Why retirement plan adviser RFPs are critical to participant success

dcasdfadsfvsdfgasdsd

dcasdfadsfvsdfgasdsd

And why it’s not happening

It’s accepted practice that defined-contribution plans should periodically benchmark their record keeper’s fees and services by going out to bid every three to five years. But 15 years ago, providers resisted questioning why, if the services and fees were reasonable, it was necessary to go to market or even benchmark.

[More: The danger of focusing on retirement plan participant outcomes]

Many retirement plan advisers created their businesses by conducting due diligence on funds and record keepers. But most advisers, even the elite plan advisers, are reluctant to advocate that their clients or prospects conduct documented due diligence on them.

The reasons are obvious. There’s risk that the adviser may

lose the client and, more likely, that their fees will be reduced. What’s their

upside?

David Levine of the Groom Law Group notes, “Advisers, like any other service provider, need to be reviewed periodically even if they are doing a good job.”

Mr. Levine is seeing an increase in plan adviser RFPs in the midmarket following the accepted trend in the institutional market. “The drivers include increased awareness by plan sponsors about their duty to monitor, litigation, and the evolving role of the advisers who are branching out to other services like 3(38) outsourcing.”

Most DC plans under $500 million rely heavily on their adviser to conduct due diligence on other service providers but logically cannot ask or rely on the same adviser to fairly conduct due diligence on themselves or competitors. There are third parties like InHub that can help, as well as advisers, but getting the word out is hard.

Relationships can get in the way. It’s not hard for a plan sponsor and adviser to tell a provider that the plan needs to conduct prudent due diligence — it’s harder to tell that to a person with whom the plan sponsors may have a close relationship and may be doing everything asked.

Brian Allen, founder of Pension Consultants Inc., an elite advisory firm in Springfield, Mo., noted that, “Adviser RFPs are the way that DC plans select adviser based on performance rather than brand or image.” The talk about improving outcomes is just that — talk — unless advisers are forced to prove they are making an impact along with showing they have the required resources.

[More: Should advisers have to pick between retirement or wealth management?]

“There actually might be fewer plan adviser RFPs on traditional services like fees, funds and fiduciary in the future,” said Hugh O’Toole, president at Innovu, a data analytics company focused on human capital risk management, and former head of sales for MassMutual’s retirement division.

“Plan sponsors looking to maximize human capital while minimizing costs are starting to look at how retirement and health care services affect performance and the bottom line.” Mr. O’Toole said. “Plan sponsors are ahead of plan advisers on the confluence of benefits and retirement and may just engage plan advisers for definable services for a flat fee, alleviating the need for a traditional plan adviser search or RFP.”

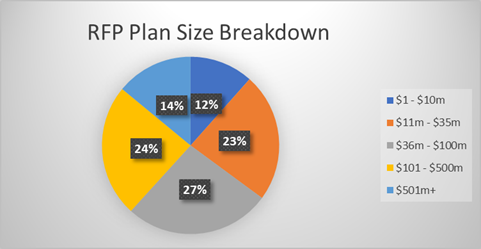

According to InHub, 35% of the adviser RFPs processed were for plans under $35 million in assets, with 62% under $100 million. (See chart below.)

Ariana Amplo, founder of InHub, noted that 50% of the RFPs came from companies that had conducted one in the past five years. She said that shows that “Many plan sponsors are embracing the advice of ERISA attorneys and running this type of project every four to five years, regardless of whether or not the committee thinks there are service or fee issues.”

Regardless, many plan sponsors have an unhealthy allegiance to their adviser out of loyalty or laziness. Realistically, a surge of adviser RFPs in the $10 million-$500 million plan is unlikely, because most plan sponsors are just waking up about their retirement plan although they are increasing, said Greg Middleton, director of marketing at Captrust.

[More: Benefits of cross-selling are too big for RPAs to ignore]

But even if a plan adviser is doing everything right at a reasonable cost, ERISA still requires the plan sponsor — the fiduciary with ultimate responsibility — to conduct periodic documented due diligence on their adviser either themselves or with the help of a qualified third party. Adviser or consultant RFPs are accepted practices by larger plan sponsors, and there’s no doubt that will move down-market.

Only when the tide turns on RFPs for advisers, as it did 15 years ago for record keepers, resulting in massive consolidation, will we know which advisers are swimming naked.

Source: InHub 2020

Fred Barstein is founder and CEO of The Retirement Advisor University and The Plan Sponsor University. He is also a contributing editor for InvestmentNews‘ Retirement Plan Adviser newsletter.

Learn more about reprints and licensing for this article.