Broker comp puts pressure on wirehouse profit margins

Even as firms trim non-compensation expenses, profit margins stay below stated goals.

Executives at the four largest brokerage houses have set their sights on higher profit margins. But even as they trim expenses, streamline branch offices and reduce back office staff, they’re struggling with compensation costs for brokers.

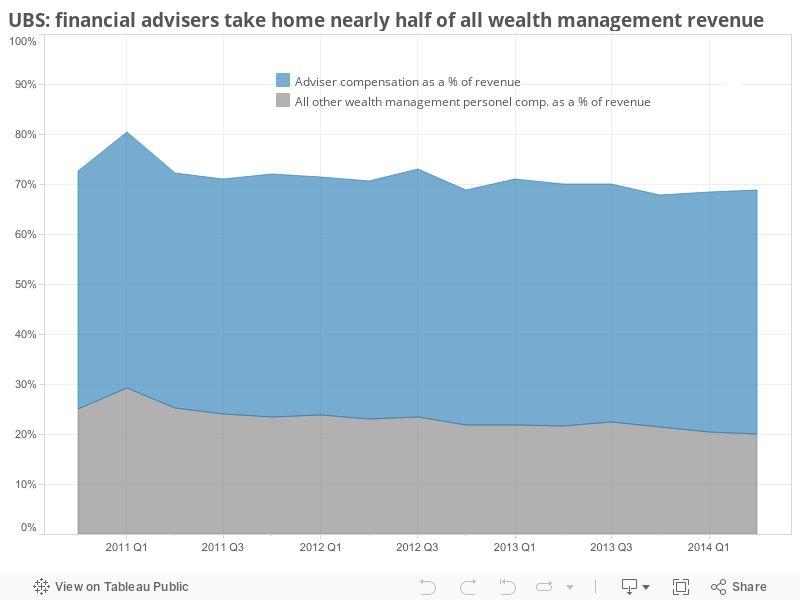

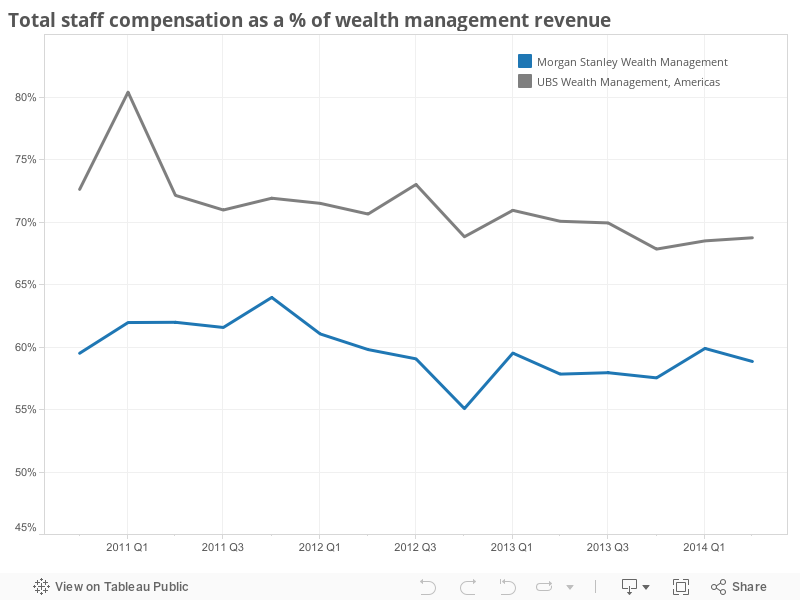

At Morgan Stanley Wealth Management, for example, compensation and benefits for all employees account for as much as 60% of revenue. At UBS Wealth Management Americas, which breaks out compensation specifically for their advisers, it is even higher. The firm has spent an average of around 70% of revenue on its financial advisers since 2011, according to SEC filings.

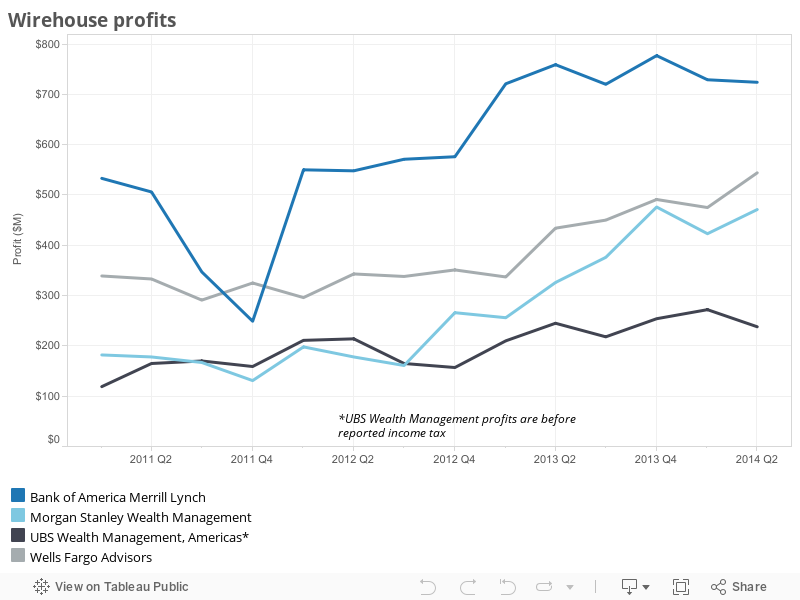

The other two wirehouses — Merrill Lynch Wealth Management and Wells Fargo Advisors — do not provide a comparable number in their quarterly earnings.

Even as non-compensation expenses at Morgan Stanley fell 9% in the second quarter as compared to last year, compensation expenses rose by 7% over the same period.

As a caveat, compensation statistics are based on quarterly reports and may include departments outside of wealth management that may skew results. Inconsistent definitions of revenue, including whether cash balance revenues are booked at the division or recognized at the bank, can also make compensation trends difficult to track or compare across the industry, according to Andy Tasnady, whose firm, Tasnady & Associates, consults with brokerage firms on compensation plans.

Morgan Stanley’s chief executive, James Gorman, said earlier this year that he’s focused on trying to get the compensation ratio closer to 55%, which is still well above the firm-wide compensation ratio of 49% and farther above the compensation ratio of 42% in the investment management unit.

The first issue is that brokers receive most of their pay according to a grid-based formula, which could provide the broker with 30% to 50% of revenue depending on their total haul for the year. That means that as revenue rises, so do compensation costs.

“Personnel expenses increased by $46 million to $1.303 [billion] mainly due to higher financial adviser compensation corresponding with higher compensable revenue,” UBS wrote in its latest earnings report.

If the average adviser at UBS, for example, brought in $1.07 million last year, it is likely that they are taking home 50% of that. Although that number is skewed by some of the higher producing advisers of the firm’s 7,100 headcount, an average salary of $500,000 is a significant payout.

Firms have tweaked those grids to try and make them more profitable for the firm by raising the amount brokers must produce to stay at their same position on the grid. At the same time, they are making compensation more focused on bonuses for certain behaviors, such as bringing in more fee-based business.

But it’s largely been a “cat and mouse game,” according to how one former wirehouse executive described it. Those measures still haven’t done much to lower costs, as average production at the firms continues to rise and more advisers find themselves at higher grid rates or qualifying for those bonuses.

As a result, adviser compensation hasn’t really changed much over the past several years, despite executives’ efforts to improve margins. Aside from some fluctuation, it’s only a few percentage points lower than where it was at the beginning of 2011 for both Morgan Stanley and UBS.

Mr. Gorman has said that one of the solutions is non-compensable revenue, such as banking products, which do not pay out according to the grid.

The other issue that’s propping up costs are the recruiting bonuses, which executives have struggled to bring in line. Competition has pushed recruitment deals up year after year. A signing bonus that was 30% of trailing-12 production tied to a three-year note has become a bonus of 300% of trailing-12 production tied to a nine-year note.

Firms have continued to tinker with that as well, pushing deals out to 12 years or longer for the larger offers, but those loans continue to account for a substantial portion of expenses. UBS spent $184 million on such loans in the second quarter, or just under 10% of revenue, according to their earnings report. The firm has almost $3 billion in outstanding recruiting loans to financial advisers.

Both Bob McCann, CEO of UBS Wealth Management Americas, and Mr. Gorman are expecting those deals to fall as the dust settles from the consolidation during the financial crisis and brokers are left with fewer large firms to move to.

“Long-term, strategically, in an oligopoly structure you would expect there would be less movement of financial advisers between firms,” Mr. Gorman said in a discussion of second quarter earnings. “That doesn’t translate yet into the financials. But over the long-term we think it will.”

But no firm wants to be the first to lower either their compensation or their deals given the threat of departures.

With Finra’s plan to have brokers disclose those recruiting bonuses now shelved indefinitely and more advisers retiring without an equal number of younger brokers coming into the industry, there is no sign of advisers losing the ability to demand their high price.

Learn more about reprints and licensing for this article.