Rate cuts are on the agenda and bond yields are near post-pandemic highs. Now could be the time to take advantage of a potential golden age for fixed income.

Rates are at their peak, and rate cuts are set to follow

History may not repeat itself, but it usually rhymes. Nothing in the investment world demonstrates this better than economic and interest rate cycles.

Every few years, central banks typically raise rates to contain an overheating economy and then cut them to arrest slowing or receding growth. The impact on fixed income tends to be predictable: painful when rates rise, but beneficial when they fall.

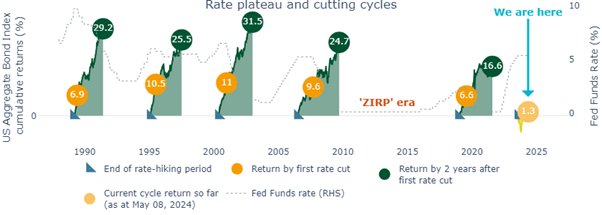

It should therefore be no surprise that the last five rate cutting periods were golden ages for bond markets. The Bloomberg US Aggregate Bond Index (known as “the Agg”) returned between 16.6% and 31.5% two years following each of the cycle’s final rate hike (Figure 1).

Figure 1: Investors may still be able to make the most of a potential fixed income golden age[1]

The sweetspot for a fixed income allocation has generally been before the first rate cut – which we expect to see in the second half of 2024.

Importantly, the Agg has only returned 1.3% since the Fed’s last rate hike in July (over nine months ago), and US credit markets only 3.3%. In other words, we think investors still have time to “get in on the ground floor” of the potential upcoming golden age by allocating to fixed income now.

Bond yields are still close to post-pandemic highs, and often imply “equity like” returns

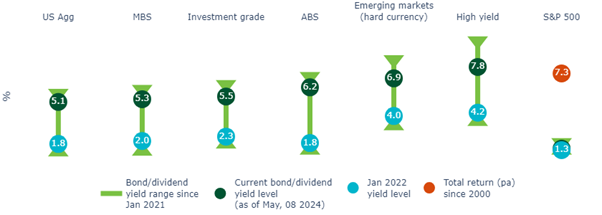

Even with rate cuts on the agenda, bond yields are still close to their recent highs. In some sectors, yields even imply buy-and-hold returns close to long-term equity total returns (Figure 2).

Figure 2: Yields remain elevated among multiple fixed income sector1

This situation may not persist, particularly once markets see rate cuts as imminent, so investors may benefit the most from acting quickly.

In our view, this environment lends itself to a multi-sector approach. Managers with specialist capabilities and credit analyst resources will likely be able to target a diverse portfolio that maximizes risk adjusted yields across these sectors and capitalize on relative value opportunities across each market.

A global approach may be the most comprehensive way to participate in the golden age

Casting the net wider to global fixed income markets may also be worth considering, particularly for those concerned about US rates remaining “higher for longer”.

The US economy appears to be materially outperforming its global peers, with the IMF even projecting the US will grow at double the pace of any of its G7 peers this year.

This might be good news for US risk assets relative to the rest of the world, but maybe not for US bonds, as it reflects more stubborn inflation in the US. As recently as last fall, CPI was running lower in the US than in Canada, the eurozone, the UK, Australia and New Zealand. But now, it’s running faster than all of them.

At the start of the year, many expected the US to be the first to cut rates among its peers, now it looks like it could be the last.

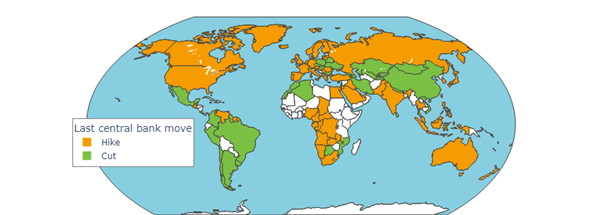

Those with a global approach may benefit from developed market rate cuts sooner than domestically constrained investors. Further, they are already benefiting from rate cuts in emerging markets, particularly LATAM, Asia and Central and Eastern Europe (Figure 3).

Figure 3: Emerging market countries are already cutting rates, the US could be one of the last to join in[2]

Don’t miss the fixed income golden age

Rate cutting cycles have only tended to happen every few years. We think this is a golden opportunity for investors to position themselves to fully take advantage of the next one.

Brendan Murphy is Head of Fixed Income, North America at Insight Investment, an investment firm of BNY Mellon Investment Management.

This document has been prepared by Insight North America LLC (INA), a registered investment adviser under the Investment Advisers Act of 1940 and regulated by the US Securities and Exchange Commission. INA is part of ‘Insight’ or ‘Insight Investment’, the corporate brand for certain asset management companies operated by Insight Investment Management Limited including, among others, Insight Investment Management (Global) Limited, Insight Investment International Limited and Insight Investment Management (Europe) Limited (IIMEL).

Opinions expressed herein are current opinions of Insight, and are subject to change without notice. Insight assumes no responsibility to update such information or to notify a client of any changes. Any outlooks, forecasts or portfolio weightings presented herein are as of the date appearing on this material only and are also subject to change without notice. Insight disclaims any responsibility to update such views. No forecasts can be guaranteed.

Nothing in this document is intended to constitute an offer or solicitation to sell or a solicitation of an offer to buy any product or service (nor shall any product or service be offered or sold to any person) in any jurisdiction in which either (a) INA is not licensed to conduct business, and/or (b) an offer, solicitation, purchase or sale would be unavailable or unlawful.

This document should not be duplicated, amended, or forwarded to a third party without consent from INA. This is a marketing document intended for institutional investors only and should not be made available to or relied upon by retail investors. This material is provided for general information only and should not be construed as investment advice or a recommendation. You should consult with your adviser to determine whether any particular investment strategy is appropriate.

Assets under management (AUM) represented by the value of the client’s assets or liabilities Insight is asked to manage. These will primarily be the mark-to-market value of securities managed on behalf of clients, including collateral if applicable. Where a client mandate requires Insight to manage some or all of a client’s liabilities (e.g. LDI strategies), AUM will be equal to the value of the client specific liability benchmark and/or the notional value of other risk exposure through the use of derivatives. Regulatory assets under management without exposures can be provided upon request. Unless otherwise specified, the performance shown herein is that of Insight Investment (for Global Investment Performance Standards (GIPS), the ‘firm’) and not specifically of Insight North America. A copy of the GIPS composite disclosure page is available upon request.

Past performance is not a guide to future performance, which will vary. The value of investments and any income from them will fluctuate and is not guaranteed (this may partly be due to exchange rate changes). Future returns are not guaranteed and a loss of principal may occur.

Targeted returns intend to demonstrate that the strategy is managed in such a manner as to seek to achieve the target return over a normal market cycle based on what Insight has observed in the market, generally, over the course of an investment cycle. In no circumstances should the targeted returns be regarded as a representation, warranty or prediction that the specific deal will reflect any particular performance or that it will achieve or is likely to achieve any particular result or that investors will be able to avoid losses, including total losses of their investment.

The information shown is derived from a representative account deemed to appropriately represent the management styles herein. Each investor’s portfolio is individually managed and may vary from the information shown. The mention of a specific security is not a recommendation to buy or sell such security. The specific securities identified are not representative of all the securities purchased, sold or recommended for advisory clients. It should not be assumed that an investment in the securities identified will be profitable. Actual holdings will vary for each client and there is no guarantee that a particular client’s account will hold any or all of the securities listed.

The quoted benchmarks within this document do not reflect deductions for fees, expenses or taxes. These benchmarks are unmanaged and cannot be purchased directly by investors. Benchmark performance is shown for illustrative purposes only and does not predict or depict the performance of any investment. There may be material factors relevant to any such comparison such as differences in volatility, and regulatory and legal restrictions between the indices shown and the strategy.

Transactions in foreign securities may be executed and settled in local markets. Performance comparisons will be affected by changes in interest rates. Investment returns fluctuate due to changes in market conditions. Investment involves risk, including the possible loss of principal. No assurance can be given that the performance objectives of a given strategy will be achieved.

Insight does not provide tax or legal advice to its clients and all investors are strongly urged to consult their tax and legal advisors regarding any potential strategy or investment.

Information herein may contain, include or is based upon forward-looking statements within the meaning of the federal securities laws, specifically Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements include all statements, other than statements of historical fact, that address future activities, events or developments, including without limitation, business or investment strategy or measures to implement strategy, competitive strengths, goals expansion and growth of our business, plans, prospects and references to future or success. You can identify these statements by the fact that they do not relate strictly to historical or current facts. Words such as ‘anticipate’, ‘estimate’, ‘expect’, ‘project’, ‘intend’, ‘plan’, ‘believe’, and other similar words are intended to identify these forward-looking statements. Forward-looking statements can be affected by inaccurate assumptions or by known or unknown risks and uncertainties. Many such factors will be important in determining our actual future results or outcomes. Consequently, no forward-looking statement can be guaranteed. Our actual results or outcomes may vary materially. Given these uncertainties, you should not place undue reliance on these forward-looking statements.

Insight and BNY Mellon Securities Corporation (BNYMSC) are subsidiaries of BNY Mellon. BNYMSC is a registered broker and FINRA member. BNY Mellon is the corporate brand of the Bank of New York Mellon Corporation and may also be used as a generic term to reference the Corporation as a whole or its various subsidiaries generally. Products and services may be provided under various brand names and in various countries by subsidiaries, affiliates and joint ventures of the Bank of New York Mellon Corporation where authorized and regulated as required within each jurisdiction. Unless you are notified to the contrary, the products and services mentioned are not insured by the FDIC (or by any government entity) and are not guaranteed by or obligations of the Bank of New York Mellon Corporation or any of its affiliates. The Bank of New York Mellon Corporation assumes no responsibility for the accuracy or completeness of the above data and disclaims all expressed or implied warranties in connection there with. Personnel of certain of our BNY Mellon affiliates may act as: (i) registered representatives of BNYMSC (in its capacity as a registered broker-dealer) to offer securities, (ii) officers of the Bank of New York Mellon (a New York chartered bank) to offer bank-maintained collective investment funds and (iii) associated persons of BNYMSC (in its capacity as a registered investment adviser) to offer separately managed accounts managed by BNY Mellon Investment Management firms.

Disclaimer for Non-US Clients: Prospective clients should inform themselves as to the legal requirements and tax consequences within the countries of their citizenship, residence, domicile and place of business with respect to the purchase and ongoing provision of advisory services. No regulator or government authority has reviewed this document or the merits of the products and services referenced herein.

This document is directed and intended for ‘institutional investors’ (as such term is defined in various jurisdictions). By accepting this document, you agree (a) to keep all information contained herein (the ‘Information’) confidential, (b) not use the Information for any purpose other than to evaluate a potential investment in any product described herein, and (c) not to distribute the Information to any person other than persons within your organization or to your client that has engaged you to evaluate an investment in such product.

Telephone conversations may be recorded in accordance with applicable laws.

© 2024 Insight Investment. All rights reserved.

[1] Bloomberg, Insight calculations, May 2024. Past performance is not indicative of future results. Investment in any strategy involves a risk of loss which may partly be due to exchange rate fluctuations.

[2] Macrobond, National Sources, May 2024

Vanilla is extending its estate planning tech to Callan Family Office's ultra-high-net-worth business, while WealthFeed's organic growth engine will now be available to roughly 100 advisors at The Mather Group.

“We are helping families take an important first step toward building a financial foundation for the next generation,” said Franklin Templeton CEO Jenny Johnson

Richard Brothers Financial Advisors joins the fee-only RIA, adding its first Maine office and $240 million in client assets

Cleveland RIA grows to $68 billion in assets as Philadelphia team, deepening its high-net-worth and retirement-plan practice.

Financial planning leaders say unresolved rules on fees, Roth conversions and financial aid complicate comparisons with 529 plans.

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income

Direct indexing is on pace to outgrow ETFs and mutual funds. Northern Trust's Ken Lassner explains why the advisors who get it wish they had started sooner.