The ripple of wealth management firms — including super-sized registered investment advisers — seeking both riches for executives and investor capital to feed expansion plans via an initial public offering looks as if it’s turning into a wave.

And many mega RIAs are backed by private equity investors, who invested in the first place because firms typically kick off returns of 25% to 35% of revenue. Those private funds are looking to cash out and eyeing the public market in some instances to do so.

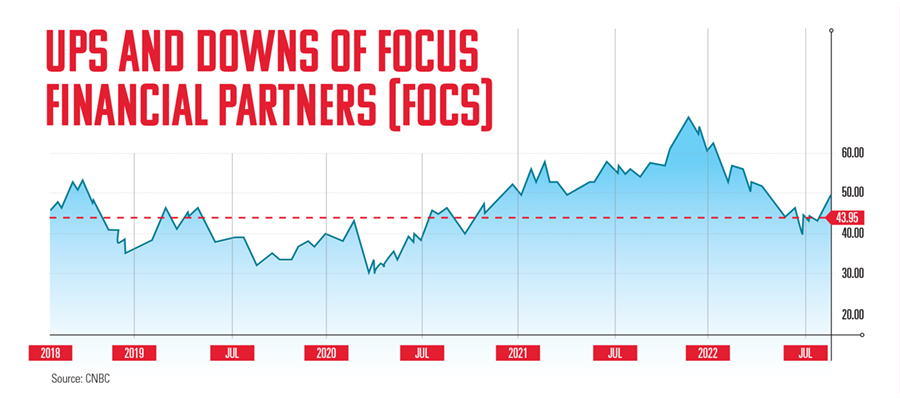

This RIA IPO wave has been building for years. Four years ago, Focus Financial Partners Inc., a longtime buyer and aggregator of RIAs, had its initial public offering, and as of Aug. 10 it was trading at $42.18 per share, an increase of 27.8% from its initial offering price of $33 per share.

It’s not easy being a public company and riding the storm of the public markets. Since its IPO in July 2018, Focus Financial Partners (FOCS) shares have hit an intraday low of $12.17 during the March 2020 market sell-off caused by the Covid-19 pandemic and traded as high as $69 last November, when the market was cresting before its most recent dive into bear market territory.

But Focus Financial Partners’ success as a public company that buys RIAs didn’t lead to an instant flood of copycats, or firms looking to replicate its success. Sure, plenty of other RIA aggregators, often backed with heaps of private equity money, which Focus Financial Partners mostly shunned, have come to the fore as industry standouts. Yet the public market for RIAs or other wealth management firms that provide services for advisers remained quiet — until last year.

That’s when The Tiedemann Group, a New York-based investment and wealth management firm, and Alvarium Investments Ltd., a London wealth management and investment firm with global reach and an RIA in Miami, said they were, first, merging, and, next, combining with Cartesian Growth Corp. (GLBL), a special purpose acquisition company. (Also known as blank-check companies, SPACs were the investment darlings of the Covid-19 pandemic but have fallen out of favor this year.)

The new business combination embraced its potential. According to an investor presentation outlining the deal, the Tiedemann/Alvarium venture expects to have more than $100 billion in client assets by 2026 as compared to $54 billion at the end of 2020.

More importantly, the Tiedemann/Alvarium deal appears to have triggered a rush to the IPO door this year by wealth management firms and mega RIAs.

Dynasty Financial Partners, a service company that supports wirehouse representatives who break away to become independent advisers, filed for its IPO in January. St. Petersburg, Florida-based Dynasty, a longtime leader in the independent RIA industry, is seeking to raise $100 million through its IPO, and the stock will list on the Nasdaq under the ticker DSTY.

Then in April, Toronto-based RIA aggregator CI Financial (CIXX) said it planned to file an IPO this year for its fast-growing U.S. wealth management business. Since entering the U.S. wealth sector in early 2020, CI has become the country’s fastest-growing wealth management platform, and its U.S. wealth management business has grown to become CI’s largest business unit by assets.

At the time, CI Financial said that once its outstanding RIA acquisitions had been completed, its U.S. wealth management assets would reach approximately $133 billion.

Others make the IPO rush look like a pile-on. Reverence Capital Partners and its financial services SPAC, Reverence Acquisition Corp., launched last year. Broker-dealer aggregator Wentworth Management Services last month said it was merging with Kingswood Acquisition Corp. (KWAC).

And waiting in the wings, many industry observers believe, are any number of privately held, private equity-backed wealth management firms that are either RIAs or have significant advisory businesses, including Advisor Group, a broker-dealer network, Wealth Enhancement Group, a giant adviser network, and Hightower Advisors, one of the oldest RIA aggregators in the industry.

Still, some senior industry executives, bankers and attorneys sound cautious about the RIA IPO wave, despite the recent rush.

“The question is, how much of these RIAs’ funding should come via equity and how much via long- and short-term debt,” said Mark Tibergien, the former CEO of Pershing Advisor Solutions and a longtime industry executive and RIA proponent.

He said that valuations for some high-profile private equity-backed RIAs reflect long-term growth prospects more than the immediate expectations of an IPO.

“And once they enter into the realm of public registration for an IPO, RIAs add a whole new level of complexity, including Securities and Exchange Commission regulations on their activities and disclosures,” Tibergien said. “They also might end up being a bit more focused on short-term profits to prop up stock prices.”

One challenge, he noted is that most, if not all RIA consolidators — think Focus Financial Partners or CI Financial — are micro-cap or mid-cap companies. And companies of that size, particularly micro-caps with a market capitalization in the neighborhood of $300 million, have trouble finding a following among analysts or institutional investors.

Right now, the RIA IPO wave is more of a story about “supply push” rather than true demand from the market, said Dan Seivert, CEO and managing partner of Echelon Partners, an investment bank that focuses on wealth management firms.

“The financial profile of these companies is not such that the public would be going crazy for them,” Seivert said, but added that the Tiedemann/Alvarium merger stands out, given the focus on high-net-worth investors. “That’s a tough space to get into and a potential reason why other high-net-worth investors would be interested.”

Asked whether private equity investors are seeking to cash out of their ownership of RIAs, Seivert said: “Those firms will just continue to ride the wave of private investors interested in the RIA industry. Being a public company is expensive and difficult. It could cost $1 million to $2 million per year. And then everything management does that may have been confidential is now out in the open.”

But some disagree, believing the market is burgeoning for RIA IPOs.

“Any RIA worth $500 million or more probably has the ability to go public,” said Peter Nesvold, a veteran merchant and investment banker in the financial services industry. “Whether management and the investors want to or not is up to them.”

The aforementioned Focus Financial Partners, for example, this month has a market capitalization in the neighborhood of $3.3 billion. The Tiedemann/Alvarium combination, under the moniker Cartesian Growth Corp., has a projected valuation of $1.4 billion.

“The Tiedemann deal involves a traditional RIA,” Nesvold said. “I think a lot of us are rooting for that deal to be successful. We want to see that happen because it’s an option for firms other than just going to private equity investors.”

The timing has to be right for an IPO. The rough market of the first half of 2022, with the S&P 500 stock index down 21%, is creating potential problems for listings in the second half of this year.

“The public market is a lucrative place to play.”

Brian Hamburger, industry attorney

Indeed, the IPO window “was virtually shut” during the second quarter this year, and venture capital-backed public listings reached a 13-year quarterly low, with just eight completed, according to the most recent Pitchbook U.S. Venture Monitor report.

“This has meant that late-stage companies that may have been on the road to a public listing or that often rely on public market valuations to help price their financing rounds have had to pivot liquidity strategies and cool pricing expectations,” according to the report.

Meanwhile, some SPAC investors are getting nervous and are looking to pull money out of some deals. SPACs have been criticized generally for fees.

Shares are sold at $10 each, often with a warrant to purchase an additional share at $11.50.

But investors pay a price. The new company and its sponsor get a stake called a “promote,” typically paying themselves 20% — a hurdle critics don’t like.

Mergers also had a tough second quarter in which “we saw general sentiment around SPACs continue to deteriorate in light of massive losses in public equities,” according to the Pitchbook report. “Many announced SPAC mergers were abandoned or canceled in the wake of the reset in valuation multiples. SPAC shareholders are likely becoming more risk-averse and strongly considering their redemption rights to get their principal back rather than take on the risks of operating the business.”

Finally, holding back an RIA IPO wave are potential fiduciary problems with a public company registered investment adviser.

“The public market is a lucrative place to play,” said Brian Hamburger, an industry attorney. “But the wealth management firms themselves are heading into dangerous waters. There’s a meaningful distinction when the ownership of these firms is so disconnected from the clients’ needs.”

“RIAs are supposed to be fiduciaries,” Hamburger said. “But the board of directors has dueling interests between the firm’s clients and the fiduciary obligation of the board to the shareholders.”

“So you have another layer of conflict,” he added. “It remains to be seen if independent RIA firms can succeed in this construct.”

Eliseo Prisno, a former Merrill advisor, allegedly collected unapproved fees from Filipino clients by secretly accessing their accounts at two separate brokerages.

The Harford, Connecticut-based RIA is expanding into a new market in the mid-Atlantic region while crossing another billion-dollar milestone.

The Wall Street giant's global wealth head says affluent clients are shifting away from America amid growing fallout from President Donald Trump's hardline politics.

Chief economists, advisors, and chief investment officers share their reactions to the June US employment report.

"This shouldn’t be hard to ban, but neither party will do it. So offensive to the people they serve," RIA titan Peter Mallouk said in a post that referenced Nancy Pelosi's reported stock gains.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.