The August edition of the latest in financial #AdviserTech kicks off with the news that Envestnet has acquired Redi2, a company whose revenue management systems are among the most widely used by broker-dealers. Redi2’s systems facilitate the flow of dollars coming in and being paid out to advisers in all the various increasingly complex ways they can get paid, from upfront commissions via various product types to trails to advisory fees to stand-alone planning fees, along with Redi2’s BillFin solution for independent RIAs doing stand-alone AUM billing.

The deal is well timed to a recent risk alert from the Securities and Exchange Commission about advisers engaging in unwittingly incorrect billing as a result of a lack of strong billing systems and processes. But arguably, it also signals a broader trend, particularly among broker-dealers, toward increasingly complex revenue models with various combinations of third-party products, in-house products, advisory fees through a wide range of SMAs and TAMPs, home office models, and representative-as-portfolio-manager portfolios, and fee-for-service financial planning. This necessitates increasingly sophisticated billing systems to handle the growing complexity, as the industry continues its evolution from product sales to advice fees and the messy middle that comes in the midst of that transition.

The latest highlights also feature a number of other interesting adviser technology announcements, including:

Read the analysis about these announcements in this month's column, and a discussion of more trends in adviser technology, including:

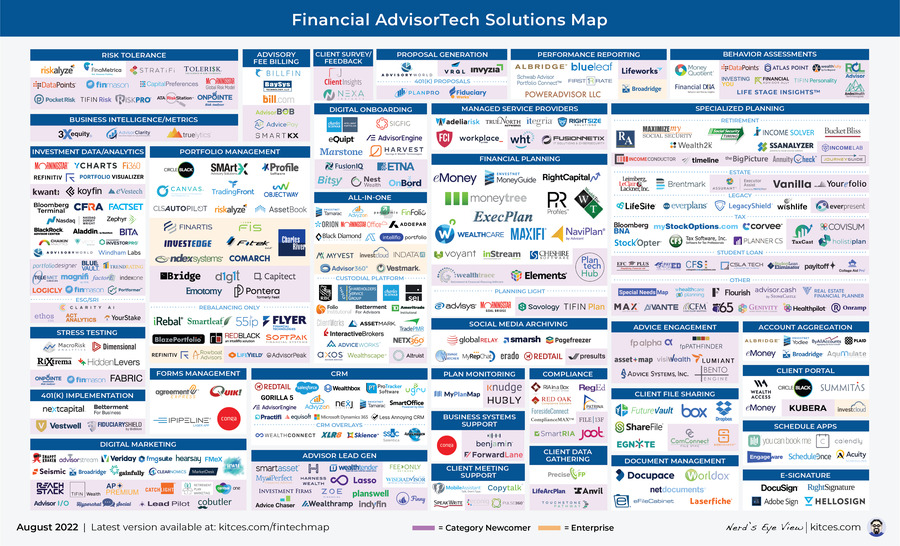

In the meantime, we’ve also made several updates to the beta version of our new Kitces AdviserTech Directory to make it even easier for financial advisers to look through the available adviser technology options to choose what’s right for them.

And be certain to read to the end, where we have provided an update to our popular Financial AdviserTech Solutions Map as well.

AdviserTech companies that want their tech announcements considered for future issues should submit to [email protected].

In the early days of financial-advisers-as-stockbrokers, managing broker compensation was relatively straightforward: Brokers earned commissions for the stock and bond trades they placed directly for their customers, and broker-dealers had one set of standard commission rates typically based on trade size and volume to determine what the compensation would be.

In the 1980s and 1990s, with the rise of discount brokerages like Schwab, and as stock-brokering became increasingly computerized, trading commissions began to fall, and brokerage firms increasingly shifted to the distribution of third-party mutual funds. This allowed for the rise of independent broker-dealers — independent because they were independent of any investment bank to underwrite the securities being sold — that facilitated the distribution of third-party investment products, particularly mutual funds.

By the late 1990s and into the 2000s, though, the sheer breadth of different products that independent broker-dealers offered, from mutual funds to variable annuities and private placements — each of which would have their own commission rates and revenue-sharing agreements, and may have differing payouts to the brokers based on varying grid incentives — led to the rise of revenue management systems. These systems could help track all the different financial arrangements from various providers and the different ways the commissions were split between the broker-dealer home office and its reps, and tie the appropriate commissions to each of the various reps, including in situations where commissions were split across multiple reps.

Over the past decade, though, broker-dealer enterprises have further diversified their revenue streams — not just across the breadth of securities product types, but also with the rise of advisory accounts in the shift to dual B-D/RIA registration after the Merrill Lynch rule was vacated in 2007, and more recently the emergence of subscription and other fee-for-service financial planning models. This has made revenue management exponentially more complex and driven demand for increasingly sophisticated solutions.

In this context, it’s notable that Envestnet announced the acquisition of Redi2, one of the early players and market-share leaders in revenue management systems for adviser enterprises. This includes both Redi2’s core offering – Wealth Manager – which handles the complexities of broker-dealer and TAMP tracking and payouts, along with Revenue Manager, a similar system that supports asset managers, and BillFin which facilitates AUM fee invoicing and billing for RIAs, along with internal tracking of fee splitting and billing compliance.

Strategically, the deal is a good fit for Envestnet’s ever-expanding role in facilitating the back-end of large adviser enterprises — particularly broker-dealers — as Redi2 brings both sizable existing market share in the revenue management category to which Envestnet’s other services can be cross-sold, some upgrades over Envestnet’s existing revenue management systems (e.g., sleeve-level billing for SMAs), and the opportunity for Envestnet to then offer Redi2’s expanded capabilities to its immense base of enterprises.

The related acquisition of Redi2’s BillFin also gives Envestnet a deeper penetration into AUM billing capabilities for stand-alone RIAs, particularly among smaller up-and-coming RIAs, which tend to purchase stand-alone solutions like BillFin until they’re large enough to handle AUM billing within all-in-one platforms like Orion, Black Diamond or Envestnet’s own Tamarac. Envestnet signaled that it sees further opportunities for BillFin to begin facilitating more fee-for-service financial planning payments as well, by integrating it more directly into Envestnet’s MoneyGuide in the coming years. Though given that many larger enterprises offer their advisers multiple planning software tools, it’s not clear how feasible directly-MoneyGuide-based financial planning fee payments will be.

Ultimately, though, the key point is simply that the ongoing growth of advice fees is driving a rising focus on billing systems to manage those fees. From the shift of IBDs into the hybrid model with a broad range of revenue streams where tools like Redi2’s Wealth Manager aim to help, to the ongoing growth of RIAs into larger and more complex enterprises, which necessitates their own revenue management systems. Also, greater scrutiny from the Securities and Exchange Commission about advisory firms not always having cleanly executed billing processes in the first place — per the SEC’s risk alert on investment advisers’ fee calculations last November — is turning what historically was a relatively mundane domain of billing and the associated revenue-sharing/fee payments to advisers into a growth market for financial/operations technology solutions for adviser enterprises.

One of the key lessons that nearly every new financial adviser has to learn the hard way is that there’s a difference between a prospect and a qualified prospect. A prospect is anyone the adviser meets with to discuss potentially doing business with them. A qualified prospect is someone who actually has a need for the services the adviser provides and the financial wherewithal to pay for the adviser’s services. One of the biggest potential losses in productivity for an adviser is spending a lot of time talking to unqualified prospects who can’t or won’t ever actually do business with the adviser.

In the past, qualifying a prospect was often part of the initial meeting process itself. Either at the beginning of the meeting, or perhaps during the process of scheduling the meeting or via a brief intake form, it would be determined whether the prospect had enough assets or other financial wherewithal to work with the adviser, and an understanding would be gained of prospect’s needs to affirm that the adviser was a good fit. This, in itself, was still both a time-consuming process, and a more reactive one, as advisers often still had to initially engage with prospects to determine if they were qualified, and the adviser wouldn’t know if they were qualified or not until the engagement process began.

But in May, a new platform called Catchlight was launched that specifically aims to solve for these challenges by leveraging the plethora of data now available in the digital era to better prequalify prospects in advance.

Born from the Fidelity Labs incubator, Catchlight is not so much a prospecting or lead generation tool, per se, as a lead evaluator that takes in an existing list of potential prospects — e.g., a list of social media contacts, or an existing drip marketing email list — and then cross-references each individual’s identity on available social media platforms and marketing databases. This is in order to try to identify the potential financial complexities they may face — e.g., based on their age, stage of life, neighborhood affluence or company affiliations — and score the prospect to help the adviser understand how worthwhile it would be to pursue that prospect further.

From the adviser perspective, the potential benefits of Catchlight are clear — advisers can reduce the amount of time they spend with nonqualified prospects, or outright have an opportunity to amplify their efforts to reach more (pre)qualified prospects. This can greatly improve the efficiency of the business development process. In turn, Catchlight built its system with an AI layer that can take feedback from advisers on which prospects actually do turn out to be qualified and close as clients (or not), and learn from the feedback to make its qualified-prospect identification process even better. In fact, Catchlight has been in pilot with a handful of firms since the beginning of the year to train its algorithm before release.

Notably, because Catchlight operates as more of a lead evaluator than a lead generator, it won’t necessarily help advisory firms that haven’t figured out how to generate a list of leads or at least a growing list of email or social media contacts in the first place. This is a domain where marketing-tech competitors like SmartAsset and Zoe Financial are better suited. Nor is Catchlight necessarily the drip marketing system to those qualified prospects, where Snappy Kraken, AdvisorStream and ReachStack have grown. Instead, Catchlight would help screen the leads from SmartAsset or Zoe, or the email list in Snappy Kraken, AdvisorStream or ReachStack, or the social media contacts the adviser is building on Twitter, LinkedIn or Facebook, to highlight which leads the adviser should more proactively pursue or screen out altogether.

In the end, Catchlight’s success will be driven first and foremost by the ability of its algorithm to actually spot which are the most qualified leads, and screen out those that truly aren’t qualified, while minimizing the number of false positives or false negatives. Only time will tell whether Catchlight’s algorithm does, or can learn to, execute effectively. But given the incredibly high client acquisition costs of the typical adviser and in particular, how loathe advisers are to spend time with non-qualified prospects, Catchlight seems incredibly well positioned to execute on its opportunity to make the prospecting process efficient. This is especially true for advisory firms trying to scale up that must figure out how to focus their resources on the most qualified leads.

In its earliest days, the turnkey asset management platform, or TAMP, functioned as an alternative to traditional investment products like mutual funds (or funds of funds). Instead of the adviser engaging in the time-consuming process of setting individual stock and bond (or mutual fund) allocations for their clients and then doing the research and due diligence to manage those investments, the adviser could outsource the whole process to a turnkey platform that could handle model design and investment due diligence on a centralized basis. TAMPs then competed in a similar manner to any other investment product on the quality of their investment analysis and research, and their ability to manage client portfolios in a way that would outperform the available alternatives.

However, because many advisers have a wide range of clients that may have differing investment needs and differing investment preferences, it was not uncommon for advisers to choose multiple different TAMPs to work with, selecting the particular TAMP manager’s strategies that aligned to their particular clients. This, unfortunately, deleveraged a lot of the operational efficiencies that TAMPs were supposed to bring, as advisers ended up managing within multiple TAMP systems. This eventually led to the rise of the platform TAMP — a kind of platform-of-platforms solution where advisers could manage all client accounts within one centralized TAMP system, but still have a choice of a range of product TAMPs, and SMAs, within that platform.

Over the years, the two have continued to run largely in parallel. Product TAMPs tend to be more modest, with a focused proprietary investment management offering that they aim to distribute by offering outsourced services to advisers who invest their clients into those strategies; platform TAMPs are mostly technology companies that have access to a wide range of third-party strategies and products that they help distribute.

As platform TAMPs have continued to evolve, though, the irony is that they too have begun to morph back into a form of product TAMP, except the product isn’t the investment offering, it’s the technology offerings that power the platform, with different providers trying to build their own differentiated technology and then find advisers who want to operate within their TAMP tech ecosystem.

It was in this context that several years ago, Adhesion Wealth — which has followed the platform-TAMP-turned-technology-product-TAMP path — was acquired by Vestmark. At the time, Vestmark was and remains one of the larger back-office systems to handle managed accounts for enterprise. Adhesion had built its own proprietary layers of technology value-add on top of the VestmarkONE system, which Vestmark clearly hoped to cross-sell to other advisory firms, particularly other RIAs, where Adhesion had been concentrated up to that point.

Four years later, Vestmark has decided to exit its Adhesion TAMP business and divested the offering to AssetMark, citing what was ultimately nontrivial growth — up from $3.5 billion in 2018 to $9.5 billion today. Though notably, nearly half of that growth may simply be attributable to market growth over the intervening time period. In the end, Adhesion is reporting 180 advisory firms that it works with — up 30 firms from the 150 reported at the original acquisition, of which 17 apparently came in just the first six months of the deal. This implies that growth may have been stalling at Adhesion despite the cross-selling opportunities within Vestmark and ongoing investments into the breadth of models available on its platform.

The end result is that Vestmark appears to be looking to focus back on its core business of being a back-end technology provider to power managed accounts rather than trying to grow the TAMP service layer, which may have been challenging simply because so many of its users already are TAMPs or using other TAMP solutions. Meanwhile, AssetMark — which has been a rapidly growing platform TAMP in its own right — gains the opportunity to bulk up with both additional assets from Adhesion, and additional technology (e.g., Adhesion’s capabilities in direct/personalized indexing that can be rolled out to AssetMark advisers).

From the broader industry perspective, arguably the real takeaway of the Adhesion-Vestmark-AssetMark deal is simply that the ongoing demand for TAMPs to gain scale — including and especially by acquiring other TAMPs — continues unabated, with the buzz that Adhesion didn’t take a valuation hit despite recent market volatility. This is because differentiated technology itself is very hard and costly (and requires scale) to build and maintain. The hyper-competitive nature of the current TAMP marketplace means it’s not an “if you build it, they will come” environment, but instead also requires scale and reach just to distribute the solution and actually attract new advisers to grow.

The financial services industry has long been a slow adopter of new technology trends. In part, that’s simply the reality of a highly regulated industry that tends to be wary of changes that can cause disruptions to key systems. It’s also driven by the fact that the overwhelming majority of advisers operate in at least some form of quasi-independence, either as a stand-alone RIA, or affiliated with a broker-dealer or hybrid RIA, and consequently lack the team and resources to adopt, implement and roll out new technology.

The slow-moving evolution of adviser technology is perhaps most evident in how adviser systems themselves are housed, as the financial services industry severely lagged most others in the transition to the cloud, and a nontrivial number of advisers are still running local desktop- or server-based software rather than fully utilizing available cloud-based systems.

However, the trend to the cloud is now fully underway and accelerating, driven by what is, finally, a near ubiquity of cloud-based solutions for all major adviser software systems. Ultimately, this greatly simplifies the technology demands of advisory firms themselves. After all, when all systems run entirely on the cloud, the in-office/desktop computer simply becomes a kind of dumb terminal whose sole purpose is to provide an access conduit to the adviser’s systems. This alleviates most of the prior burdens related to maintaining local systems and software, and enables advisers to leverage more centralized, remote-based IT solutions.

As a result, one of the rapidly growing sections of the AdviserTech Landscape Map is the category of “Managed IT Services,” which has seen both new launches (e.g., FusionNetix) and existing players focusing more into the adviser channel (e.g., AdeliaRisk), as well as mergers and acquisitions (RIA In A Box acquiring Itegria, True North and RightSize being acquired and merged into Visory). This is a trend that appears likely to accelerate further as the SEC increasingly scrutinizes how securely RIAs are operating their computer systems and recently proposed new cybersecurity requirements. Advisers realize that their existing in-house systems are not actually as secure as modern cloud systems and that they don’t have the in-house expertise to be able to fully manage and maintain a secure environment.

Another new entrant arrived in the managed IT services segment with hybrid-RIA Independent Advisor Alliance announcing a partnership with We Handle Tech: 4 Advisors. Similar to other providers in the space, the partnership will help advisers set up their computers, provide centralized IT support for tech problems and new tech needs and oversee cybersecurity for all the advisers’ systems. It even includes cybersecurity insurance as an overlay to the relationship.

For adviser support platforms like Independent Advisor Alliance, the partnership and its ostensibly IAA-favored pricing forms an interesting differentiator in its technology stack to attract potential advisers to affiliate in an environment where differentiation of adviser networks and platforms has been increasingly difficult, even as it solves for what is arguably a problem that every independent advisory firm ultimately must address.

From the broader industry perspective, though, the real significance of IAA’s partnership with We Handle Tech is part of a broader trend underway toward the outsourcing of IT services by independent advisory firms. Now that the core systems that advisers use are finally all cloud-based enough, and adviser attitudes about the cloud have shifted enough, advisers really can let go of managing their own IT as the burden of cybersecurity increasingly pressures them to do so. Instead, they can refocus themselves more directly on serving clients and growing the business.

One of the most fundamental requirements of a financial adviser's sales process with a prospective client is that, in order to win the business, it’s necessary to convey how the client’s financial situation will be improved by the adviser. This, in practice, is most commonly expressed in the form of an investment proposal, where the adviser reflects back to the prospect their current situation, what the adviser recommends should be changed, and how the prospective client’s situation will be improved as a result.

Over the years, though, the way advisers generate proposals has changed. In a product-based world, proposals were often product illustrations provided by the manufacturer (e.g., the life insurance company’s product illustration tools) that showed the impact of the product purchase on the client’s long-term future (versus the alternative of not buying the product) or a product comparison tool that showed how one product stands up against another (e.g., using Morningstar to show how the adviser’s funds have performed relative to whatever the prospective client already owns). As advisers have increasingly shifted toward advisory accounts, the nature of proposal generation has shifted toward increasingly more comprehensive portfolio analytics that compare the adviser’s proposed portfolio to the prospect’s existing investments on a wide range of metrics (from modern portfolio theory statistics like alpha, to Riskalyze’s Risk-Number-based portfolio comparison).

Notably, though, most advisers ultimately generate their investment proposals not necessarily from sales tools that aim to present a compelling offer to prospects but from investment data/analytics tools that aim to conduct a robust analysis of the investments and then generate some kind of output that can be presented to prospects. However, this means a lot of investment proposals don’t actually do a good job of presenting the information in a way that compels prospects to take action. This means that most advisers don’t have to, or at least aren’t used to, paying separately for investment proposal tools, as they’re typically part of the adviser’s existing investment analytics tools used to build portfolios in the first place (or are provided by a TAMP or home office for advisers that use pre-built or existing models.

In that context, in June CapIntel announced a new $11 million Series A round to scale up its investment proposal generation and supporting investment analytics tool for financial advisers, with a particular focus on not just trying to create a compelling investment proposal for prospects, but providing the ability to do so more quickly and easily so as to save advisers time in the proposal generation process.

For most financial advisers in the U.S., the CapIntel name is likely unfamiliar, as the company has been primarily focused in the Canadian marketplace, where it works with several of the big banks with which a large segment of Canadian advisers are affiliated. In fact, CapIntel’s Series A round is primarily to leverage its success in building out tools for Canadian advisers by funding an expansion of CapIntel into the much larger U.S. marketplace given that there are more than five times the number of CFP professionals in the U.S. as in Canada.

However, the reality is that the U.S. marketplace is also drastically more competitive, in no small part because of the sheer size of the adviser opportunity in the U.S., and the number of technology firms it attracts. And in practice, a number of adviser technology companies from Canada, the U.K. and Australia have tried — without much or any success — to migrate their tools into the U.S., only to find that despite the number of U.S. advisers to potentially work with, it’s arguably even harder to find a beachhead or gain a toehold.

When it comes to investment proposal generation tools, in particular, CapIntel will face an uphill battle in a marketplace where most U.S. advisers are not used to paying separately for proposal generation tools, where advisers have increasingly standardized their portfolios into models (which naturally makes the investment proposal process less time-consuming because the recommendations are virtually always a standard array of models), and where investment data/analytics tools have both long-standing incumbents (e.g., Morningstar, Bloomberg) and rapidly growing competitors (e.g., YCharts and Kwanti) that don’t leave many openings.

In the end, arguably there is room for tools that create a compelling conversation with prospects to stirs them to do something different and take action. This is evidenced by the rapid growth of Riskalyze in particular, which is nominally a risk tolerance tool but has driven its success primarily by functioning as an investment proposal tool that happens to use risk tolerance as its metric for comparison.

Still, though, with the existing landscape littered with the remains of adviser technology companies that tried to expand into the U.S. but failed to know or learn the marketplace enough to find a viable beachhead, the real question is not whether CapIntel can make an investment proposal tool that all advisers can use, but one that’s compelling enough for at least a segment of advisers to actually make a switch from whatever they’re using today.

INCOME LAB LAUNCHES LIFE HUB AND MONEYTREE ADDS NEW SUMMARY AS ONE-PAGE PLANS GAIN TRACTION

When financial planning first emerged with the original class of CFP certificants in 1973, the reality was that financial planning was used primarily to facilitate the sale of insurance and investment products. Relative to the solely product-centric pitch of most salespeople at the time, financial planning was certainly a more holistic and consultative approach to selling. But in the early decades, the primary role of financial planning was to understand a client’s situation and conduct a needs analysis to demonstrate the gaps because the adviser was paid to sell the insurance or investment product that filled that gap.

As advisers began to charge fees for their financial planning, though, the depth and breadth of the traditional financial plan expanded further. The planning software output became more formal. Advisers sometimes even formally bound their printouts to improve the perceived quality of the output being delivered, and the sheer page count of financial plans exploded. This was largely because advisers wanted to literally do more analysis to demonstrate their value to substantiate the fee being charged (or at least to demonstrate that they’d done the required analysis and that clients could trust what otherwise might be a relatively abbreviated page of recommendations at the end).

Over the past decade, though, the business model has shifted further, advisers are increasingly charging ongoing fees in the form of AUM, or now subscription fees, to provide ongoing financial planning advice. The traditional financial plan only addresses the upfront/initial part of the planning engagement, and not what happens in each of the years that may follow. In the past, advisers occasionally returned to and updated the original financial plan. Yet the reality is that client situations often don’t change that much in the span of just a year or two, such that some update may be necessary but a whole new plan is wasted effort.

To fill the void, in recent years an alternative approach of the one-page financial plan has begun to emerge. In practice, the one-page financial plan, or OPFP, isn’t necessarily used as a substitute for the traditional plan upfront with a client when, even if a one-page plan is presented, it may still be supported by dozens of pages of technical appendix to substantiate the analysis. Instead, the OPFP is more about providing a single-page dashboard for clients and their advisers to monitor and understand their ongoing progress. This led to the rise of stand-alone OPFP templates from advisers like Jeremy Walter’s OPFP and Mike Zung’s Beautiful Plan. as well as new planning software features like RightCapital’s new Snapshot.

The one-page plan/summary appears to be gaining momentum, as MoneyTree financial planning software announced a new one-page summary output for clients, and Income Lab’s retirement planning software similarly introduced a new Life Hub module that is built around providing clients with a one-page dashboard to track their retirement and ongoing distributions. This includes updated details of retirement balances and withdrawals, the sourcing of those withdrawals for tax efficiency, and upcoming planning milestones like starting Social Security or paying off a mortgage.

Notably, at this point the actual substance of one-page financial plans still varies by provider, a combination of the fact that different advisers have different preferences on what to show, different clients need to see different information depending on their financial situation and the focus of their planning needs, such as retirees versus accumulators or business owners versus employees, and a simple lack of consensus about the best practices in presenting such information in the first place.

Nonetheless, the growing momentum of planning tools rolling out one-page financial plans — not necessarily to replace the upfront financial plan, but to support the ongoing planning engagement of monitoring client progress and helping to keep track of open recommendations and action items — signals the extent to which advisory firms are increasingly looking to shift their own valuation proposition from just the upfront planning process to demonstrating ongoing value to retain ongoing financial planning relationships. Expect to see more solutions and iterations in this direction from other providers in the coming years.

In the meantime, we’ve rolled out a beta version of our new AdviserTech Directory, along with making updates to the latest version of our Financial AdviserTech Solutions Map with several new companies including highlights of the Category Newcomers in each area to highlight new fintech innovation.

So what do you think? Does Catchlight sound like something that would be useful to scan your prospect list to better qualify the leads? Do you think there’s a gap and a need for more and better investment proposal generation tools? Would you like to see more one-page financial plan summary tools to use with ongoing clients?

Michael Kitces is the head of planning strategy at Buckingham Strategic Partners, co-founder of the XY Planning Network, AdvicePay and fpPathfinder, and publisher of the continuing education blog for financial planners, Nerd’sEye View. You can follow him on Twitter @MichaelKitces.

Kyle Van Pelt is the executive vice president of sales at Skience. You can connect with Kyle Van Pelt via LinkedIn or follow him on Twitter at @KyleVanPelt.

Surveys show continued misconceptions and pessimism about the program, as well as bipartisan support for reforms to sustain it into the future.

With doors being opened through new legislation and executive orders, guiding clients with their best interests in mind has never been more critical.

Meanwhile, Stephens lures a JPMorgan advisor in Louisiana, while Wells Fargo adds two wirehouse veterans from RBC.

Large institutions are airing concerns that everyday investors will cut into their fee-bargaining power and stakeholder status, among other worries.

Fights over compensation are a common area of hostility between wealth management firms and their employees, including financial advisors.

Orion's Tom Wilson on delivering coordinated, high-touch service in a world where returns alone no longer set you apart.

Barely a decade old, registered index-linked annuities have quickly surged in popularity, thanks to their unique blend of protection and growth potential—an appealing option for investors looking to chart a steadier course through today's choppy market waters, says Myles Lambert, Brighthouse Financial.