This month’s edition kicks off with the big news that Vanguard has apparently decided that direct indexing is the future, making its first-ever external acquisition of direct indexing platform JustInvest after an initial pilot program with RIAs quickly brought in more than $1 billion of AUM. Of course, the reality is that if Vanguard is going to put its full scale of resources behind JustInvest and distribute the direct indexing offering to its $3 trillion of assets with financial intermediaries, then it may cause direct indexing to become the future, even if it wasn’t going to be already. On the other hand, with Vanguard deciding to break the mold and acquire externally in an apparent move to quickly catch up, it appears that even Vanguard sees both momentum in direct indexing … and an apparent threat to its own core business of index mutual funds and ETFs that it wishes to head off at the pass?

From there, the latest highlights also feature a number of other interesting adviser technology announcements, including:

Read the analysis of these announcements in this month's column, as well as a discussion of more trends in adviser technology, including:

Be sure to read to the end, where we have provided an update to our popular Financial AdviserTech Solutions Map as well!

#AdviserTech companies that want their tech announcements considered for future issues should submit to [email protected]!

Direct indexing has been around for more than 20 years, since early pioneers like Parametric originated the strategy as a way to gain tax efficiency for ultra-high-net-worth clients, and it gained additional visibility nearly seven years ago when robo-adviser upstart Wealthfront made the case for “democratizing” direct indexing for mass affluent investors. But in practice, adoption of direct indexing strategies has been relatively limited, a niche separately managed account offering for HNW clients through players like Parametric and Aperio that failed to gain much traction with consumers given the complexity of the sale.

Notably, though, while direct indexing largely originated as a tax alpha strategy, in which owning the individual stocks of a major index makes it possible to do tax-loss harvesting at the individual lot level, such that even if the index is up, at least some stocks in the index will likely be down and can be harvested, in recent years a number of new technology upstarts have entered the game, making the case that once an index can be disaggregated into the component stocks and managed through technology, it can be adapted in any manner the adviser or client want. For instance, advisers can build their own SRI models by filtering an index at the individual stock level, clients can express their ESG preferences by requesting an overweight to green energy and underweight to vice stocks, advisers can build their own proprietary strategies implemented at the stock level (e.g., a factor-based investing approach where the adviser directly overweights small-cap and value), or entirely client-customized portfolios can be constructed (e.g., building a core S&P 500 index holding by using the existing low-basis stocks the client already had previously and using the direct indexing tools to build the completion portfolio around them).

The growing buzz around direct indexing culminated last fall in big companies starting to make big bets that direct indexing’s time had come. Morgan Stanley acquired Parametric (via its purchase of Eaton Vance) for $7 billion, followed shortly thereafter by BlackRock buying Aperio for $1 billion. That, in turn, spawned a wave of major investments into newer direct indexing players, from Fidelity staking Ethic Investing with $29 million and JPMorgan acquiring OpenInvest, to storied Silicon Valley venture capital firm Sequoia staking Vise at a whopping $1 billion valuationon just $250 million of total AUM. Which begins to create a self-fulfilling prophecy: When existing direct indexing players are bought for billions, and new startups receive nearly $100 million of venture capital to become the next billion-dollar direct indexing players themselves, the hyper-funding of the direct indexing thesis makes it a reality. Especially when it is coupled with growing pressure on financial advisers themselves to differentiate in an increasingly commoditized world of investment management — for which direct indexing allows for the ultimate in adviser-level customization and client-level personalization.

In this context, it is perhaps not surprising that even indexing pioneer Vanguard is suddenly feeling the competitive threat, leading Vanguard to make its first-ever external acquisition by buying JustInvest to become its own direct indexing solution on the tail of a 2020 pilot program that quickly garnered $1 billion of AUM. Notably, Vanguard emphasized that JustInvest will specifically augment Vanguard’s “financial intermediary business” — in other words, not to replace the popular index mutual funds and ETFs that Vanguard sells to consumers, but specifically to ameliorate the risk that financial advisers stop using Vanguard’s popular index funds in an effort to use direct indexing tools to differentiate themselves with more customized client portfolios. While it was Parametric’s tax alpha approach that garnered the original interest in direct indexing, creating more customized portfolios — “custom indexing” as opposed to “direct indexing” — is the approach that appears to be gaining more momentum, especially at the intersection of rising consumer interest in ESG and adviser pressure to differentiate, which JustInvest solves for with its Kaleidoscope offering.

At this point, direct indexing still hasn’t fully proven it can expand into a mainstream solution beyond its niche roots. Though Vanguard’s decision to acquire JustInvest suggests the company sees (or fears?) real direct indexing momentum is coming — so much that it couldn’t even wait to build its own solution but had to try to leapfrog ahead with an acquisition instead. Which, again, may soon become a self-fulfilling prophecy, as when BlackRock and Vanguard decided a decade ago to make ETFs the future, ETFs over mutual funds became the dominant investment story of the 2010s. So now that Blackrock has Aperio and Vanguard has JustInvest, and both are making their bets that advisers using direct indexing tools to create their own customized indexing solutions will be the next big thing of the 2020s, it seems increasingly inevitable that it will be?

The traditional allure of active portfolio management has been the opportunity to outperform the markets, either by doing a better job of selecting the winners (investments that go up) or avoiding the losers (investments that go down). Yet the unfortunate reality is that study after study shows that the majority of managers fail to beat their benchmarks (at least, net of fees), such that in the end, often the best pathway to growth is simply to minimize fees and stay the course through the volatility, rather than trying to avoid it. Those who don’t want to have such a bumpy ride can simply own less risky stuff in the first place (i.e., by owning more bonds and less in stocks), and/or to spend more conservatively to be able to better wait out the volatility when it comes (e.g., the safe withdrawal rate approach).

The irony, though, is that because of the compounding effects of “good” stock returns over time, those who do manage to own substantial holdings in equities, stay the course and keep their withdrawals conservative often end up compounding far more in their portfolios than they actually needed in the first place — such that those who invest in a balanced portfolio and take a conservative withdrawal rate have an equal likelihood of either spending down all of their principal or accumulating more than 9X(!) their original nest egg over the same multidecade time horizon. In other words, the long-term compounding growth rate on stocks requires some conservatism or risk management to avoid early depletion, but doing so also increases the likelihood of accumulating far more than what we wanted or needed in the first place. Which raises the question of whether a better approach might be to more surgically manage risk by choosing to carve off the extreme upside of return outcomes in exchange for being able to hedge at least a portion of the downside — an options strategy known as a collar, in which the investor sells an out-of-the-money call option (giving up the upside beyond that point) and uses the proceeds to buy an out-of-the-money put option (eliminating any losses below that point).

The problem, though, is that most advisory firms are not built to manage complex options strategies like collars, especially when doing so would require implementation across a wide range of clients, with a wide range of holdings that need to be collared, with varying strike prices and time horizons depending on when they came on board, which can’t always be purchased in certain types of accounts (e.g., IRAs), and then have to be re-upped when the options expire (and/or implemented with longer-dated options that may not be accessible or tradeable on most adviser platforms). That has led in recent years to a wide range of packaged products to achieve the same collared outcomes, from structured notes and defined-outcome ETFs to registered index-linked annuities (RILAs), that achieve substantively similar outcomes but in a stand-alone product format that is far easier to purchase and implement systematically for clients.

Simon Markets — which in 2018 spun off from Goldman Sachs to create a structured note marketplace and has since expanded into the RILA marketplace as well — has quickly grown to $25 billion of flows from financial advisers in 2020 alone, and is now announcing a whopping $100 million capital round to accelerate the growth of its marketplace of risk-hedged investment vehicles. The appeal of a platform like Simon, in particular, is that historically, the structured notes marketplace has been relatively inefficient (with a number of suboptimal products with high internal costs that are difficult to glean because the packaged nature of the product makes it impossible to see how much interest spread or other internal markups have been priced in). The annuity marketplace similarly has been plagued with inefficiencies that result in the products with the most marketing and highest commissions (even if they have higher costs, which often they must have to recover those higher distribution costs) dominating investor flows over the annuities that are objectively the best in a fair comparison. A marketplace like Simon makes it possible to more easily compare products on equal footing, making it easier to actually figure out which ones are good for clients to implement.

Notably, the industry has spent nearly 20 years debating and trying to figure out the best way to package risk-hedged investment offerings — from indexed annuities and RILAs to structured notes, defined-outcome ETFs to the good old-fashioned hedge fund. Ultimately, though, Simon is simply positioning itself to participate in whatever vehicle turns out to be dominant — offering all of the above as choices — and is betting that in the long run, as long as advisers still don’t have a scalable way to manage options collars across their entire client base directly, but more and more clients are willing to give up excess upside in exchange for eliminating at least some of their downside, there will be growing demand from advisers looking for a marketplace to shop for the best version of that risk-hedged solution — implemented via whatever vehicle it may be.

Over the past decade, there has been an immense focus on technology that can automate investing for consumers — so-called robo-advisers — and the subsequent shift of applying that same robo technology to make advisers’ back offices efficient as well. But the reality is that brokerage accounts are not the only way that consumers save. In fact, for the average American, the bulk of their savings isn’t even in an investment account; it’s the equity in their home and the balance in their 401(k) plan.

The caveat when it comes to financial advisers, though, is that for many understandable reasons, most adviser-facing technology is designed to help people with hundreds of thousands of dollars, up to hundreds of millions, or even billions in net worth. There’s nothing wrong with that, and for a long time, it was borderline impossible to build a successful advisory practice without serving those types of clients.

In addition, there has sadly been very little progress or innovation in the workplace savings channel because, frankly, it has been a low-profit, low-margin channel that’s fraught with regulatory risk. That has left many with a 401(k) user experience that looks as if it is stuck in the 1990s, or early 2000s at best, because the ones who have the distribution achieved it by offering technology for free, so long as the workplace used their asset management products. In other words, the 401(k) technology platforms were loss leaders for the asset managers, which not surprisingly woefully underinvested in those user experiences because it wasn’t their core business.

But now, as robo technology to automate the adviser’s back office expands, there is not only a growing focus on going down-market to serve more average Americans, there’s also a shift across channels to help bring advice to the average American via employer retirement plans (and not just the taxable investment account or IRA). Upstart technology providers see the opportunity to transform the 401(k) business by building technology that is focused first and foremost on the end-client experience and using that adoption to drive interest up the distribution chain.

In that vein, Vestwell launched back in 2016 with a vision of bringing the robo-tools that were emerging at the time to support advisers serving the 401(k) channel in particular. Over the years, Vestwell has quickly added infrastructure to power several other payroll-deducted savings programs as well, including health savings accounts, individual retirement accounts, 529s, emergency savings accounts and more. It’s all built around not trying to compete with advisers for this business but empowering them to serve more of this type of business.

Now Vestwell has announced that it is raising a fresh $70 million round of capital to continue its mission to help transform workplace savings for small and medium-size businesses. Notably, a key participant in Vestwell’s latest round is Morgan Stanley, which announced that along with the funding itself, it is rolling Vestwell out to its 15,000 advisers, which will be a huge boost for Vestwell’s 401(k) distribution. That’s key at its current stage of scaling, where the more distribution it has, the more economies of scale it will get, which will allow it to more profitably serve the rest of the marketplace.

In fact, it wouldn’t be surprising to see Vestwell use some of this capital to buy assets, entering the fray of acquiring retirement plan record-keeping businesses from those looking to offload those plans in the even-more-regulatorily-challenging Department of Labor and Reg BI environment (and increasingly Vestwell’s distribution and scale in the process). Alternatively, Vestwell may also begin to acquire smaller technology businesses that allow it to expand its own vertical integration; for instance, today Vestwell has great payroll integrations, but acquiring its own payroll provider would provide even more scale and revenue. As frankly, there’s just only so much to be built in technology itself — on top of what Vestwell already has — or spent on marketing to advisers, from a $70 million war chest, without deploying some of that capital for acquisitions as well.

The key point, though, is simply that it’s game-on for a technology renaissance in the 401(k) channel, as the combination of shifting regulatory winds (DOL fiduciary and Reg BI), plus a change in the business and distribution model (as regulators force a separation of behind-the-scenes cross-subsidies that make it more difficult to use technology and record-keeping as a loss leader) is opening the door for new entrants. Especially among financial advisers, who increasingly are looking at the employer channel as a pathway to serve more clients (but don’t want to get bogged down in the administrative tasks that technology can automate).

In the meantime, with Goldman Sachs, Wells Fargo and Morgan Stanley all now on Vestwell’s cap table, one has to wonder how long it will be until one of them makes Vestwell an offer it can’t refuse? Only time will tell, but any sizable exit for Vestwell — especially in just five years since its founding — highlights the fact that despite the buzz of the 2010s that technology would replace human financial advisers, in reality, it’s the technology that supports human financial advisers that is driving the most growth. There has never been a better time to be building adviser-facing software!?

The traditional approach to risk tolerance is a very one-dimensional evaluation of a client’s ability to take risk, typically scored from a range of questions that cover everything from time horizon to investing experience to the infamous question of whether you’d sell, hold or buy more stocks in the event of a market downturn.

In recent years, this one-dimensional risk tolerance framework has begun to give way to a more two-dimensional view of risk, in which risk tolerance (willingness to take risk) is measured separately from risk capacity (financial capability to take risk), recognizing that even if someone can afford to take risk (e.g., significant assets and a long time horizon), if they don’t want to take risk and don’t need to take risk (i.e., low risk tolerance), then they probably shouldn’t.

But the reality is that even when a portfolio aligns to a client’s tolerance and capacity for risk, some clients are simply more behaviorally inclined to keep their composure when the volatile markets come, while others are highly prone to misperceive the risks they’re taking and overreact. Which means even for two clients of identical risk tolerance and capacity, differences in this third dimension — composure — can also result in drastic differences in client behavior that must be managed.

In practice, though, few risk tolerance tools delve so deeply into these second and third dimensions of risk. Through its 2020 acquisition of Brinker Capital, though, Orion added Dr. Daniel Crosby to its staff. Crosby, who has a Ph.D. in psychology (with a focus on behavioral finance), was building a behavioral finance tool prior to the acquisition called Tulip. Now Orion appears to have harnessed Crosby’s knowledge and experience in behavioral finance and building Tulip to launch its new 3D Risk Profile tool.

At its core, Orion’s new 3D risk profiling tool aims to capture all three dimensions of risk — tolerance, capacity and risk composure — by assessing the client’s tendency to be anxious about volatility, to help advisers identify which clients are most likely to be overly elated in bull markets or overly stressed in market declines. In essence, the goal of this new Orion risk tool is to try to predict how a client will respond to expected volatility and allow the adviser to be a better coach for their clients when the market returns are inexplicably good or stressful.

Notably, using risk tolerance assessment tools to facilitate better client conversations isn’t entirely new. Riskalyze’s tools similarly help to quantify how much volatility a client’s portfolio might experience (e.g., within a 95% confidence interval), to facilitate the adviser-client conversation: “While these are big swings, they are expected for a portfolio like this and none of your goals are in jeopardy at the moment. If we begin to get outside of this portfolio’s expected ranges of volatility, we will have a conversation together and take action from there.”

Still, though, Orion’s solution remains unique because it doesn’t just aid in the conversation at the time of volatility (based on expectations that were set in the risk assessment process), it is the first tool that aims to allow advisers to preempt those conversations with their clients via psychological profiling. “Hello, Mr./Mrs. Client, you have a tendency to act or think a certain way when the market performs like this. Here is our recommendation, and what we have been doing for you during these times of volatility.”

Or, as Orion CEO Eric Clarke said, “Using technology to augment human compassion and insight is the new frontier of fiduciary service.”

Within the next decade, will measurable risk composure scores and psychological profiles become part of know your client requirements for fiduciary advisers? Only time will tell, but this development is only positive. The more that risk becomes core to client conversations, rather than a box to be checked for suitability requirements, the better off we will be.

While Riskalyze has been the risk tolerance software provider to beat in the competitive landscape for nearly a decade, the reality is that it’s not the longest-standing provider of risk tolerance software for advisers. That honor goes to Finametrica, which was developed in the late 1990s to be the most academically rigorous assessment of risk tolerance, in an era where virtually all firms simply used homegrown risk tolerance questionnaires designed by compliance departments that may have been deemed sufficient for compliance purposes but did a poor job actually assessing a client’s tolerance for risk. Simply put, writing good risk tolerance questions is actually a very hard thing to do.

The caveat, though, is that the best questions for assessing risk tolerance are free from industry jargon and may not overly focus on market volatility at all, instead drilling down to the more abstract trait that is our psychological tolerance for engaging in risky trade-offs. The good news is that there’s an entire branch of psychology — called psychometrics — that exists to provide a process for creating valid and reliable assessments of such abstract psychological traits. The bad news is that it means, almost by definition, that the best risk tolerance assessment questions will have no clear connection to actual client portfolios. Which makes it very hard for the adviser to know what to implement once the client completes the process!

Accordingly, it’s notable that this month, Morningstar announced the launch of a new Morningstar Risk Ecosystem, which builds upon the Finametrica risk tolerance assessment tool it acquired via PlanPlus early last year, with a specific focus to solve for the gap between abstract risk tolerance assessment and concrete portfolio implementation.

Unsurprisingly, Morningstar is taking a more academic approach to the problem and is building on its Risk Profiler tool with two new additions: a Morningstar Portfolio Risk Score that allows advisers to score their own portfolios for riskiness, and a Risk Comfort Range that provides the missing link by mapping a client’s Risk Profiler score to the range of Portfolio Risk Scores that would be appropriate for them. In other words, Morningstar created a framework to score any adviser’s model (or more client-customized) portfolios, and map which of those adviser models fits the client’s (abstract) risk tolerance score.

It’s worth noting that Morningstar’s approach still remains relatively one-dimensional — at least relative to the three-dimensional approach with tolerance, capacity and composure being taken in Orion’s recent launch. In the end, the primary goal of its new offering appears to be a desire to definitively resolve Finametrica’s longest-standing challenge — the gap in how to map abstract risk tolerance scores to a concrete portfolio the adviser can recommend and implement for the client. Though given Morningstar’s sheer reach — and the fact that its new Risk Ecosystem will be embedded into Advisor Workstation and Morningstar’s enterprise components — its new risk framework is likely to see rapid adoption (at least among its existing base of advisers).

With both Morningstar and Orion launching free risk tools embedded in their platforms, one has to wonder whether this is an existential threat to other players like Riskalyze, Totum Risk, Tolerisk, Risk Pro or Pocket Risk, or if it is a “rising tides lift all boats” situation? Though, in the end, when the T3 Advisor Technology survey still shows that the overwhelming majority of advisers don’t use any risk tolerance software at all — instead ostensibly just relying on client conversations and compliance-created assessments — it appears that risk tolerance software solutions still have ample room to grow?

When robo-advisers first arrived, the vision was to put human financial advisers out of business, on the grounds that it shouldn’t take hours of work and thousands of dollars to open an investment account and implement it into a diversified asset-allocation portfolio. The reality, though, is that account opening is not the core value proposition of the human financial adviser, either; in fact, when the robo-advisers arrived, most human advisers said they wished they had such efficient technology tools as well, to free up more of their time to provide their real value-adds to clients. Stated more simply, robo-advisers were never actually an alternative to the human financial adviser; they were a replacement for the adviser’s back office.

In fact, one of the most surprising aspects of advisory firms over the past decade is that the explosion of technology has brought virtually no measurable increase in adviser productivity as measured by revenue/professional or clients/professional. It has, though, brought about significantimprovements in back-officeproductivity, as advisory firms today drive nearly 26% more revenue/staff compared to the early 2010s, with the rise of everything from better digital onboarding tools to more CRM-driven processes and workflow engines.

The end result of this trend is that a growing number of AdviserTech firms are trying to get into the business of back-office automation for advisory firms. In some cases, the shift comes from platforms that showed up as digital onboarding robo-tools — e.g., AdvisorEngine — that have expanded further into the back office (e.g., AdvisorEngine acquiring Junxure CRM). In other cases, though, the pivot comes from AdviserTech solutions that started even further in the back office — e.g., Docupace and its cloud-based document management solution — and are expanding further into all of the back-office workflows associated with those documents.

In that context, it’s notable that Docupace recently announced the acquisition of Jaccomo. Nominally Jaccomo was in the business of helping broker-dealers handle adviser compensation — in particular, calculating commissions from a wide range of sources and ensuring the right commissions with the right splits received the right payout rights and were deposited in the right adviser’s bank accounts, with its jCore solution. Over the years, that has expanded further into facilitating data integrations (given the amount of data that Jaccomo had to parse through in order to determine compensation), and compliance oversight (given the amount of data on which Jaccomo could do real-time surveillance). All of which can complement (and be integrated with) Docupace’s own document management (and the onboarding and workflow systems it has built with it) to expand into (and automate) even more of the broker-dealer’s back office.

From the broader industry perspective, the significance of the Docupace acquisition is that while so much of the focus of robo tools has been on client portals, onboarding, and the front-end client experience, there is a quiet war underway to take over, consolidate and automate the adviser’s back office, creating the potential that in the future, adviser platforms may seek to differentiate themselves not by the amount of service support they provide for the home office, but how little service support their advisers will need in the first place (thanks to back-office automation).

Historically, the compliance business was a business of consultants that provided advice on compliance systems and processes, which initially were paperwork-driven processes but more recently have increasingly been enshrined in technology, from CRM workflows to social media archiving to cybersecurity.

In 2018, though, private equity firm Aquiline Capital took a stake in RIA In A Box, turning what was historically a compliance consulting solution into a technology-based SaaS business that provides a compliance platform that advisory firms can use to manage their own compliance obligations, along with the consultants necessary to provide advice about more customized needs.

In the years since, RIA In A Box has increasingly expanded its technology capabilities around various compliance functions, from vendor due diligence to employee trade monitoring, in addition to the upfront RIA registration and ongoing RIA compliance.

Now RIA In A Box has announced the rollout of a new digital archiving solution for websites, email and social media accounts, along with the associated communications review workflows to monitor for keywords.

While compliance isn’t always the most fun topic to bring up at a dinner party, it is a necessary part of running any practice. RIA in a Box is on the path to helping advisers consolidate many compliance-related functions into one solution. This seems to be a trend across the industry, as the pendulum swings back from completely open architecture and trying to integrate best-of-breed platforms to the appeal of having one vendor that does it all (at least in a single category) and makes it all just work together. In other words, why have a stack of 15 vendors when you can have five that cover the key areas? After all, reducing the adviser technology stack of vendors by 10 also reduces integration points of failure, contract renewals, cybersecurity risk and the number of tech support conversations by 10. It also likely eliminates a lot of redundant functionality that multiple vendors have as more and more try to expand into increasingly overlapping domains. (How many times does the typical advisory firm pay for redundant client portals!?)

RIA In A Box appears particularly well positioned in the compliance domain. While advisers often form deep attachments to financial planning tools (e.g., MoneyGuidePro or eMoney or RightCapital) or portfolio management tools (e.g., Orion or Black Diamond or Tamarac), because they’re at the center of client conversations that repeat over and over (and advisers thus get very comfortable and don’t want to change their conversations), it’s rare to meet anyone who was particularly loyal to their social media archiving vendor. That provides the opportunity for consolidation in compliance technology — or RIA in a Box simply building each component for itself and offering it as part of an ever-growing all-in-one compliance platform — even more appealing when executed well.

Owning equity in a (fast-growing) company has long been one of the best ways to build significant wealth, and with the explosion IN tech over the past few decades, many are getting access to equity and creating wealth in ways they never have before. However, few things are as confusing or as complex as the tax aspects of equity compensation from an early-stage growth company. The stakes are high, since typically people only get one shot at a major liquidity event such as a company being sold or going public, and poor advice can be extremely costly when it comes to stock options and other equity vehicles.

Enter Harness Wealth, which provides a matchmaker platform to pair (prospective) clients facing complex equity decisions with specialized service providers such as advisers, attorneys and tax professionals (along with its own in-house Harness Tax offering).

Like other players in the increasingly popular category of lead generation services for advisers, Harness generates its revenue by being paid referral fees from the firms it connects clients to. It will likely be able to generate above-average fees from each referred client, simply given the concentration of wealth associated with equity compensation and private company liquidity events. In other words, lead generation services targeted at a niche of above-average-wealth consumers have the potential for above-average referral fees for Harness.

In that vein, it’s not entirely surprising to see that Harness Wealth has now raised a $15 million round of financing, funded in part by the very venture capital firms that are also funding other technology startups whose future IPOs, SPACs, acquisitions and other liquidity events may fuel future Harness clients!

Harness will still have to live or die by the same challenge that faces any lead generation platform — how to scalably generate the volume of leads necessary to refer affluent (equity compensation) clients to advisers to earn their referral fees. It’s notable that even as lead generation platforms are only just now really getting underway with the recent funding rounds of SmartAsset’s SmartAdvisor, Zoe Financial and the like, the shift from generalist to specialist is already underway as Harness aims to distinguish itself from the others with its particular equity-compensation focus.

Time will tell, but Harness is tapping into a very real need for many people. Look at Robinhood’s recent IPO; it has more than 1,000 employees, most of whom are the exact demographic for what Harness is offering. And Robinhood’s growth story is just one of many.

One of the greatest challenges in the financial advice business is simply getting clients who will pay for financial advice. Not that there isn’t a willingness and interest to pay for advice among a growing number of consumers. But given the low trust levels of the financial services industry, and the reality that it’s very difficult for a prospective client to figure out whether or not an adviser is actually any good at what they do (not to mention whether the adviser is a fit for that client in particular), adding clients is difficult. That’s why a recent Kitces Research study found that the average client acquisition cost for financial advisers is a whopping $3,119 per client.

Today, the increasingly popular solution to this matchmaking challenge is for financial advisers to specialize in a niche, such as Chick-Fil-A operators or even bass fisherman. It narrows the universe of clients who will work with a particular adviser, gives the adviser an opportunity to build a reputation and become known among at least a particular segment of (ideal) clients, and if they find each other, it’s likely that it will be a mutual fit.

For most businesses and industries, though, the process of finding the right fit has become simpler thanks to the rise of the internet and an ever-growing number of platforms that provide reviews of service providers, from Angie’s List to Yelp. From the consumer’s end, the process can be simplified down to: Which providers have the capability to solve my problems and have good reviews from other people who are able to affirm the provider did a good job?

For financial advisers, this wasn’t a feasible path because for decades industry regulations barred advisers from soliciting and using client testimonials in their marketing. But with the recent SEC rule change now permitting testimonials in full effect, new platforms are emerging to fill the void.

The latest example is Finance Friends, which has launched as something akin to a “Yelp for Advisers” approach to crowdsource consumer reviews and identify the best financial advisers. Clients can confidentially submit information about themselves and their desires, search advisory firms that seem to be a good fit, match with an adviser on the spot or even do a live chat as a means of providing a lower-commitment way of engaging with an advisory firm. Once matched, consumers can return to leave a review for the adviser’s services that will help guide others in the future.

Conceptually, this approach is clearly appealing. But Yelp works great for finding a restaurant or a coffee shop because the consequences are limited if it doesn’t work out. The consequences for a poor decision about a financial adviser are tremendously high, and the switching costs when an adviser relationship doesn’t work out are painful. (Which is why so many clients stay with relatively mediocre advisers year after year!?) Which raises the question of whether consumers will really trust finding a financial adviser through third-party reviews the way they do when looking for dinner on a Thursday night?

On the other hand, given that the financial advice business is so confusing for consumers, a case can be made that a Yelp-for-Advisers platform may be especially appealing, because the average consumer doesn’t know how to vet whether an adviser is really expert enough, which makes reviews from other clients of the adviser especially appealing as a guide. Still, though, Yelp works because the average business has thousands of patrons over time, such that even if just 1% to 2% of them leave reviews, it’s possible to get to a critical mass of feedback that guides the decisions of others. Whereas if the average adviser has fewer than 100 individual clients, there may only be one to two reviews per adviser, which isn’t very compelling. Ironically, it would only be the mega advisory firms, with multiple advisers all collecting reviews for the firms, that would likely achieve the necessary volume of reviews to convey trust. Which doesn’t exactly solve the matchmaking problem, as the largest advisory firms already have the most scale to market themselves (it’s the solo advisers who struggle the most).

Of course, even if the Yelp-for-Advisers model can work, it’s still necessary to solve the infamous chicken-and-egg problem of review sites — consumers won’t use it until there are enough reviews to be useful, but it’s hard to get enough reviews until consumers start using it. Will Finance Friends be able to get the flywheel going? We’ll see.

Building a prospective investment portfolio for a client to achieve their goals involves first and foremost doing analysis on the available investment universe to determine what the good investments are for a particular investment objective. While the particular investment building blocks may change over time — from stocks and bonds in the early days, to mutual funds, ETFs and a growing number of alternative investments — the need to analyze the data to make the investment selection is ever present. Over the years, that’s spawned an entire category of tools to provide the requisite investment research and analytics, from the old stalwarts like Morningstar and Bloomberg to more recent up-and-comers like YCharts and Kwanti.

When it comes to the recent boom in cryptocurrencies, though — from Bitcoin to ethereum to the infamous dogecoin — the reality is that the data are still limited and not so readily available, at least at the depth and level to which advisers constructing client portfolios would typically expect. In fact, the dearth of crypto data has spawned a number of startups that aim to fill the void by collecting and (re-)selling the data, in a form of Morningstar for crypto solution.

The latest newcomer in the space is Fidelity. Its Fidelity Center for Applied Technology innovation team developed “Sherlock.” For $500 a month, advisers can use Sherlock to leverage a Bloomberg-style dashboard of price and volume data on a wide range of cryptocurrencies, back-test investment models based on that historical data, track news coverage and social media trends, and soon be able to track derivatives on cryptocurrencies as well. In essence, it’s everything that a cryptocurrency trader might want.

The caveat is that it’s not clear that advisers are looking to trade cryptocurrencies for their clients anytime soon, in a world where advisers are less and less likely to trade any kind of individual security, instead preferring pooled investment vehicles like mutual funds or, where a more active strategy is desired, utilizing ETFs as the trading unit of choice. Especially given that an adviser can get the analytics on everything else they might choose to invest in for less than the fee that Fidelity’s Sherlock would charge for just the data and analytics on cryptocurrencies alone.

The reality is that a number of other startups trying to build businesses around cryptocurrency data have already been struggling or shut down entirely as the companies struggle to find a critical mass of traders who are willing to pay for data, given that retail investors typically don’t buy professional platforms, while the SEC’s limitations on pooled cryptocurrency vehicles (i.e., no crypto mutual funds or ETFs, at least thus far) eliminates most asset managers as a potential, and advisory firms typically aren’t day trading anything (whether stocks, bonds or crypto).

In the long run, if cryptocurrencies do continue to gain momentum, it seems likely that at some point, they will be incorporated into other investment vehicles — e.g., an eventual SEC approval of cryptocurrency ETFs — which may both expand the market of firms that would buy crypto data solutions like Sherlock and provide a more likely pathway for advisers themselves to begin to make at least small allocations of client portfolios into cryptocurrency. But for the time being, it doesn’t seem likely that an advisory firm would pay Fidelity’s Sherlock as much or more for just crypto data than it might be paying for each adviser to have research tools for everything else they invest in for their clients?

Despite the forecasts a decade ago that robo-advisers and commoditization would decimate the human adviser business, in practice robo-advisers have struggled to grow while the human advice business is flourishing, to the point that strong growth and healthy margins have led to one record-breaking year after another for advisory firm mergers and acquisitions, with a reported “50-75 buyers for every seller,” and so many dollars chasing so few advisory firms for sale that advisory firm valuations are also setting new records year after year, from what was historically an average of 2X revenue (or a valuation of about 1.5% of AUM given an average revenue yield of 0.75%) to deals that are rumored to be happening at 2.5X to 3X revenue (or a valuation of roughly 2% of the firm’s AUM). Accordingly, even back in 2016, a number of heads turned when Ron Carson’s advisory firm sold a 29% stake to Long Ridge Equity Partners for $35 million, valuing what at the time was $6 billion of Carson AUM at $120 million (or about 2% of the firm’s AUM).

This month, Carson Wealth announced that Long Ridge was exiting, Bain Capital was taking over its stake (coupled with a fresh infusion of cash for additional growth), and Carson’s now $17 billion of AUM was being valued at a stunning $1 billion-plus of enterprise value. That means after growing AUM by just about 3X in the past five years, Carson was being priced 8X higher in enterprise value, expanding its price tag to nearly 6% of its AUM, and raising questions about whether Carson has set a new high-water mark in the incredibly buoyant valuation of RIAs. Notably, though, in its announcement, Bain didn’t say that it was acquiring an RIA or a wealth management firm, but a “financial technology and services” leader, suggesting that Carson Wealth may not have been valued as an RIA at all, but first and foremost as a tech company (that also does wealth management!?)?

From a revenue perspective, Carson is in the traditional wealth management business, with both an employee RIA model (Carson Wealth) and a TAMP platform for affiliated advisers (Carson Partners), alongside a practice management platform called Carson Coaching. But unlike most advisory firms, it has built its own proprietary layer as well — in particular, Carson CX, a client portal that clients can use for their own personal financial management (akin to Mint.com, eMoney or Personal Capital). Carson has indicated that in the future, that portal will be available not only to Carson clients, but also to the broader public whose lives are less complex and don’t need an adviser — at least, not yet.

In other words, Carson CX appears to be getting positioned as a lead generation portal for prospects, who can aggregate assets, keep track of their finances — and provide a direct conduit for Carson to reach out to them when they have accumulated enough wealth to become a client, just as Personal Capital did over the past decade to power its own growth. (The key to Personal Capital’s success was using its PFM portal not just for business efficiency in serving clients, but as a prospecting tool.) In an environment where powering adviser lead generation has actually become one of the hottest AdviserTech categories (from Zoe Financial raising $10 million, to Harness Wealth raising $15 million and SmartAsset reaching unicorn $1 billion-plus valuation status with a $110 million capital round driven by the growth of its financial adviser lead-generation solution.

In the AdviserTech context, though, a growing hunger for larger advisory firms to build their own middleware layer of technology, and their own adviser dashboards and client portals — as witnessed other recent announcements like Mercer Advisors adding a new chief technology officer role on its executive team — signals a more fundamental shift in the AdviserTech landscape itself. Historically, independent advisory firms bought software off the shelf, while mega-firms built it themselves. But in the future, the expectation may become that AdviserTech tools are expected to be the engine that powers behind the scenes, but must re-architect for an even more API-based microservices structure to make it easier for independent advisory firms to build their own interfaces and value layer on top?

The T3 conference is the longest-standing and largest trade show event for adviser technology, organized by AdviserTech guru Joel Bruckenstein to showcase the entire landscape of technology solutions for financial advisers. Nominally, the T3 conference is an opportunity for advisers to walk the exhibit hall, shop for their needs, and see the latest and greatest. In practice, the T3 conference has also become a gathering place for leaders of AdviserTech firms themselves, spawning new integrations, partnerships and even the occasional merger or acquisition that initiated from a chance meeting at T3.

The caveat, though, is that AdviserTech firms have tended to send their business leaders — CEOs, chief revenue or growth officers, and perhaps the CTO — but not the actual developers, even though they too can benefit from networking and deeper relationships with other developers (with whom they will someday be building integrations anyway!?). So in an attempt to deepen the AdviserTech developer community, T3 has announced a partnership with INVENT.us (which provides consulting and custom development work for FinServ enterprises transitioning to the cloud) to launch a new WealthTech DevCon, a two-day developer conference that will run concurrently with the broader T3 Advisor Conference.

In practice, the primary focus of the new INVENT WealthTech DevCon is to help developers come together to build in the INVENT.us ecosystem — which uses a cloud-native approach to its development work — with content focusing on microservices architecture, building on Kubernetes, leveraging big data and data lakes, and creating workflows across microservices applications. Accordingly, in addition to an agenda of developer sessions themselves, the event will feature an INVENT Developers Challenge, where developers have a hackathon-style opportunity to build new applications on-site, which are then pitched to industry celebrity judges, and the winner is announced and presented to the entire T3 audience in a subsequent general session at the conference.

From a broader perspective, though, the significance of the new WealthTech DevCon is that — akin to the Orion Fuse event, which first brought this approach of assembling AdviserTech developers for a hackathon to the WealthTech industry several years ago — it creates real opportunities for the developer community to deepen its own relationships, which helps to attract and keep developer talent in the industry, as well as the potential to help improve overall consistency in everything from development approaches to API and data standards, as developers who spend time together connecting with and learning from one another maintain better communication channels across companies in the months and years that follow.

For AdviserTech firms interested in sending their senior developers and architects, registration for the WealthTech DevCon is available directly on the INVENT website, at a nominal cost of just $500 for the two-day event.

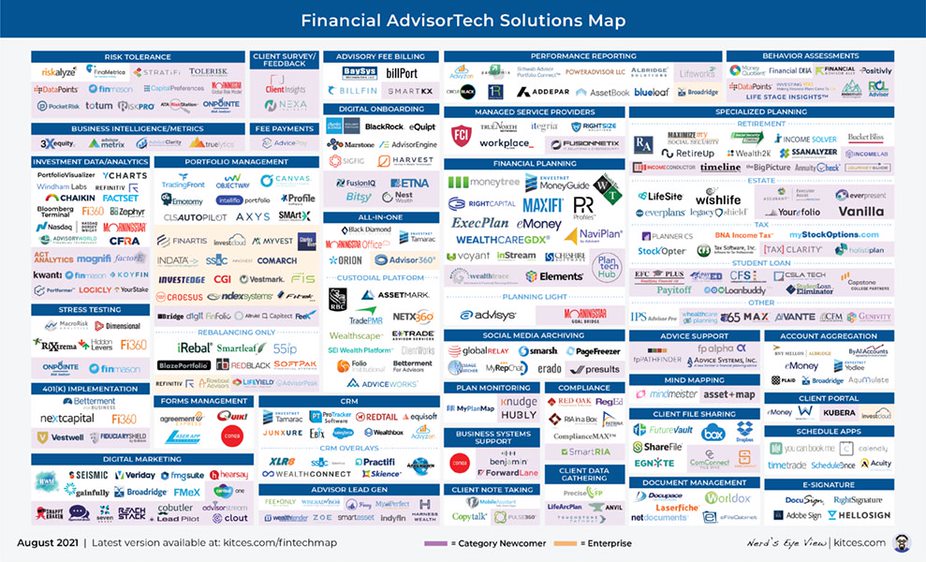

In the meantime, we’ve updated the latest version of our Financial AdviserTech Solutions Map with several new companies, including highlights of the “Category Newcomers” in each area to highlight new FinTech innovation!

So what do you think? Is direct indexing the future? Will Vanguard putting its heft behind it make it so? How much appetite will there be among financial advisers for more risk-hedged investment vehicles on the Simon marketplace? Will adviser review sites gain traction with solutions like Finance Friends, or will consumers prefer more direct “we figure it out for you” matchmaking solutions like Harness Wealth? And what would it take for cryptocurrency to actually start gaining real traction with financial advisers?

Michael Kitces is the head of planning strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’sEye View. You can follow him on Twitter at @MichaelKitces.

You can connect with Kyle Van Pelt via LinkedIn or follow him on Twitter at @KyleVanPelt.

Only 7% of U.S. parents are "very confident" they understand how the Trump accounts work, says Omni Calculator

One transfer alone came to $5.6m, and the receiver says none of it was real profit.

Investors chose which factory to fund - the SEC says the money went elsewhere.

Ameriprise and LPL Financial for the past few years have engaged in a financial advice trade war.

Why advisors at every stage may have more leverage, flexibility, and strategic options than they realize.

Northern Trust’s Ken Lassner shows advisors how to convert volatility into after-tax portfolio gains

Dan Biagini of American Equity says the steady decline of pensions, longer lifespans and a reset in interest rates are rewriting how advisors build retirement income