Providing specialized advice to single parents

Advisers can be a critical guide in securing financial health during transition

Single-parent families are on the rise, which means advisers are more likely than ever to have clients with financial needs and planning issues that differ from couples who are raising children together.

Whether it’s from a divorce settlement or an insurance payout from the death of a spouse, single-parent families often start out with a pot of cash to be invested in ways that balance what may be limited future earnings potential of the single parent and the high costs of raising children.

Housing costs and future housing plans are something financial adviser Steve Stanganelli discusses first with his single-parent clients.

“I try to get a handle on where they live and why they want to live there and how much it costs,” said Mr. Stanganelli, principal of Clear View Wealth Advisors. “Typically one spouse wants to keep the family home and the kids, but it just doesn’t work; it becomes the biggest financial concern.”

Mr. Stanganelli said he’s seen many divorce cases where one spouse is given the equity in the home while the other may be allocated a pool of retirement assets that are worth the same on paper. But down the road, the person who owns the home “always ends up poorer,” he said.

Marilyn Timbers, a financial adviser with ING Financial Partners, said financial advisers can have an especially significant impact working with a single parent.

“A single parent is only relying on themselves and they are torn on how to prioritize their money,” she said. “They often prioritize their children’s needs over their own retirement, and retirement savings is especially important for someone single who won’t have a spouse’s retirement sources available.”

Single parents usually feel less secure about money, regardless of how much they have, Ms. Timbers said. Showing them where funds are coming from to cover different expenses can increase their security and really empower them, she said.

Honorée Corder, a personal coach and author of “The Successful Single Mom,” said single moms need a professional in their lives with an eye on their money to help them make investment choices.

“A woman getting $1 million in cash and child support for a number of years who hasn’t worked during 25 years of marriage isn’t going to be able to live as well as she did married to a surgeon,” Ms. Corder said. “She has to have someone to consult with about how much of a house or car she can afford to buy and how to protect that lump sum.”

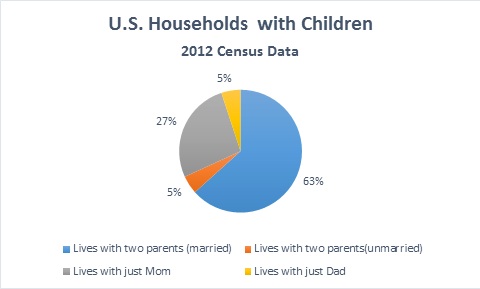

In fact, on average, the nation’s approximately 14 million single-parent households are more financially strapped than those with two parents, according to U.S. Census data. Most also are still headed by moms — about 83% of single-parent households — Census data in 2012 found.

Insurance is another focus of planning for single-parent homes. It includes making sure there’s life insurance for the parent in charge, as well as for anyone who may be paying child support or alimony over the period it is owed, Mr. Stanganelli said.

He also might suggest a single parent work with a job coach or seek other professional development that could help increase their salary if cost-cutting measures haven’t been enough to put the single parent on a successful retirement savings path.

Learn more about reprints and licensing for this article.