The most tax-efficient way to own gold

Pile of pure gold bullion view from above and lots of pure gold bullion

Pile of pure gold bullion view from above and lots of pure gold bullion

Taxes on gold can be complicated and costly, but there are tax-efficient ways to participate in the gold market. Find out how in this article

Updated January 9, 2024

Gold is often viewed as an attractive investment option. It presents investors with a reliable way of protecting wealth, maintaining purchasing power, and diversifying their portfolios. But owning physical gold and other precious metals has tax implications.

In this article, Investment News delves deeper into how tax on gold works and why an industry expert describes the implications to be “not all that glittery.” We will also discuss what he sees as the most tax-efficient ways to own gold.

Financial advisors can share this piece with their clients to help educate them on the tax implications of investing in gold.

How does tax on gold investments work?

For tax purposes, the Internal Revenue Service (IRS) classifies physical investments in precious metals – which include gold, silver, palladium, platinum, and titanium – as collectibles. This means that such investments are subject to capital gains tax.

Gains on collectibles held for up to one year are taxed as ordinary income. This is like how taxes on short-term capital gains are treated. Gains on collectibles held for over a year, while also taxed as ordinary income, are subject to a capital gains tax equal to an investor’s marginal tax rate. The maximum collectibles tax rate is 28%.

This maximum tax rate is higher than the 15% long-term capital gains rate that applies to most assets and taxpayers. That also means that those in the 33%, 35%, and 39.6% tax brackets only must pay 28% on their physical precious metals investments.

“The truth is that in terms of taxes, gold isn’t all that glittery,” the late tax expert Robert N. Gordon told Investment News in a 2010 interview. Gordon was the founder and former president of New York-based wealth management firm Twenty-First Securities.

“Gold is a collectible when it is held in the form of coins or bullion,” he explained. “As a result, the tax treatment of gains and losses on physical-gold investments is different from the tax treatment of investments in stocks, bonds, and other paper assets.”

According to Gordon, long-term capital gains on gold aren’t taxed as favorably as the long-term profits on stock transactions.

“Long-term gains on gold are taxed at 28%, which is almost double the 15% tax rate afforded similar gains in stocks and bonds,” he noted. “Short-term gold profits are taxed at an investor’s ordinary income rate, which is similar to the way short-term profits on mutual funds and stocks are taxed.

“Because of the tax treatment, it is no wonder that investors are asking about the best ways to invest in gold and speculate on its price direction.”

What are the most tax-efficient ways to own gold?

Gordon highlighted three tax-efficient ways to invest in physical gold:

1. Gold futures contracts

One way for investors to participate in the gold market is through futures contracts. These involve buying or selling gold at a predetermined date and price. Gold futures give investors financial leverage by boosting potential returns and carrying additional risks.

“Gold futures contracts, like all futures contracts and index options, come under the provisions of Section 1256 of the Internal Revenue Code,” Gordon explained. “All Section 1256 profits are taxed as being 60% long-term gains and 40% short-term gains.

“This is a trade-off because unrealized profits or losses are marked-to-market at the investor’s year-end.”

Gordon added that this blend could create an effective 23% tax rate calculated as:

[(60% of the gain x 15%) + (40% of the gain x 35%)]

This 23% rate is preferable to either short-term or long-term gains on gold itself.

However, Gordon pointed out that gold futures contracts can be complicated. That’s why a deep understanding of the volatility and complexities of the gold market is essential when entering such agreements.

“Because many investors and financial advisers aren’t comfortable with futures, they may do well by looking into listed options in gold-related investments,” he said.

2. Gold ETFs

Gold ETFs have become a popular option among investors. These commodity funds trade like stocks. The exchange-traded funds consist of gold-backed assets, so investors don’t own physical gold. Instead, they own small quantities of gold-backed assets, allowing them to diversify their portfolios.

“One increasingly popular gold investment is SPDR Gold Shares (GLD), an exchange-traded fund from State Street Global Advisors,” Gordon said.

“One would think that the tax treatment of gains and losses in GLD shares would be similar to that of other ETFs. Unfortunately, that isn’t the case, because GLD is structured as a grantor trust, not a mutual fund.

“A grantor trust is ignored for tax purposes so that the investor is treated as owning a pro-rata share of the underlying holdings, not the entity. If GLD were a mutual fund, it would be taxed ‘normally,’ but because it is a grantor trust, its long-term gains are taxed as a collectibles gain – at the 28% rate.”

According to Gordon, long-term gains would be better than short-term gains for most investors.

“Oddly, though, investors in the 25%-or-lower tax bracket are better off with a short-term gain taxed at their ordinary income tax rate of 25% rather than having a long-term gain taxed at 28%,” he noted.

“A listed option on the GLD ETF, for example, would offer the same maximum 23% tax rate as a gold future. Exchange-traded options on GLD are treated as non-equity options and therefore are Section 1256 contracts.”

3. Over-the-counter physical gold or gold ETF

Over-the-counter option on either the GLD ETF or the gold itself could have better tax implications, according to Gordon.

“These non-exchange-traded options aren’t available for Section 1256 treatment,” he explained. “It seems that the rules governing long-term gains on collectibles don’t govern the taxation of options on collectibles. If my analysis is correct, OTC gold options are taxed ‘normally.’ This means that if the options are held for more than 12 months, any profit is taxed at just 15%.

“For those unlucky enough to have losses on gold, there is one saving grace – because wash sale rules apply only to securities, and not to collectibles, those with gold losses aren’t bound by the rules. They may sell gold to lock in a loss and buy back a similar quantity, with no tax impact.”

How is tax on gold calculated?

The amount of tax owed on gold investments depends on its cost basis. If the investors purchase gold themselves, the cost basis is equal to the amount they paid. The IRS, however, allows investors to add certain costs to the basis to reduce their future tax liability.

Here’s a sample calculation for 100 ounces of physical gold purchased at $1,330 per ounce by an investor in the 39.6% tax bracket and sold them for $1,500 per ounce two years later.

Investors can use capital losses on other collectibles to offset tax liability. For example, if an investor sells gold at a $500 loss, they can offset this amount and owe only $4,260 on taxes. Investors can also opt to carry over the loss to offset future liability.

In addition, the IRS lays down two special scenarios for calculating the cost basis of gold:

1. Gold given as a gift

If an individual receives the gold as a gift, the cost basis is equal to the market value of the gold on the date it was purchased by the gifter. But if the market value is less than what the gifter paid, then the cost basis will be equal to the market value of the gold on the day the individual receives it.

2. Inherited gold

If the gold is inherited, then the cost basis is equal to its market value on the date of the death of the person who left the inheritance.

These scenarios also apply when calculating the cost basis of silver.

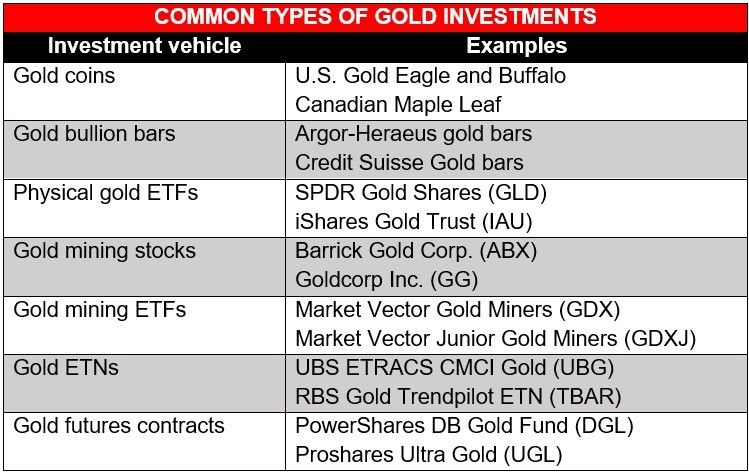

What are the most common types of gold investments?

Gold investments can take on many forms. Here are the most common types:

1. Gold coins and bullion bars

Coins and bullion bars provide investors with a relatively simple and straightforward way to invest in the gold market.

In general, gold bars sell closer to the spot price compared to coins as they are also less costly to produce. Gold coins, on the other hand, are costlier to mint because of their intricate designs. Coins are less costly to store than bullion bars, which often offsets the price difference.

2. Gold ETFs

Gold ETFs are considered a good alternative to purchasing physical gold. ETFs trade like common stock, so buying and selling gold are often convenient and involve low transaction costs.

Another benefit is that investors are not responsible for storing gold, although ETFs charge an annual fee ranging from 0.25% to 0.4% of the spot price.

3. Gold mining stocks and ETFs

These allow gold investments but with limited access to physical gold bullion. Gold mining stock and ETFs typically move in relation to gold prices and are also influenced by production and borrowing costs. Gains from these types of investments are taxed as long-term capital gains if they are held for more than a year.

4. Gold ETNs

Gold exchange-traded notes act as debt securities where the rate of return is linked to an underlying gold index. In ETNs, investors don’t physically own gold. However, at maturity, they yield returns that are equal to those in gold investments.

Because ETNs are secured only by the issuer, if the issuer goes bankrupt, the investors may receive little to no return for their investment. ETNs also trade like shares of stocks and benefit from long-term capital gains.

5. Gold futures contracts

Gold futures contracts involve buying or selling gold at a predetermined date and price. These enable investors to leverage swings in gold prices, which can lead to profits or losses.

For tax purposes, any gains or losses on a futures contract is treated as 60% long-term capital gains and 40% short-term capital gains. This paves the way for a lower effective tax rate compared to the ordinary income rate but still higher than the long-term capital gains rate.

Here’s a summary of the common types of gold investments:

The tax rules for investing in gold can be complicated. That’s why a deep understanding of the different taxation laws and regulations is crucial to maximize profits. Our Tax Planning Section can help you sift through the noise. Here, you can access views and advice from renowned industry experts. Be sure to bookmark this page to keep abreast of the latest updates on investments and taxation.

Learn more about reprints and licensing for this article.