Sponsored Content from Protective

Rethinking the Risks of Retirement

A new study finds that clients want fiduciary advice, risk management ability and retirement income solutions from advisors — who may find that guaranteed retirement income solutions now resonate.

The world has changed — especially for advisory clients in or near retirement. After a long period in which they enjoyed rising and relatively stable markets, low inflation and increasing confidence in the future, those over the age 55 now face a time of greater market volatility and lower returns, surging inflation and greater anxiety overall — no doubt spawned by the pandemic and increasing global tensions.

Helping clients navigate this “new normal” has become one of advisors’ most important challenges. A recent study, “The Value of Advice,” conducted for Protective by InvestmentNews Research, offers insights into what clients in or near retirement are thinking and how advisors can provide value in these more difficult times. The study reflects responses from advisors and investors, of whom 69% are over 55 years old, and shed light on the services that clients value most from advisors.

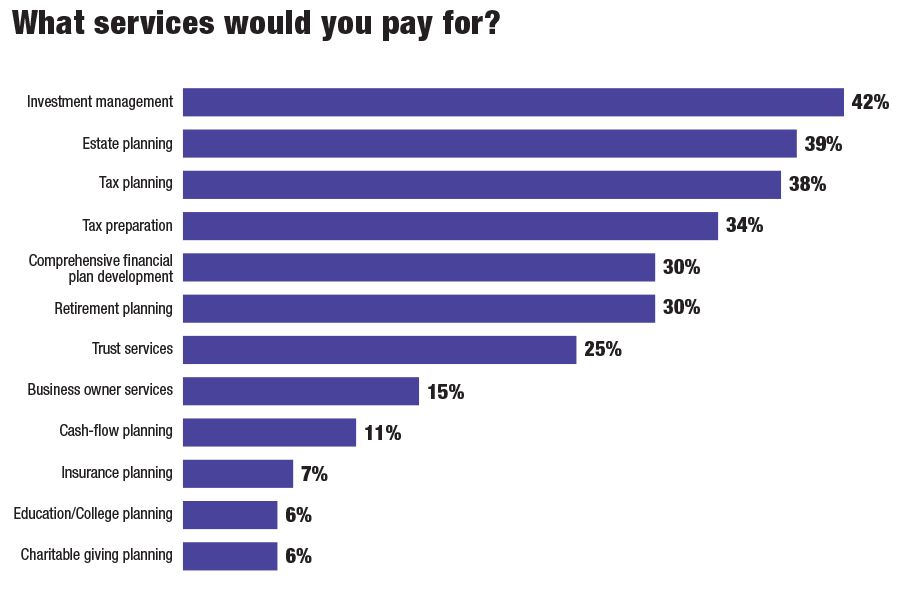

What can be inferred from these survey results is that clients overwhelmingly view advisors as sources of investment-related information and advice. Since investments are top of mind among most clients when dealing with their advisor, it is not surprising that the advice they want is largely related to investments. When asked which services they would specifically pay for, 42% said investment management, 39% said estate planning and 38% noted tax planning and tax preparation, followed by comprehensive financial planning and retirement planning, each at 30%.

Advisory fees are a bigger issue among clients than advisors may think. Only 19% of clients in our survey said they would stick with an advisor who raised fees; 57% of advisors, however, were highly confident most clients would stick with them. Nevertheless, clients are not averse to paying for performance. When clients were asked how they think about performance and fees in connection with investment selection, the largest group, 49%, said that performance is their most important consideration, while they also consider fees. Thirty percent said they consider performance and fees equally. Only 13% said they consider fees most important, but even they take performance into consideration.

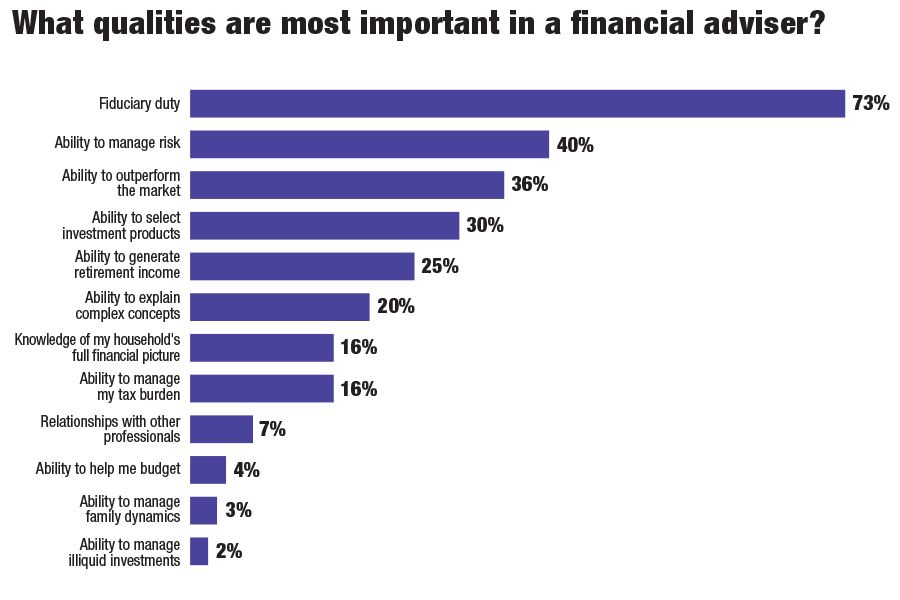

While clients are heavily focused on investment performance and have strong views on fees, other issues are important to them. In fact, clients rank having an advisor who is a fiduciary most important of all, a quality cited by 73% of respondents. Significantly, clients rank risk management second (cited by 42% of respondents) among all factors they consider important in a financial advisor. Following in importance are the ability to outperform the market (36%), ability to select investment products (30%), ability to generate retirement income (25%) and ability to explain complex concepts (20%).

Clearly, in addition to delivering investment performance at a reasonable cost, clients also want their advisor to educate them about the many financially related issues they will face in the future as well as about the financial products that can deliver the income they seek to live comfortably in retirement.

To quell client’s fears about running out of money in retirement, which they may not directly express, advisors should explore solutions that offer lifetime guarantees. Those guarantees can help cover fixed expenses in retirement, as well as help with lifestyle spending. A variable annuity with an optional guaranteed minimum withdrawal benefit is one of those solutions. With these flexible and customizable products, advisors can help clients select from a variety of investment options, provide them with the tax deferral that investing within an annuity provides, and take advantage of an income stream that they cannot outlive. Additionally, guaranteed income offers important behavioral advantages. By creating a lifetime income from savings, retirees can lessen the worry of outliving savings, and research suggests that this freedom results in a more satisfying retirement.

While today’s investing climate has changed the risks of retirement, advisors have the tools to address those risks through a wide range of solutions, including those that offer guaranteed lifetime income. In fact, an advisor’s access to such solutions, plus their skill in providing information, guidance and support, constitute the true value of professional advice.

Lauren Drapeau is National Sales Director of Annuity Advisory Solutions at Protective and a registered representative of Investment Distributors, Inc., a Registered Broker/Dealer, member FINRA and wholly owned subsidiary of Protective Life Corporation.

Protective® is a registered trademark of Protective Life Insurance Company. The Protective trademarks logos and service marks are property of Protective Life Insurance Company and are protected by copyright, trademark, and/or other proprietary rights and laws.

Protective refers to Protective Life Insurance Company (PLICO) and its affiliates, including Protective Life and Annuity Insurance Company (PLAIC). PLICO, founded in 1907, is located in Nashville, TN, and is licensed in all states excluding New York. PLAIC is located in Birmingham, AL, and is licensed in New York. Product availability and features may vary by state. Each company is solely responsible for the financial obligations accruing under the products it issues. Product guarantees are backed by the financial strength and claims paying ability of the issuing company. Securities offered by Investment Distributors, Inc. (IDI) the principal underwriter for registered products issued by PLICO and PLAIC, its affiliates. IDI is located in Birmingham, Alabama. Insurance and Annuities are: Not a Deposit | Not Insured by any Federal Government Agency | Have no Bank or Credit Union Guarantee | Not FDIC/NCUA Insured | May Lose Value

Learn more about reprints and licensing for this article.

This content is made possible by Protective; it is not written by and does not necessarily reflect the views of InvestmentNews' editorial staff.