UBS Wealth embraces exotic strategies to battle market headwinds

A pedestrian shelters under an umbrella while passing a UBS Group AG bank branch in Zurich, Switzerland, on Monday, Jan. 22, 2018. A UBS loan backed by shares of Steinhoff International Holdings NV was to blame for the majority of the Swiss bank's 79 million francs ($82 million) in credit losses in the fourth quarter, a person with knowledge of the matter said. Photographer: Stefan Wermuth/Bloomberg

A pedestrian shelters under an umbrella while passing a UBS Group AG bank branch in Zurich, Switzerland, on Monday, Jan. 22, 2018. A UBS loan backed by shares of Steinhoff International Holdings NV was to blame for the majority of the Swiss bank's 79 million francs ($82 million) in credit losses in the fourth quarter, a person with knowledge of the matter said. Photographer: Stefan Wermuth/Bloomberg

The strategy draws inspiration from fast-money playbook beloved by hedge funds.

The world’s largest private bank is doubling down on exotic strategies to profit from the intensifying meltdown in the synchronized bull market.

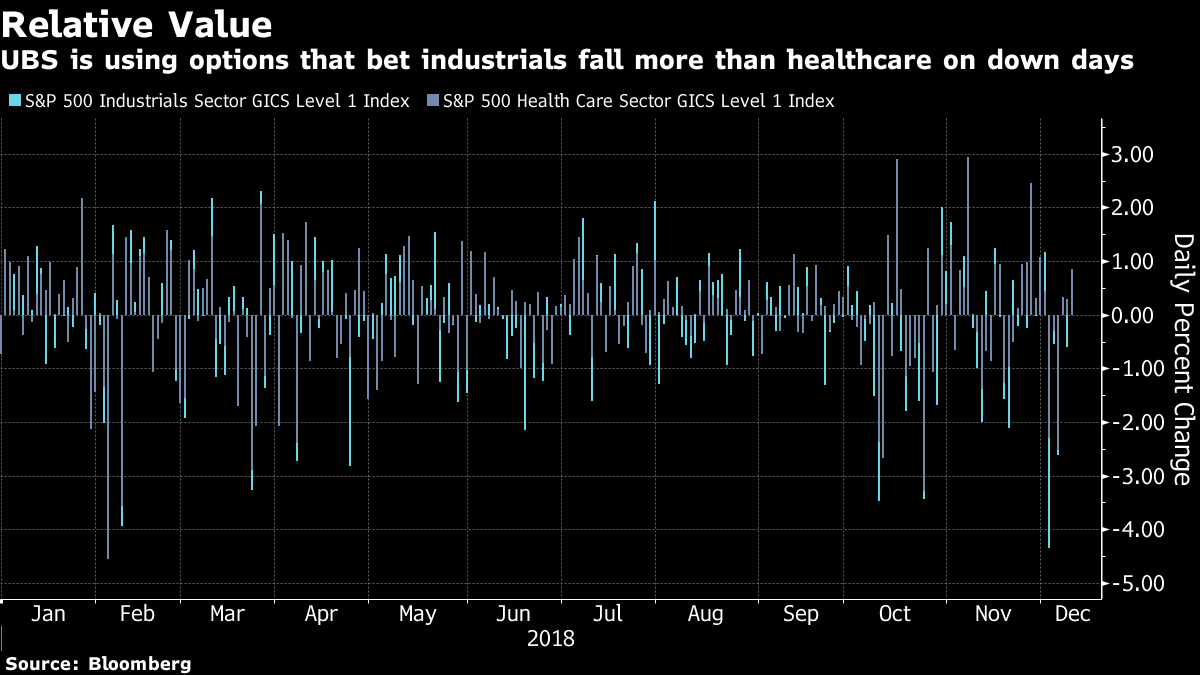

As Wall Street frets another annus horribilis, UBS Global Wealth is embracing a playbook beloved by hedge funds — a slew of options trades that bet, for example, on the continued outperformance of U.S. health-care stocks versus industrials when tensions in commerce sink equities.

The $2.4 trillion money manager’s skeleton key to unlock ever-more complex and fitful markets also links the yield curve to the fate of stocks, and the latter with currency moves.

It’s one solution to the investing conundrum facing its ultra-wealthy clients: How to navigate a multispeed world in which the global expansion looks long in the tooth and liquidity is tightening. As bearish forces grip assets unevenly, the strategy draws inspiration from fast-money investors who buy and sell related securities to profit from price distortions, or relative-value trades.

(More: Market volatility brings alternative investments back into focus)

“As the cycle ages, volatility tends to rise, and it rises because policy support starts to become a headwind in different countries and at different times,” said Vinay Pande, head of trading strategies at UBS Global Wealth Management’s Chief Investment Office. “Those are the reasons you have bigger relative swings across markets.”

One hot strategy is to bet on stock performance in a shifting bond landscape. Though the relationship between the two is debated, Mr. Pande likes options that link a steepening yield curve to falling share prices.

“Owning options on the yield curve steepening out is the cheapest it’s ever been,” said Mr. Pande. “And you can cheapen that considerably if you make it conditional on the equity market performing poorly.”

In Lockstep

Another stocks-rates trade involves buying low-cost call options on the S&P 500 Index conditional on the 10-year Treasury yield remaining range-bound. The theory is that it’s unwise to go long risk assets sensitive to the discount rate like equities if the benchmark note makes a big move.

Hedge funds pursuing the relative-value style are among the top performers in a torrid year, beating most peers that run directional strategies, according to data from Eurekahedge Pte.

“Our view is that, on balance, overweight equity exposure, combined with relative value trades, and portfolio hedges, is the right positioning for the start of 2019,” Mark Haefele, chief investment officer at UBS Global Wealth Management, wrote in an outlook for next year.

Unigestion SA also reckons that 2019 is the year of entrenched divergence. “We expect the opportunity set to change next year, from being directional to more cross markets/relative value oriented,” the $25 billion investment manager wrote in a recent note.

Euro Woes

Smart-money traders are sniffing opportunities as vanilla correlations crater.

In Europe, the weakness of the single currency is failing to give equities dominated by export-orientated multinationals a lucky break as investors flee a region riddled with political risk and easing profit expansion.

“Generally, if the euro would rally, these companies would suffer — but in the environment we’re in, that is trumped by idiosyncratic drivers,” said Mr. Pande.

(More: Advisers tell clients market volatility is the new normal)

He favors bullish call options on European shares conditional on a small strengthening in the euro. The strategy is looking decidedly cheap right now as the contract’s price is capped by the historic relationship these two assets have enjoyed.

Risky Business

While Credit Suisse Group AG also extols the virtues of multi-asset options, the securities are complex and risk backfiring if market doesn’t move as divined.

Still, relative-value trades have an obvious appeal in a choppy landscape where local flare-ups throw correlations off balance, while continued economic expansion challenge bearish bets with conviction.

“The risk we face is not systemic,” said Mr. Pande. “How you address idiosyncratic risk is not the same as how you address systemic risk.”

Learn more about reprints and licensing for this article.