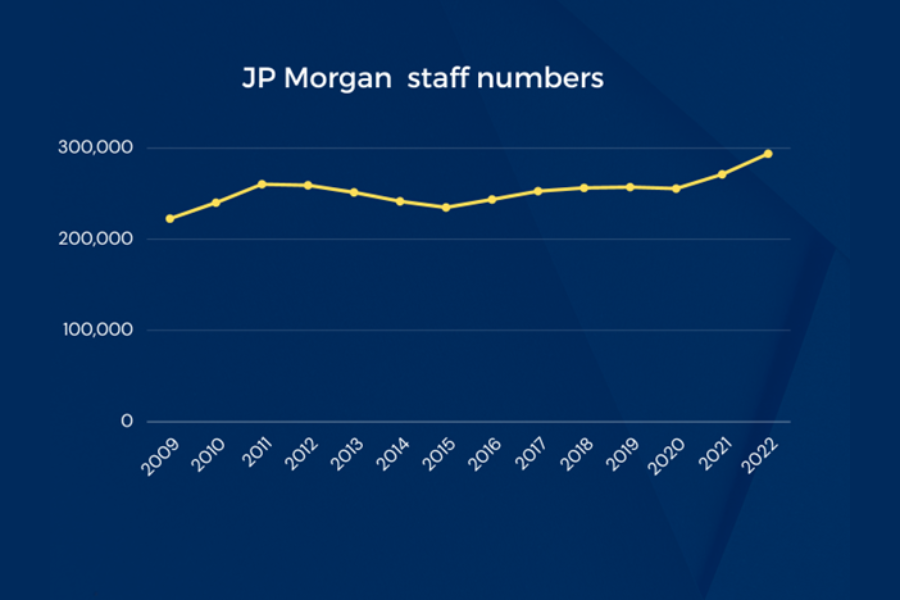

Standing out from the crowd, JPMorgan Chase, the country's largest bank in terms of assets with extensive retail, investment banking, and trading operations, increased its workforce by 8% to 300,000 in the second quarter. This doesn't include the employees from First Republic, the California-based lender it acquired in May, whose employees officially joined JPMorgan in July.

First-half job cuts;

Bank of America 4,000

Citigroup 5,000

Goldman Sachs 3,400

Morgan Stanley 3,000

Wells Fargo 5,000

James Walesa “should have been barred from the industry years ago,” one attorney said.

Kristy Smith from Broadridge says advisors who can't adapt risk being left behind.

Three contenders stand out to replace the departed Erika McEntarfer, according to Hal Ratner, who is the head of research for Morningstar Investment Management.

Surveys show continued misconceptions and pessimism about the program, as well as bipartisan support for reforms to sustain it into the future.

With doors being opened through new legislation and executive orders, guiding clients with their best interests in mind has never been more critical.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.