The latest in financial adviser fintech — December 2019

This month's edition kicks off with the blockbuster news that Charles Schwab will be acquiring TD Ameritrade in 2020.

Welcome to the December 2019 issue of the Latest News in Financial Adviser #Fintech — where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors and wealth management!

This month’s edition kicks off with the blockbuster news that Charles Schwab will be acquiring TD Ameritrade in 2020, which sets off not only a seismic shift in the competitive landscape for retail brokerage and RIA custodial platforms but also raises substantial questions about the future of advisor FinTech innovation in a world where the majority of such startups in recent years have built first to TDA’s VEO platform as an initial go-to-market strategy… which may or may not remain viable if Schwab folds VEO into its own (much-harder-to-get-onto-the-integration-roadmap) OpenView Gateway platform.

From there, the latest highlights also include a number of other interesting advisor technology announcements, including:

• Newly Proposed Regulations to update SEC advertising rules and permit advisors to steer clients towards third-party review sites could spawn a slew of new Advisor Ratings platforms

• Envestnet’s Tamarac integrates with FIX Flyer as more and more large RIAs look for trading efficiencies in a multi-custodial world

• MaxMyInterest launches a 1.00% APY high-yield checking account (to couple with their even-higher-yielding savings account) for advisory firms to offer their clients

• Goldman announces that it is gearing up a new pricing strategy for United Capital’s FinLife CX technology to support the distribution of Goldman proprietary solutions

Read the analysis about these announcements in this month’s column and a discussion of more trends in advisor technology, including the launch of BidMoni’s FiduciaryShield platform to help advisors support (and prospect for) 401(k) plans, LoanBuddy’s launch of a new advisor dashboard and enterprise pricing as student loan planning as demand begins to rise for student loan planning tools, the launch of a new “AdvisorEpisodes” platform by three former Riskalyzers to provide advisory firms ready-made short videos to share on their social media channels, and JourneyGuide’s launch of a new retirement planning software platform with the novel approach of illustrating, in the planning software itself, whether a particular annuity product actually improves the client’s long-term financial plan (or not)!

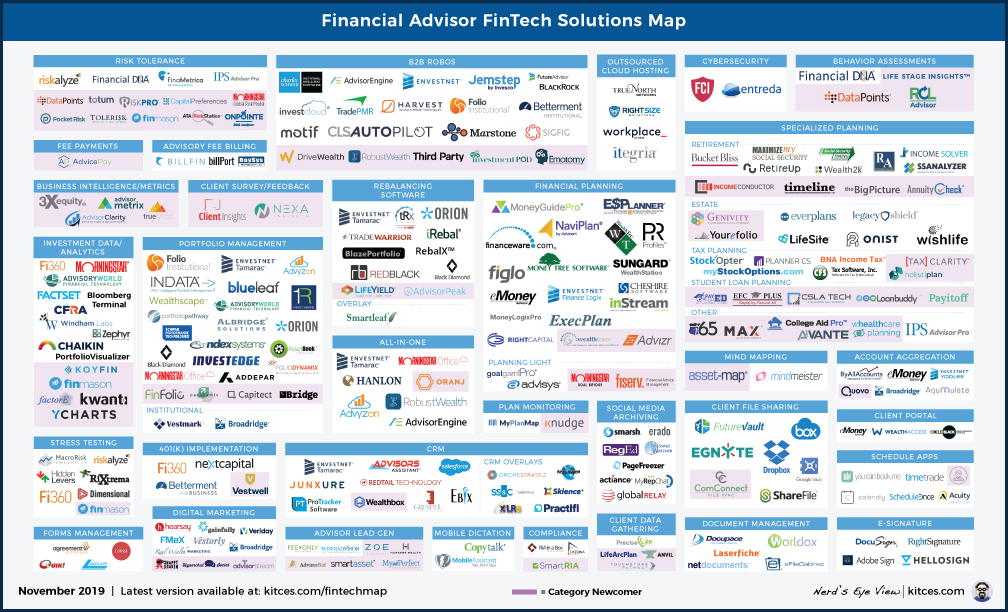

And be certain to read to the end, where we have provided an update to our popular new “Financial Advisor FinTech Solutions Map” as well.

I hope you’re continuing to find this column on financial advisor technology to be helpful. Please share your comments at the end and let me know what you think!

*And for #AdvisorTech companies who want to submit their tech announcements for consideration in future issues, please submit to [email protected]!

Will Charles Schwab Acquiring TD Ameritrade Reduce Advisor FinTech Innovation? The mega news out this month was the announcement that Charles Schwab is acquiring competing discount broker (and 3rd-largest RIA custodian) TD Ameritrade, to form what will become one of the largest financial services companies in the country, dramatically advancing what was already Schwab’s lead as the largest RIA custodian. News of the deal boosted the share price of both companies, as the merger is anticipated to bring even better economies of scale for Schwab in an increasingly competitive and commoditized landscape for brokerage services where scale is essential to compete on price. Yet from the advisor perspective, the news of “Schwabitrade” is being met largely with concern and trepidation, as TD Ameritrade was long a refuge for smaller RIAs that didn’t feel they received good service (or couldn’t even access) Schwab due to required asset minimums, larger RIAs liked the competitive aspect of playing RIA custodians off of each other and the independence that becomes with being multi-custodial and not beholden to any one player, and the consolidation of advisor referral networks will likely reduce access and create fewer larger winners (which increasingly are the firms that are already the largest, where custodians offer access to their advisor referral networks to incentivize large firms to affiliate and keep assets there). But from the Advisor FinTech perspective, the real concern of the Schwabitrade merger is the potential loss of TD Ameritrade’s VEO platform, which thanks to its industry-leading open architecture APIs has been the go-to-market build strategy for the overwhelming majority of recent startups trying to access the RIA market, benefitting both Advisor FinTech startups and TD Ameritrade itself (that enjoyed the most active and rapid iteration of new platform features by attracting such a large host of startups). As while Schwab’s OpenView Gateway has become increasingly open in recent years, it is still far more difficult to get any kind of meaningful integrations onto Schwab’s roadmap, and startups have typically opted for building to TD Ameritrade’s VEO first precisely because they felt ‘shut out’ from Schwab (and Fidelity)’s less accessible integration platforms. Raising the question of whether one of the secondary knock-off effects of Schwab acquiring TDA may be a chilling effect on Advisor FinTech innovation, as even when new startups create compelling new advisor solutions, if they can’t get the product to market efficiently (without TDA’s VEO and being unable to wait out Schwab’s multi-year integration waiting list), the company won’t be viable. Which in turn raises the question of whether there’s an opportunity for a competing RIA custodian to fill the void that Schwabitrade may create and take up the mantle of FinTech innovation leadership by becoming the new truly-open-architecture “Google”-style platform for RIAs, as contrasted to Fidelity’s more “walled garden” Apple-style approach?

New SEC Advertising Rules For RIAs To Spawn Third-Party Advisor Review Sites? This month, the SEC announced for the first time in nearly 60 years that it would be updating the Rule 206(4)-1 limitation that prevents RIAs from using client testimonials in their advertising to prospective clients. Recognizing the modern era of social media and internet websites that consumers routinely rely upon to evaluate potential services providers, the SEC’s new rule will not only permit advisors to use client testimonials in their advertising, but also to cite their scores or ratings from third-party review sites. And perhaps most importantly, the SEC’s newly proposed rule explicitly notes that “statements regarding the investment adviser on a third-party hosted platform… that solicits users to post information, including positive and negative reviews of the adviser, would not fall within the scope of the proposed rule’s definition of ‘advertisement’… unless the adviser took some steps to influence such reviews or posts”. Which is notable because in the past, 2014 guidance from the SEC had suggested that advisors wouldn’t run afoul of the anti-testimonial rule simply because a client independently went to a third-party website (e.g., Yelp) and posted a review of the advisor, but had implied that if the advisor solicited clients to post such reviews, it may constitute a prohibited testimonial (whereas the new rules state more clearly that asking clients to leave reviews isn’t prohibited, and in fact isn’t subject to the advertising rules at all!). Which could prove to be a much-needed breakthrough that stokes the rise of “Advisor Review” sites. Because in the past, third-party advisor review sites have consistently languished and failed, driven heavily by the fact that most advisors don’t have very many clients in the first place (often no more than 100-150 active client relationships), and when only a few percent of customers typically leave a review for any business on a third-party website, the “average” advisor would likely only end out with 1-3 reviews at best… and even that level of review activity would be hard to achieve when the advisor couldn’t solicit and encourage their clients to leave a review. Now, however, advisors can not only encourage clients to leave reviews, but even incorporate such a feedback/review process systematically into their interactions with clients (e.g., encouraging clients after the initial planning process, or after their annual review, to go and leave a review on a third-party website), which makes it possible to have a significantly higher review rate, making it possible for third-party review sites to actually reach the critical mass necessary to become a viable review platform. Of course, sites like Yelp (where some advisors already have clients leaving feedback) have a significant headstart, and it may simply become more common for consumers to check Yelp (or AngiesList, or similar service-provider review sites). Nonetheless, with the SEC proposing relief for advisors to encourage client reviews – at least if/when the currently-Proposed Rule takes effect as an actual rule sometime in 2020 – the regulatory change will likely spark a new wave of Advisor Review sites in the coming years!

Envestnet’s Tamarac Integrates With FIX Flyer As (Large) Independent RIAs Go Increasingly Multi-Custodial. One of the fundamental key functions that all RIA custodians must fulfill is the ability for advisory firms to execute trades on the custodial platform in their clients’ accounts, for which all of the RIA platforms have developed their own trading tools. The caveat, however, is that as independent RIAs accumulated clients and developed increasingly systematized investment processes, the needs of independent RIAs outgrew the capabilities of their platforms, leading to the rise of “rebalancing” or model-management software that determines the appropriate trades and then creates the relevant trade files to upload to custodians to process. And in the case of advisory firms that operate across multiple custodians – which is increasingly common as advisory firms grow larger and develop the infrastructure necessary to be able to support multiple platforms – such third-party portfolio management tools become necessary to be able to centralize trading and portfolio management in a single system that can then allocate trades across those custodians (rather than forcing the firm to separately log into each custodian’s trading system, which in turn raises “Best Execution” concerns for clients whose trades in one custodial system may be executed before other clients on other platforms). Yet the growing adoption of third-party portfolio management systems inevitably leads to a growing desire to make the subsequent trading more efficient, which is now leading to the rise of direct integrations to third-party Order Management Systems (OMS) that can facilitate such trade execution in real time across multiple custodians. Accordingly, this month the Tamarac trading and rebalancing platform announced an integration with Order Management System FIX Flyer, allowing Tamarac users to queue up and then execute trades directly across multiple brokerage platforms, ensuring faster execution and reducing the risk of trade errors, adding to FIX Flyer’s existing integrations to other popular multi-custodial RIA rebalancing solutions, including Orion’s Eclipse, Morningstar’s TRX, and last month’s just-announced Riskalyze’s Autopilot. From the RIA perspective, such FIX Flyer trading integrations gives firms a greater opportunity to both control their trade execution, and be more efficient in doing so across multiple custodians… to the chagrin of RIA custodians, that increasingly want to bind advisors to their particular platforms (and trading systems), but continue to struggle with the trend of (especially larger) RIAs becoming multi-custodial and putting the custodians’ capabilities in direct competition with each other.

Goldman Prepares To Gear Up United Capital’s Finlife CX With New Leadership And New Pricing But To What End? United Capital has been one of the most successful and fast-growing RIA aggregators of the past decade, when a number of advisory platforms emerged – from HighTower to Focus Financial to Fiduciary Network – with the vision of acquiring multiple firms into one larger enterprise in the hopes that the whole would be worth more than the sum of the parts. From the financial engineering perspective, such feats are readily possible because larger enterprises – thanks to both their size and relative stability, and their relative appeal to private equity investors – tend to generate higher valuation multiples than small to mid-sized firms… making it possible for a mass of smaller firms to be purchased for 6X to 9X free cash flow, and then be re-sold as part of a larger enterprise for 12X to 15X EBITDA. The caveat, however, is that a pure “aggregation” of independent advisory firms has little real cohesiveness, and limited operational efficiencies or economies of scale; as a result, ideally, RIA aggregators try to find firms with a consistent approach and who are willing to systematize, which unfortunately isn’t always possible because the pressure to acquire and grow can potentially limit the aggregator’s ability to be selective. In this context, United Capital was/is notable in the category of RIA aggregators, because it took a unique focus on building a single standardized advisor and client experience (built on top of Salesforce), with deep integrations into financial planning and portfolio management software, and its own proprietary client portal. Which in 2016 United Capital decided to license externally to other advisory firms to use as a standalone software solution, dubbed “FinLife”. Unfortunately, though, United Capital struggled to find the ideal monetization model for the advisor platform, variously trying to charge first a basis point fee, and then pivoting in 2018 redubbing the platform “FinLife CX” (for Client Experience) and repricing to a $600-per-client fee instead. Accordingly, when Goldman Sachs acquired United Capital earlier this year, the question emerged of whether or to what extent Goldman was buying the United Capital wealth management business, versus its FinLife CX platform. But now, Goldman has announced a fresh re-launch of FinLife CX, under new (Goldman) leadership, and a new per-advisor (rather than a per-client) pricing structure, and a mandate to broaden FinLife CX’s “accessibility and capabilities, including access to Goldman Sachs products”. In fact, the new FinLife CX relaunch notably includes integration to a new FinLife “MarketPlace”, explained as a “curated offering of products and services allowing advisors to deepen client relationships by extending beyond traditional portfolio management and financial planning”, to initially include GS Select (a securities-based lending offering), and raising the question of whether Goldman will eventually try to roll out Goldman Sachs Asset Management (GSAM) solutions through FinLife CX as well. In other words, while United Capital struggled to monetize FinLife CX by charging basis points or a full-fledged software fee, Goldman Sachs may be repositioning FinLife to instead function as a distribution channel for Goldman products… and reinforcing how FinTech tools are increasingly being positioned not just as a software solution, but an entire distribution channel for financial services products unto itself!

MaxMyInterest Launches High-Yield (1.00% APY) Checking Account For Advisory Firms To Offer Clients. As both large banks and brokerage firms increasingly shift to a business model of earning a substantial spread on cash, a growing number of competitors are offering high-yield savings accounts as a means to attract prospective investors’ idle cash holdings (to both establish new investment relationships, and in the hopes of eventually converting that cash to be invested). Accordingly, 2019 has witnessed both direct-to-consumer platforms like Robinhood, Wealthfront, and Betterment launch high-yield savings solutions, as well as a growing crop of advisor-oriented platforms including early entrant MaxMyInterest and their MaxForAdvisors solution, and more recently Stonecastle’s FICA, Galileo Money+, and Flourish Cash. The caveat, however, is that these high-yield savings solutions are primarily focused on savings accounts – specifically, the excess cash that clients may be holding above and beyond what they use to cover their ongoing monthly spending bills. Which means clients must still keep some outside banking relationship for their traditional “banking” activities – i.e., paycheck (and/or physical check) deposits, and bill paying and check writing. Accordingly, it’s notable that this fall MaxMyInterest has launched a new “MaxChecking” solution (in partnership with online Radius Bank), that will provide advisors the ability to offer clients a high-yield checking account (with a currently-reported 1.00% APY) and “full mobile banking capabilities” (i.e., mobile check deposit, bill pay, etc.). The appeal of a high-yield checking solution – coupled with high-yield savings – is the potential for independent advisors to offer clients a full “cash management” banking solution that would make it feasible for clients to completely consolidate their finances with their advisor and terminate their existing outside banking relationships. For those who don’t actually want to move their checking accounts – or at least, not entirely sever their prior/existing banking relationships – MaxChecking may also be appealing simply as a conduit for outside cash to transfer in to MaxMyInterest’s high-yield savings, and/or to more easily shift money from Max savings to Max checking in the event they need to ‘quickly’ write a check. Overall, though, when advisors typically work with more affluent clients who sometimes carry rather substantial balances in their checking accounts, the ability to provide a 1%-yield checking account is a fairly material solution that would have a non-trivial financial benefit for clients (an opportunity to add value in an era where advisors are increasingly under pressure to validate their fees with any value-adds they can!).

LoanBuddy Rolls Out New Advisor Dashboard And Enterprise Pricing As Student Loan Planning Gains Momentum. Because of the highly specialized nature of our software needs, a significant portion of the financial advisor technology landscape are comprised of the “homegrowns”… where an advisor makes a solution that he/she needs for their own work with clients, then makes it available to other advisors, and ends out running a software company “on the side” along with their advisory firm. The latest addition in this homegrown category is LoanBuddy, developed by financial planner Ryan Inman (of Physician Wealth Services), who does extensive student loan planning for his own clientele (a common planning issue for young physicians), and has turned LoanBuddy into a student loan planning solution for other advisors to assist in everything from pulling in NSLDS (National Student Loan Data System) information on the client’s existing student loans, comparing the various income-based repayment programs to whether the client may qualify for Public Student Loan Forgiveness (PSLF), and helping to determine when it may be better to consolidate or even privately refinance student loans. And with growing advisor interest in offering student loan planning solutions, LoanBuddy announced recently the rollout of a new advisor dashboard, a new Enterprise pricing structure for firms with 10+ advisors, and a single-sign-on integration with MoneyGuidePro. From a planning perspective, the highly specialized and technical nature of student loan rules, along with the high stakes (substantial debt!) and high income potential (at least for those who obtained student loans to enter professional services careers like law or medicine), makes student loan planning both an appealing service to offer clients, and one that is highly conducive to software to support the associated analysis. The caveat, however, is that advisors who do student loan planning will likely often still do it as part of a broader more holistic financial plan, raising concerns about whether – similar to Social Security planning – such student loan planning software is better in a standalone tool, or to ultimately be fully integrated into financial planning software. For the time being, though, with student loan planning software remaining an open gap in today’s financial planning software, solutions like LoanBuddy appear well positioned to either develop deeper integrations into existing financial planning software (to reduce double-data-entry and make it easier to integrate student loan planning with the rest of the financial plan), or alternatively may end out being an appealing acquisition target to whichever financial planning software recognizes the emerging opportunity first?

Financial Planning Software Shifts Towards Next Generation PFM As eMoney Launches Project Avocado And MoneyGuide Integrates With Yodlee FinApps. While “client portals” have become increasingly ubiquitous in recent years, attached to most portfolio performance reporting and financial planning software tools, the caveat is that in reality, advisory firms struggle to gain client adoption (with often no more than about 1/3rd of clients who log in even infrequently). After all, as financial advisors, we often try to reduce the client’s focus on volatility by discouraging them from looking too often at their portfolio (which means we don’t actually want them to log into their portal to look at their investment results), and financial planning progress towards multi-decade goals is in practice so slow that logging in regularly doesn’t show much progress anyway (or worse, makes a market pullback look like clients are “failing” their goals). Yet PFM (Personal Financial Management) portals like Mint.com and Personal Capital have stated that their typical users log in as much as one or two dozen times per month. The key difference: PFM solutions focus primarily on household cash flow and net worth (which can and do change and progress more regularly) rather than investment performance and progress towards (ultra-long-term) goals. And those platforms increasingly not only provide aggregated data about where household spending is going (and progress towards accumulating net worth), but provide recommendations and action items to help suggest additional steps to take for further improvement. Unfortunately, though, client portals that financial advisors have available to offer to clients have been slow to shift the focus to a more PFM-centric (and more client-relevant) approach. But now, the shift finally appears to be underway, with eMoney Advisor announcing its new “Project Avocado” (yes, it really is an Avocado-Toast-for-Millennials reference), a new PFM solution specifically designed to facilitate tracking of cash flow and budgeting (and provide clients suggestions for improvement), and MoneyGuide announcing a series of new “Blocks” modules leveraging Yodlee FinApps that will analyze cash flow and its sustainability and track the client’s net worth. On the one hand, the good news of these long-overdue, next-generation PFM solutions for advisors – that move beyond portfolio performance reporting and goal tracking – is the potential to deepen engagement with clients in areas more meaningful to them on a daily/weekly/monthly basis. On the other hand, when many financial advisors aren’t actually accustomed to providing advice for clients around their household spending and cash flow behaviors, opening “Pandora’s Box” of spending conversations may challenge some advisory firms to develop new areas of expertise (albeit in what will likely become a new area of value-add in the long run, especially when working with younger clientele!).

Can BidMoni’s FiduciaryShield Become The Riskalyze Of 401(k) Plan Management? Software to assess a client’s risk tolerance had already been around for nearly two decades when Riskalyze first appeared in 2011… yet within just 5 years, it had become the dominant player in the category (and has continued to grow since then). The fundamental difference between Riskalyze and its incumbent competitors, though, wasn’t merely about the tool for assessing risk tolerance itself, but the fact that other risk tolerance software was built primarily to assess risk tolerance after the client became a client, with a focus on doing so efficiently and compliantly… while Riskalyze was built to facilitate the prospecting process with a potential client, leveraging the risk tolerance conversation to first and foremost show how the prospect’s existing portfolio was a poor fit, and how the advisor’s solution could improve upon the result. In other words, while most risk tolerance software was about compliance and operational efficiency, Riskalyze was first and foremost about prospecting and generating new clients (and then subsequently documenting their risk tolerance as necessary), and Riskalyze’s connection to bringing in new revenue made it feasible to outgrow incumbents despite also charging more-than-double the price of their competitors. In this context, it’s notable that newcomer BidMoni has launched a new “FiduciaryShield” solution to help advisors do more 401(k) plan business, with a similar focus on helping advisors help plan sponsors to fulfill their ERISA fiduciary duties… but framed in a solution that is built first and foremost to aid advisors in generating new business opportunities. Because the core differentiator of FiduciaryShield is a “401(k) Prospecting” tool, that allows advisors to enter their zip code, and then search and filter through local 401(k) plans (ostensibly based on their Form 5500 filings), identify plans that may have some potential fiduciary issues (with respect to plan documents, available investments, plan costs, etc.), and then submit an invitation to the plan sponsor’s company to participate in an RFP process, where FiduciaryShield then sends the relevant plan information to third-party plan administrators and recordkeepers to submit their bids for the plan’s business. Behind the scenes, FiduciaryShield will naturally capture the relevant documentation necessary to substantiate the decisions of the plan sponsors – and ‘check the ERISA fiduciary boxes’ – but arguably it’s FiduciaryShield’s streamlining of the prospecting process to find potential plans to compete for, and facilitating the RFP process, that really differentiates the platform from mere ‘401(k) fiduciary compliance software’. Which is important because in the end, if FiduciaryShield becomes the best at not just supporting ERISA fiduciary compliance but helping advisors to generate more business through the ERISA fiduciary compliance process, it has the potential to disrupt its category much the same way that Riskalyze did with risk tolerance software!

Schwab Launches “Free” Envestnet-Style Alternatives Platform In Partnership With iCapital. With Charles Schwab’s recent announcement last month to drop their trading commissions to zero, the rising question has been whether RIA custodians will be forced to either cut service given the foregone revenue, or come up with a new source of revenue to make up for it. Yet the reality is that trading commissions have long been an ever-reducing portion of the revenue for brokerage firms, which already have spent the better part of 20 years shifting to alternative sources of revenue, including proprietary products (e.g., Schwab ETFs, and Schwab’s affiliated-bank cash sweep), and getting paid to help distribute investments to the investors (and advisors) on its platform. After all, it was Schwab that pioneered the “OneSource” mutual fund marketplace in the 1990s, that offered “free” mutual fund trades… to be made up by receiving 12b-1 and sub-TA fees paid directly from the mutual fund providers to get onto the “free” platform (and extended to the emergence of pay-to-play no-transaction-fee ETF platforms over the past decade). And so as trading commissions vanish, and advisors increasingly feel pressure to find new and unique investment solutions for clients (in an era of increasing commoditization, not to mention an overall low-return environment for “traditional” stocks and bonds), it is perhaps no surprise that Schwab has announced a new “free” Schwab Alternative Investment Marketplace (in partnership with iCapital), which will provide RIAs on their platform with a wide range of alternative investment managers, an integrated platform that makes it easier than ever to allocate client dollars to such investments (with iCapital helping to pre-qualify clients electronically for Accredited Investor status, access to lower investment minimums [of ‘just’ $100,000], and paperwork facilitated via eSignature)… and providing Schwab with an opportunity to participate economically as alternative investment managers pay to be on the platform. Notably, the idea of creating a marketplace for investment managers – where the platform gets a piece of the action for helping to make the manager-advisor-client connections happen – isn’t new; in fact, it’s been the core model of Envestnet since it was founded as a third-party manager marketplace, and has been further expanding recently in the explosion of “Model Marketplaces” where asset managers share dollars to FinTech platforms that help to facilitate distribution of their investment solutions. However, while FinTech platforms have been increasingly trying to become investment product marketplaces – and get paid for distribution – the reality is that brokerage firms are the OG distribution platform for investment products. After all, FinTech platforms may compete for advisor attention, but RIA custodial platforms literally already have the client assets, and are already the core platform advisors use to actually implement client investment portfolios. Which means even as industry pundits have raised questions of whether Envestnet will complement its FinTech platform by going into the brokerage custody/clearing business against Schwab, it looks like Schwab may be pre-empting them by using its brokerage custody/clearing business to go into the Envestnet third-party (alternatives) manager distribution business first!?

New Product Watch: Will FinTech Enable Startups Like FactorE And Portformer To Reinvent The Proprietary Investment Newsletter As A Proposal Generation Tool? In the past, investment analysts who were able to develop their own unique method of analyzing investments typically implemented it by either launching or working for an asset manager, where their work could be put to direct use in generating hopefully-more-favorable investment results. On the one hand, putting such analytics to work directly at an asset manager could be an incredibly effective way to monetize the intellectual property value of the proprietary analytical process. On the other hand, there wasn’t much choice of any other way to monetize, short of trying to publish a one-to-very-many “investment newsletter” in the hopes that subscribers would put those investment methods to use in their own portfolios. But the emergence of technology is creating a new alternative methodology to monetize proprietary investment analytics – by turning it into a Proposal Generation tool that analyzes a prospective client’s portfolio to identify potential gaps or flaws, and then demonstrate how the advisor’s alternative may be superior. Of course, the idea of turning investment analytics into a proposal generation tool isn’t new – it is effectively the original and still-core business model of Morningstar and its Star (and now additional Analyst and also Sustainability) ratings. But the rise of the internet and APIs has democratized both the ability to collect data, embody it in software, and quickly and easily distribute it to investors or advisors… leading to a recent surge of new Proposal Generation platforms that are actually proprietary investment analytics/algorithms embodied into software, purporting to provide unique ways to both analyze (and find the flaws in) existing client portfolios, and secondarily to help advisors construct better ones themselves. In the past, this has included platforms like Chaikin Analytics, and more recently the emergence of FactorE (which provides a unique factor analysis approach to deconstruct portfolios and their factor exposures, shown to the prospective client as a unique factor ‘fingerprint’ diagram), and Portformer (which analyzes mutual fund and ETF portfolios to identify high-cost or poor-performing funds based on its own unique analytical process, and then helps the advisor to proposed more appealing alternatives to be implemented). Ultimately, though, tools like FactorE and Portformer will live or die not just by their ability to generate an investment proposal with appealing technology, but their ability to get buy-in and acceptance from advisors about the value of their proprietary analytical process… which is no small task in a world where Morningstar has already become the ubiquitous and de facto standard. On the other hand, the fact that Morningstar is so widely used creates pressure on advisory firms to come to the table with some different and unique analytical investment process – given that any/every other advisor can already do the same analysis with the same Morningstar reports (or the consumer can look up the funds themselves on Morningstar.com!). At a minimum, though, the approach of turning a proprietary investment process into technology that supports proposal generation and (unique and differentiated) investment analytics is a trend that seems likely to continue, as those who create the intellectual property value of the analytical investment process itself find new and original ways to monetize and distribute it via FinTech!

New Product Watch: Advisor Episodes Launches Ready-Made ‘More Shareable’ Video Content For Advisor Social Media. One of the game-changing aspects of social media platforms was/is the ability for “anyone” to create their own audience of followers, to whom they demonstrate their expertise and generate potential business, at a miniscule fraction of the cost of traditional advertising and other marketing strategies. The caveat, however, is that when it comes to financial advisors, most do not have a natural skillset to create such content in order to demonstrate their expertise in the first place, which has led in recent years to the rise of numerous platforms, like Vestorly and Financial Media Exchange, that aim to create pre-packaged content that advisors can share via email and social media in order to gain followers and eventually generate new clients. Unfortunately, though, in practice, such platforms have struggled to gain traction, due in no small part to the fact that most advisory firms are so unfamiliar with “digital marketing” strategies that they don’t know how to convert newly gained followers into clients, even with the help of platforms that provide the content to share. On the other hand, in many cases advisors struggle and fail on social media simply because the content they share still isn’t that compelling to social media followers, in what is becoming an increasingly visual (i.e., video-based) medium. Accordingly, this fall marked the launch of Advisor Episodes, a new social media pre-packaged content solution for advisors, aiming to create short pre-packaged videos (i.e., “episodes”) that advisors can share via their social media channels. Launched by a group of former Riskalyzers, Advisor Episodes is taking a narrow and simple focus – to create high-quality, “shareable” videos for advisors (leveraging the recent statistic that 90% of all content shared on social media is video), which notably means not necessarily delving into dense financial planning topics, and instead sticking with more “high-level” content like a 26-second primer on the Equifax Settlement or 31 seconds on Millennial Money Habits. However, the ultimate question is whether sharing more ‘generic’ content that is not specific to the advisor’s expertise will really be able to turn shareable video content into actual clients (or at least bona fide prospects) for advisors, or whether Advisor Episodes will eventually go the way of Vestorly that similarly failed to gain traction with advisors sharing third-party not-necessarily-financially-related content (ostensibly as advisors failed to actually turn such content-sharing into real clients). At a minimum, advisors who are already active on social media, with a coherent digital marketing strategy to convert followers into clients, may appreciate Advisor Episodes as a complement to their menu of content to share (especially at Advisor Episodes’ very palatable $34/month cancel-at-any-time price point). Unfortunately, though, it’s not clear whether the market of already-social-media-savvy advisors is enough to support a platform like Advisor Episodes, or whether they will ultimately be able to bear out the claim that high-quality-but-not-necessarily-demonstrating-expertise video content for advisor can actually turn into bona fide new clients.

New Product Watch: JourneyGuide Launches Retirement Planning Software That Models Actual Retirement Annuity Products. While in the modern era, financial planning is increasingly being delivered as a service in and of itself (and compensated according by financial planning fees), for most of its history “financial planning” was a way to demonstrate a need for a product (that the advisor was subsequently compensated to implement), and financial planning software was built to help demonstrate the need for the financial advisor’s available products as solutions. The irony, though, is that while financial planning software has long been used to facilitate the sale of financial services products, actual product illustrations have remained entirely separate from the planning software. Thus, for instance, financial planning software’s accumulation projections for retirement might show that the client needs to save and invest more, but the actual proposed portfolio for implementation would be illustrated separately, and financial planning software might show a material risk of failure in the client’s retirement plan, but the particular annuity solution to guarantee that retirement income would be sold via separate product illustration. In this context, it’s notable that newcomer JourneyGuide has launched a new retirement planning software solution that illustrates actual annuity product solutions (from variable annuities to single premium immediate annuities, fixed indexed annuities to longevity annuities) as a part of the client’s retirement plan. Drawing on a library of more than 120 annuity products from 31 annuity carriers, with product pricing updated to the day, JourneyGuide illustrates whether or how the client’s retirement plan outcomes improve with the actual features of particular annuity products, modeled along an “Income Frontier” chart (that shows how the plan improves, or not, with the annuity product, in various Monte Carlo scenarios). Of course, the caveat of such a solution is that for certain types of annuities – particularly fixed indexed annuities with non-guaranteed participation rates, caps, and spreads – it’s difficult to determine whether the underlying assumptions embedded in the product being illustrated are realistically sustainable in the first place. And in practice, some higher-cost annuity products may not actually hold up to scrutiny when illustrated in a real-world retirement planning scenario (at least relative to lower-cost annuity alternatives)… which means JourneyGuide itself may face a potential backlash from certain annuity carriers if/when they discover their products don’t illustrate well in practice. But from the advisor’s perspective – and the end client – isn’t the ability to determine which annuity products really do or don’t help exactly what good retirement planning software should be able to illustrate… and perhaps in the process, accelerate the shift to fee-based annuities and finally bring some long overdue scrutiny to the wild west of the illustrations in the current annuity marketplace?

________________________________________

In the meantime, we’ve updated the latest version of our Financial Advisor FinTech Solutions Map with several new companies, including highlights of the “Category Newcomers” in each area to highlight new FinTech innovation!

So what do you think? Would Schwab consolidating the TD Ameritrade VEO platform impact innovation in advisor FinTech? Can BidMoni’s FiduciaryShield gain traction by helping advisors actually find new 401(k) plans to do business with? Would you use pre-made Advisor Episodes videos on your social media channels? And would you encourage clients to leave reviews on a third-party Advisor Ratings site if the SEC’s proposed changes to the advertising rules go through?

Learn more about reprints and licensing for this article.